by Jim the Realtor | Jul 18, 2023 | Mortgage News, Neg-Am |

The Orange Man pioneered the distribution of neg-am mortgages to the masses, and then hoodwinked Wall Street into thinking the loans were worthy of buying in tranches – yet he didn’t want to take the blame and instead enjoyed his retirement as a member at all the private golf clubs around Brentwood.

Some of his best quotes:

In 2006, when Mozilo was the chief of the mortgage lender Countrywide Financial, the firm originated $461 billion worth of loans — close to $41 billion of which were subprime. Subprime loans were responsible for the global financial crisis.

Mozilo was also charged by securities regulators of insider trading and securities fraud. Once named as one of the best chief executives in the United States, the disgraced CEO was subsequently named as the second worst US chief executive of all time by Conde Nast Portfolio.

“I’m fairly confident that we’re not going to do anything stupid,” he told The Wall Street Journal in 2004 when asked about the risks of a housing bubble. “We have a history of not doing anything stupid.”

Yet Countrywide, like many other lenders, embraced riskier types of loans. By August 2007, Wall Street worried that Countrywide might go bankrupt.

In January 2008, Bank of America agreed to buy Countrywide for what seemed like a bargain-basement price, $2.5 billion, which was less than 10% of what it was worth in 2007.

It was no bargain. The acquisition ended up costing Bank of America tens of billions of dollars in real-estate losses, legal expenses and settlements with regulators.

Mozilo retired from Countrywide, at age 69, a few months after the sale to BofA. Later, the Securities and Exchange Commission accused him of fraud, saying he had offered rosy assessments of Countrywide while dumping nearly $140 million of Countrywide stock.

In 2010, he agreed to settle the SEC’s charges without admitting or denying wrongdoing. He also agreed to pay $67.5 million in penalties; the bulk of that was covered by indemnities from Bank of America.

In interviews in 2018 and 2020, Mozilo told the Journal he had been unfairly singled out for blame in the aftermath of the housing bust. “I was very visible,” he said. “Anytime I was asked to go on TV, I did it.” As a result, he said, “When the s— hit the fan, everybody looked at me.”

Mozilo had defended himself several times against accusations that he was a key architect of the 2007-2009 financial crisis.

“Somehow, for some unknown reason, I got blamed for it,” he earlier said.

Mozilo had reason to cheer as well. In 2006, he was paid $48 million, beating JPMorgan Chase & Co. Chairman and CEO Jamie Dimon by $10 million and Bank of America CEO Kenneth Lewis by $20 million. From 2000 until 2008, Mozilo received total compensation of $521.5 million, according to Equilar, a compensation-research firm.

Looking back on those boom years, Mozilo said Countrywide had been swept up in a “gold rush” mentality that had overtaken the US. “Housing prices were rising so rapidly — at a rate that I’d never seen in my 55 years in the business — that people, regular people, average people got caught up in the mania of buying a house, and flipping it, making money,” he said in a 2010 interview with the US Congress-appointed Financial Crisis Inquiry Commission.

“Housing suddenly went from being part of the American dream to house my family to settle down — it became a commodity,” he said. “That was a change in the culture.”

by Jim the Realtor | Jan 23, 2019 | Jim's Take on the Market, Mortgage News, Mortgage Qualifying, Neg-Am |

Hat tip to both Rick and Richard sent in this article from the WSJ on alternative underwriting for mortgages, which is on the rise:

https://www.wsj.com/articles/no-pay-stub-no-problem-unconventional-mortgages-make-a-comeback-11548239400

Excerpted – bold added:

Aryanna Hering didn’t have pay stubs or tax forms to document her income when she shopped around for a mortgage last year—a problem that made it tough for her to get a loan.

But the nursing student who works part time providing home care for children and the elderly eventually hit pay dirt: For a roughly $610,000 home loan, a mortgage company let her verify her earnings with 12 months of bank statements and letters from clients.

Ms. Hering’s case highlights how a flavor of mortgage once panned for its role in the housing meltdown a decade ago is making a comeback. These loans, aimed at buyers with unusual circumstances such as those who can’t provide the standard proofs of income, are growing rapidly even as rising interest rates and higher home prices crimp demand for mortgages.

Lenders issued $34 billion of these unconventional mortgages in the first three quarters of 2018, a 24% increase from the same period a year earlier, according to Inside Mortgage Finance, an industry research group. While that makes up less than 3% of the $1.3 trillion of mortgage originations over that period, the growth is notable because it came as traditional home loans declined. Those originations fell 1.2% over the same period and were on track for a second down year in 2018.

Tom Jessop, the loan consultant at New American Funding who handled Ms. Hering’s loan, said he has seen demand for unconventional loans double over the past 18 months and they currently makes up more than one-third of his business. “I think it’s just catering to an audience that’s been neglected for years,” Mr. Jessop said. “Now they have an opportunity to get financing finally.”

At the same time, Wall Street investors who buy home loans are scooping up unconventional mortgages that have been packaged into bonds, edging back into a corner of the market that is riskier but provides higher returns. There were $12.3 billion of such residential-mortgage-backed securities sold in 2018, nearly quadruple from a year earlier, according to credit-rating firm DBRS Inc.

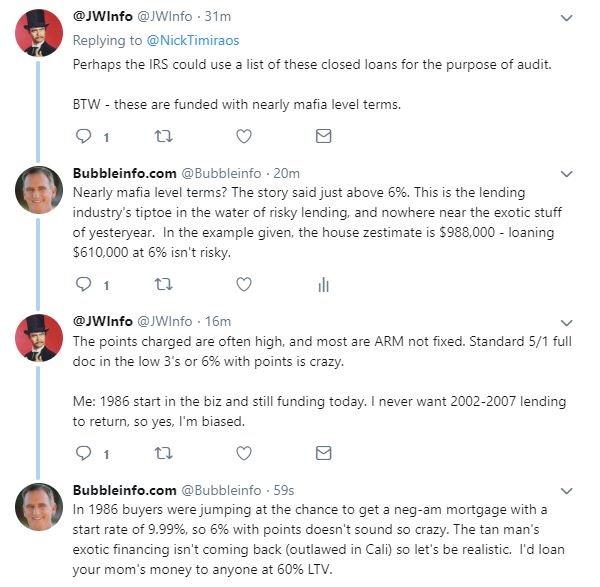

Nick also put it on twitter, where I responded:

Back in 2006-2007, Countrywide was funding neg-am mortgages up to $1,500,000 with no money down and just a decent credit score – the example given is far from that.

The mortgage industry needs to find a balance in between – it’s not out of line to finance a borrower who can show income via bank statements and has substantial equity/skin in the game.

by Jim the Realtor | Aug 27, 2017 | Jim's Take on the Market, Mortgage News, Mortgage Qualifying, Neg-Am |

In what has to be one of the most bizarre developments in real estate this year, the ivory-tower folks at the Fed, of all people, dreamed up a creative new loan that would not require a down payment. Then they used the dreaded COFI term from neg-am mortgage days! No word on when these might be available, if ever:

https://www.federalreserve.gov/econres/feds/2017.htm#2017090

Abstract: The 30-year fixed-rate fully amortizing mortgage (or “traditional fixed-rate mortgage”) was a substantial innovation when first developed during the Great Depression. However, it has three major flaws. First, because homeowner equity accumulates slowly during the first decade, homeowners are essentially renting their homes from lenders. With so little equity accumulation, many lenders require large down payments. Second, in each monthly mortgage payment, homeowners substantially compensate capital markets investors for the ability to prepay. The homeowner might have better uses for this money. Third, refinancing mortgages is often very costly.

We propose a new fixed-rate mortgage, called the Fixed-Payment-COFI mortgage (or “Fixed-COFI mortgage”), that resolves these three flaws.

This mortgage has fixed monthly payments equal to payments for traditional fixed-rate mortgages and no down payment. Also, unlike traditional fixed-rate mortgages, Fixed-COFI mortgages do not bundle mortgage financing with compensation paid to capital markets investors for bearing prepayment risks; instead, this money is directed toward purchasing the home. The Fixed-COFI mortgage exploits the often-present prepayment-risk wedge between the fixed-rate mortgage rate and the estimated cost of funds index (COFI) mortgage rate.

Committing to a savings program based on the difference between fixed-rate mortgage payments and payments based on COFI plus a margin, the homeowner uses this wedge to accumulate home equity quickly. In addition, the Fixed-COFI mortgage is a highly profitable asset for many mortgage lenders. Fixed-COFI mortgages may help some renters gain access to homeownership. These renters may be, for example, paying rents as high as comparable mortgage payments in high-cost metropolitan areas but do not have enough savings for a down payment. The Fixed-COFI mortgage may help such renters, among others, purchase homes.

Keywords: COFI, Cost of funds, Financial institutions, Fixed-rate mortgage, Homeownership, Interest rates, Mortgages and credit

DOI: https://doi.org/10.17016/FEDS.2017.090

JtR: This sounds like the reverse of a neg-am mortgage, or a positive-amortizing loan where borrowers have a fixed payment as a ceiling, and then when rates float down, the difference is applied to the principal. But how much potential is there for your rate to drop when we’re at all-time lows? Maybe they are preparing a loan option for the day that rates rise substantially?

by Jim the Realtor | Jun 18, 2015 | Foreclosures/REOs, Jim's Take on the Market, Mortgage News, Neg-Am |

Hat tip to Wendy for sending in this article on subprime vs. prime mortgages causing the crisis. The authors probably didn’t catch the fact that prime borrowers were getting neg-am loans based on FICO scores only, and those weren’t considered subprime loans:

https://fortune.com/2015/06/17/subprime-mortgage-recession/?

An excerpt:

We can draw two conclusions from this data. One is that your chances of being foreclosed upon in the past decade was more a matter of timing than anything else. If you were a subprime borrower in, for instance 2002, who bought a bigger house than a more prudent and creditworthy borrower would have bought, chances are you would have been fine. But a prime borrower who did everything right—bought a house he could easily afford, with a large downpayment—but did so in 2006 would have had a higher chance of defaulting than the subprime borrower with better timing.

Since whether you were hurt by the crisis had more to do with luck than anything else, Ferreira argues we should rethink whether doing more to help underwater homeowners would have been a good idea.

https://fortune.com/2015/06/17/subprime-mortgage-recession/?

by Jim the Realtor | Oct 13, 2012 | Carmel Valley, Foreclosure Count, Neg-Am

I’m not sure if this displayed previously, but it was researched by one of the big data gatherers (initials C-L) about the Carmel Valley zip code 92130:

- Total number of homes in that zip code: 14,331

- Total number of Neg Am loans: 282

- Total number of SFRs with neg-am: 170

No wonder we haven’t seen many foreclosures around CV!

There have only been 15 detached REO listings close this year in the 92130, and only one was over $1,000,000 – the one we saw in Collins Ranch for $1,061,000. This is a zip code whose average sales price this year is $1,023,763, and 132 of the 373 sales (35%) have closed over $1,000,000.

by Jim the Realtor | May 12, 2011 | Mortgage News, Neg-Am |

From Reuters:

Remember way back in 2006, when everyone was in a frenzy to buy a house, any house, with whatever mortgage they could grab? In many cases, it meant signing up for adjustable-rate mortgages that would reset in half a decade.

Remember way back in 2006, when everyone was in a frenzy to buy a house, any house, with whatever mortgage they could grab? In many cases, it meant signing up for adjustable-rate mortgages that would reset in half a decade.

Move forward those five years and here we are.

For the next 13 months, some $20 billion in adjustable-rate loans are scheduled to reset every month, according to figures from Credit Suisse.

That means the interest rates and monthly payments will adjust — in most cases, downward, because of interest rate declines.

Homeowners will have to decide whether to keep their loans or replace them with a refinance. In a few cases, the adjustment of interest-only loans will make the monthly payments go up, even if their interest rates go down.

(more…)

by Jim the Realtor | Apr 13, 2010 | Bailout, Neg-Am |

Carl Levin is the chairman of the subcommittee that investigated the WaMu disaster – from the latimes.com:

“Washington Mutual built a conveyor belt that dumped toxic mortgage assets into the financial system like a polluter dumping poison into a river,” Levin said. “Using a toxic mix of high-risk lending, lax controls and destructive compensation policies, Washington Mutual flooded the market with shoddy loans and securities that went bad. . . . It is critical to acknowledge that the financial crisis was not a natural disaster, it was a man-made economic assault.“

Today the WaMu executives are testifying before Congress:

“As CEO, I accept responsibility for our performance and am deeply saddened by what happened,” said Kerry K. Killinger, WaMu’s former chief executive. But he and other executives said in their prepared remarks that they had worked to limit the company’s mortgage lending as the housing market began slowing and that, more than anything else, the bank was overtaken by economic events out of its control.

“Beginning in 2005, two years before the financial crisis hit, I was publicly and repeatedly warning of the risks of a housing downturn,” Killinger said. “Unlike most of our competitors, we aggressively reduced our residential first-mortgage business.”

Stephen J. Rotella, WaMu’s former president and chief operating officer, testified in his prepared remarks that he and others worked to reduce the company’s exposure to the deteriorating housing market but were unable to do enough — or to anticipate the historic market collapse.

“As the former COO of WaMu, I would like to be able to say that after my arrival at the bank in 2005, every decision that was made was correct,” he said. “But I was neither more prescient about the future than the chairman of the Federal Reserve Bank or the secretary of the Treasury, nor did I have complete decision-making authority at the company.”

In his first public statement since the bank was seized by regulators and sold for $1.9 billion to JP Morgan Chase, Rotella said the failure was principally the result of the company’s risky concentration in the housing market and rapid growth “magnified and exacerbated by the extreme conditions in the economy.”

“The executive team and all of our people worked very hard to mitigate those risks right up until the seizure and sale of the bank,” Rotella said.

(more…)

by Jim the Realtor | Mar 29, 2010 | Loan Mods, Mortgage News, Neg-Am, Option-ARMs, Thinking of Buying? |

From our friends at the W-S-J:

The struggling housing market appears as if it will sustain less damage than expected this year from a spike in the monthly payments on hundreds of thousands of exotic adjustable-rate mortgages.

The number of such loans scheduled to adjust to higher payments this year has shrunk. Lower-than-expected interest rates, coupled with efforts to aggressively modify loans, are likely to mute payment shocks for some borrowers. Many others already have defaulted on their loans even before their payments adjusted upward.

“The peaks of the reset wave are melting very quickly because the delinquency and foreclosure rates on these are loans are already very high,” says Sam Khater, senior economist at First American CoreLogic.

The housing market still faces enormous challenges, and a full recovery is likely to take years. The threat posed by resetting payments, Mr. Khater says, is “a drop in the bucket” compared to problems posed by the sheer volume of borrowers who owe more than their homes are worth, known as being “under water.”

Still, for years, housing analysts have worried about the threat of an aftershock from a big spike in mortgage defaults from so-called option adjustable-rate mortgages, which require low minimum payments before resetting to sharply higher levels, and “interest-only” loans, for which no principal payments are due for several years.

Most option-ARM borrowers made minimal payments, so their loan balances grew. That sparked worries about what would happen when those loans “recast” and begin requiring full payments on larger loan balances, usually five years from when they were originated or when the balance reached a designated cap.

Option ARMs may be among the most likely to benefit from the White House plan, announced on Friday, to force banks to consider writing down loan balances when modifying mortgages. Until now, the administration’s Home Affordable Modification Program, or HAMP, has focused on lowering monthly payments by reducing interest rates and extending loan terms to 40 years.

A separate program could benefit borrowers who are current on their loans but under water by allowing investors to refinance those borrowers into loans backed by the Federal Housing Administration. Investors are most likely to refinance the riskiest loans that qualify.

The majority of option ARMs are set to recast over the next two years. But the volume of outstanding loans has fallen sharply because many borrowers, prior to facing higher payments, received modifications, refinanced or defaulted. Option ARM volume peaked at 1.05 million active loans in March 2006. At the end of last year, there were 580,000 loans outstanding, according to First American CoreLogic.

(more…)

by Jim the Realtor | Mar 2, 2010 | Graphs of Market Indicators, Market Conditions, Neg-Am, Option-ARMs |

Our old friend Zach Fox has moved on to more illustrious things than the NC Times, he now works for a big-time financial publication back east.

But he hasn’t forgotten us little guys, especially the data geeks:

Jim,

We’re finally sending out some free links as we move toward getting our brand more to the public and not just Wall Street. I thought these stories might interest you and was hoping to piggy back on your ever-growing fame:

I got an update on that infamous Credit Suisse ARM reset chart, along with some interesting speculation from Greg McBride at Bankrate:

http://www.snl.com/interactivex/article.aspx?CDID=A-10770380-12086

I also thought this piece by one of our banking/insurance gurus was interesting. It runs through responses to FDIC’s securitization reform:

http://www.snl.com/InteractiveX/article.aspx?CDID=A-10788544-11055

Also, here is our bare-bones free site that has some TARP info. News is on the left-hand side, let me know if you see any links you can’t click on and would like to check out:

http://www.snl.com/Sectors/Financial-Institutions/FIG/Home/Tarp.aspx

Best,

Zach

by Jim the Realtor | Nov 13, 2009 | Loan Mods, Mortgage News, Neg-Am |

from NMN:

Residential servicers, a sector that is grappling with a potential tidal wave of loan modifications, are beginning to hire “like crazy” according to Mary Coffin, a senior servicing executive with Wells Fargo Home Mortgage. Ms. Coffin, speaking at SourceMedia’s Loan Modifications Conference in Dallas, noted that new servicing employees working on modifications are receiving four to five weeks of training in order to deal with the volumes they are facing.

“When you think about the number of people being added, and this is one of the most painful subjects for me, our history had always been to train early and often to make sure we were ahead of the default, delinquency and foreclosure forecast,” said the EVP in charge of loan servicing and post-closing for the nation’s second largest player in mortgages. “We would hire people, bring them in and maybe start them in collections, easier calls, and over tenure let them encounter workout situations. We no longer have that advantage in this environment. We are hiring people by the thousands and thousands. It is very painful. The borrower has high anxiety and a lot of fear, complex documents to sign and return to us, and you are hiring people that get four and five weeks of training.”

She said servicers are going much deeper in collecting financial information from the borrower. Ms. Coffin described a transformation of servicers and what has evolved as the foreclosure crisis began and where the company sits today.

“In the old way of doing business, when the borrower first went delinquent, we would start with a repayment program. They don’t work to the point to where we have almost tried to get rid of them. It is a circular process that ultimately ends up with a different solution that needs to be found,” she told conference attendees.

“Today, we’re underwriting the financial condition of the borrower in order to pick the right solution that is sustainable. That is the first big change that has happened for servicers.”

The Wells executive noted there has been confusion regarding documentation under the government’s Home Affordable Modification Program, including re-requesting documents from borrowers and instances of losing documents.

“We are still dealing with pulling documents. We have gone back to the administration and I’d like to thank them. They already streamlined the documentation requirements for the HAMP. If we receive what are called the ‘critical documents’ then we are able to do the underwriting and the decisioning that we don’t turn the customer down if every paper is not signed perfectly. That’s a real plus,” said Ms. Coffin.

“We still have work cut out for us. We have customers where the administration has extended it four to five payments. We have a few borrowers sitting in that situation. We have heavy, heavy lifting to do in the next couple months to pull these customers through.”

Wells is trying to be as innovative as possible, working with external third-party providers, using phone calls, mail, door-knockers, branches, its sales teams, everything possible to help these borrowers get these documents in and finalized.

Wells is seeing short-term modifications as another solution for people who are able to regain employment immediately or who require only a short-term mod. It is taking an aggressive approach to the option ARMs from Wachovia. It is the one area where Ms. Coffin says they are doing principal forgiveness.

“We have lower redefault rates. Our key to these pay-option ARMs, if a customer is able to make a payment, we have to find a way to continue to allow that payment to be able to be made. What we are doing is restructuring the loan looking at net present value. It’s been very effective. Many of these customers need to be bridged from a negative amortization to an interest only. If you took them to a fully amortized product, there’s no way they are going to be able to make it. Over time, they will from an IO, step up, so there’s no payment shock.”

Early on, after analyzing its portfolio, Wells quickly saw that yes, HAMP was going to be a great tool and valuable to use, but it was not going to save 100% of their problems.

“Thirty percent to 40% of our portfolio who would be eligible for HAMP was coming to us for solutions. The remainder did not meet the criteria for eligibility. The biggest one was they were coming to us with DTIs below 31%. So, we also went to work on our in-house modification programs.”

This included the payment-reduction mod and the implementation of a full-quality review so no loan can go to a foreclosure before it actually goes through a quality review test to make sure all opportunities have been reviewed.

“These loans are going through multiple looks before they ever go to the foreclosure sale,” she said.

After the creation of the HAMP program, the volume for Wells jumped to over 40% of borrowers who were current on their mortgage that tried to get modifications.

“I knew from talking to investors, their biggest concern was the moral hazard of this program and people going delinquent to get a mod. The guidelines were not provided on default definitions. We worked to provide consistency.”

Because of all the attention on modifications “we went from a day when borrowers who were truly in need called to say, ‘What can I do?’ and we know what to do. Now we are sorting through hundreds of calls from borrowers who have been educated to some extent. We are still educating them on what you truly have to look like before you can get a modification,” she said.