The new guy named Jeremy wandered into the discussion about short-sale fraud the other day, and found that long-time readers here don’t take kindly to scams – and scammers. But we’ve seen how short-sale fraud has run unabated, and that it has practically become a badge of honor among realtors. Nobody in the industry is motivated to stop it either.

Here are a few examples:

At the top of the last article, Jeremy’s friends were filing notices that mortgages were paid off when they weren’t, which is outright fraud. But the second half of the article mentioned the typical example of short-sale fraud, where a straw buyer purchases the property at a below-market price, and then spoons it to a waiting buyer who pays retail. The banks who got shorted on the first sale might have caught the fraud with better appraisals, or if they just had a strict policy. I’ll never forget the one case where the perpetrator caught wind of his own story here on the blog and left a his comment. He said they included in their contract to flip the house immediately to the shorted bank. They then flipped their short-sale buy on the SAME DAY to a retail buyer for a $100,000+ profit. If the banks have knowledge and turn their head, then it’s on them.

A short-sale that’s fully furnished. The seller makes the furniture sale mandatory so he can squeeze some cash out of the deal – he sells the ‘furniture’ to the buyer for $50,000 to $100,000 outside of escrow, in exchange to agreeing to a low-ish sales price for the house. Usually these are cash sales only.

Listing agent twists seller’s arm to take his buyer, rather than one of the two higher cash offers. I turned this one into VP of Fraud at the Bank of America, who said that because the lower price was still within their acceptable range, he’d let it go.

There were the investors who approached naive listing agents and insisted on negotiating their own deal with the bank. If they could get the price approved low enough to flip immediately, they’d complete the purchase.

Both short sale and REO investors engage in ‘reverse staging’ to make a property appear in worse condition than it is, including the removal of kitchen-cabinet doors, garbage left lying around the home, and sometimes old fish hidden behind refrigerators to create pungent scents. Sometimes BPOs include false property stigmas such as high crime rates, or claim the home was a meth lab that would need to be entirely gutted.

Parents buying their child’s over-encumbered house as a short-sale. A favorite among realtors themselves.

Thankfully most of these are in the rear-view mirror!

The Redfin Estimate has the lowest published error rate of any valuation estimate in the U.S., with only a 1.96 percent median error rate for homes that are for sale, and 6.25 percent for off-market homes. This means that when a home that is currently on the market sells, the Redfin Estimate will be within 1.96 percent of the sales price half of the time. For off-market homes, the Redfin Estimate will be within 6.25 percent of the eventual sales price half the time. The Redfin Estimate is more accurate for homes that are for sale because there is more data available about those homes.

As a real estate brokerage, Redfin has 100% complete, direct access to Multiple Listing Services (MLSs), the databases that real estate agents use to list properties. This gives us information about homes that non-brokerage websites don’t have, like whether the home has a water view or is located on a busy street. The Redfin Estimate algorithm considers more than 500 data points about the market, the neighborhood, and the home itself. When all of this data meets the massive computing power of today’s best cloud technology, you get the Redfin Estimate.

(bold added by JtR)

More than 500 data points?

Massive computing power?

Today’s best cloud technology?

Those sound great from a marketing perspective. They want you believe that they have developed a proprietary tool that is better than all others – especially better than anything from those dastardly folks at Zillow.

But it sure looks like their estimates are just closely tied to the list and sold prices, not some superior algorithm.

Let’s consider some evidence.

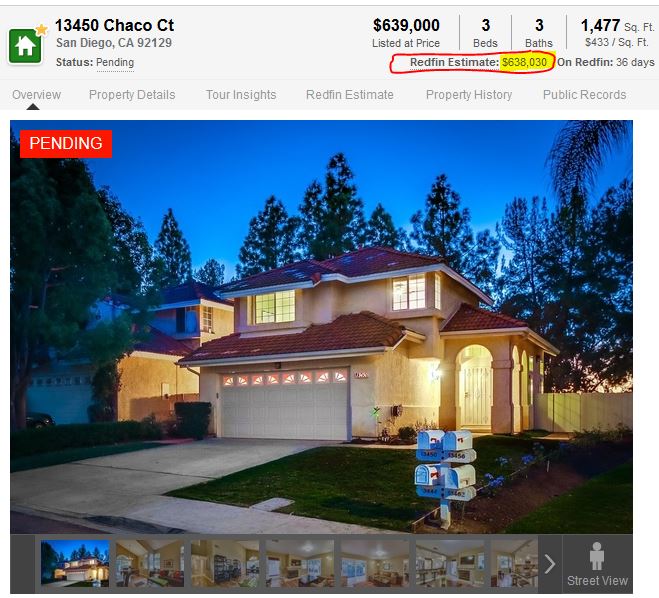

Prior to it hitting the open market, no one would have estimated the value of my listing on Chaco above $620,000. The average cost-per-sf of the solds over the last six months is a lofty $400/sf multiplied by 1,477 sf = $590,800. There was a larger one-story house that had just closed around the corner for $605,000, and the current CMA shows that there hasn’t been any evidence before or since the sale that would indicate a value much higher:

Yet once the listing hit the market, the Redfin estimate is $638,030. The only way it could be that high was if the estimate was tied to the list price, and they add or subtract their 1% to 2% to make it look legit:

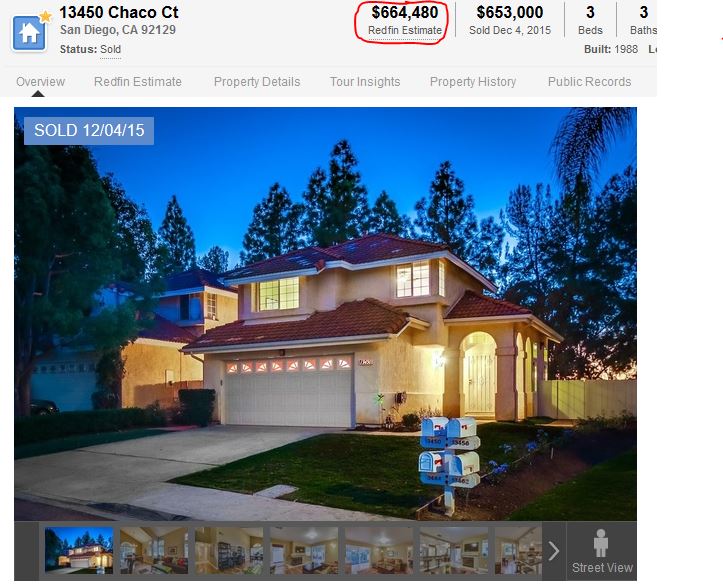

The snip above was clipped the day before escrow closed. Two days later, their estimate rose four percent to 1.8% ABOVE THE ACTUAL SALES PRICE.

But looking at the CMA, there wasn’t any other evidence to support a change in value over the three-day period. It appears that they just added a fairly random 1.8% to the sales price, which kept them within their pledge that half of the sales will close within 1.96% of their estimate:

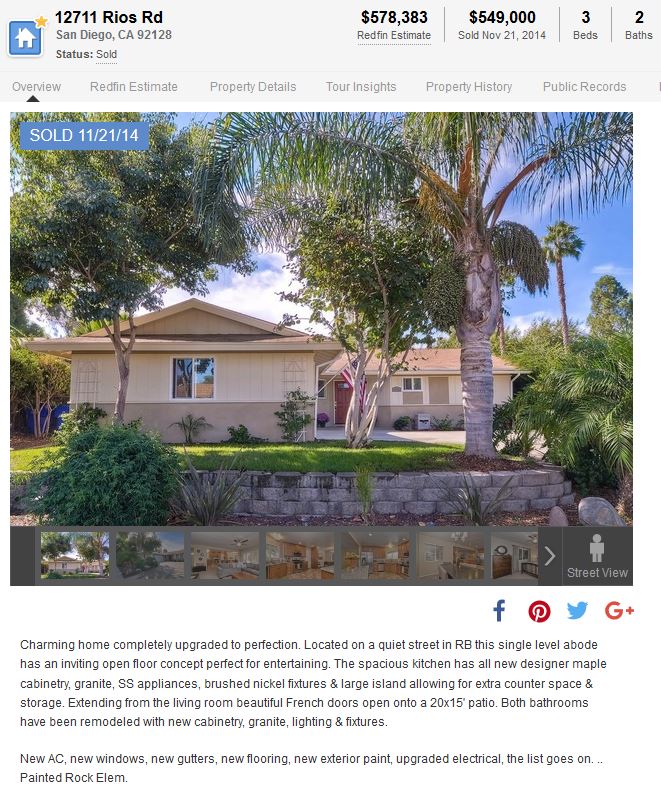

Here’s another example.

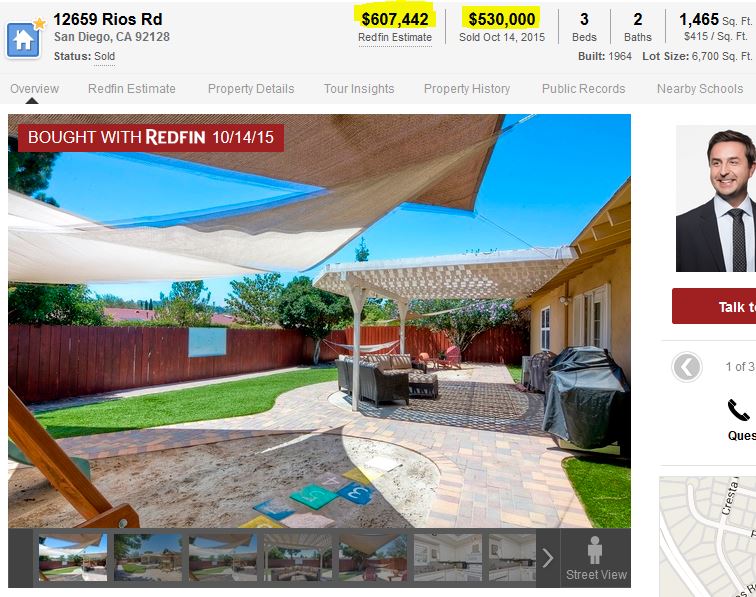

The day the Rios property listed on the MLS, I first snipped the Redfin old ad:

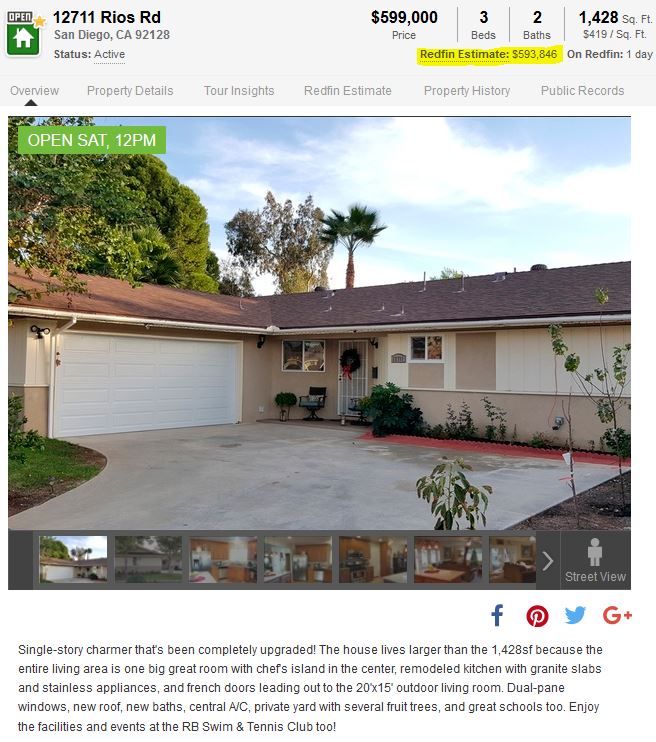

After the new listing was inputted onto the MLS and populated to Redfin, their estimate has magically risen $15,463 in just three hours, to $593,846 – and conveniently within their range of +/- 1.96%:

If all they are doing is adding or subtracting a couple of percentage points from the list and sales prices, then fine – they should state that.

But they give the impression that it’s their new whiz-bang technology that is generating their estimates, and claiming it to be the new and better-than-all-the-rest value estimator.

It also makes you wonder about their end game – will they also use their estimator to hype Redfin agents, and dog the other non-Redfin agents?

This buyer below was represented by a Redfin agent, and now the Redfin estimate of value has increased a whopping 15% in two months:

They state that their estimate is based on six solds over the last year, and they list the comps. Considering the evidence they provided, do you come up with a $607,442 value?

Redfin will probably be able to shrug off any general criticism of their estimates by just calling it a rounding error. If they are deliberately pegging their estimates to within a couple of percentage points of the actual list and sold prices in an effort to play nice with their fellow realtors, it would be understandable – and playing nice has been their track record.

If they also want to add a little juice to their own agent’s history to make them look better, I guess it wouldn’t be a surprise – heck, every realtor fluffs their sales record.

But this is where they are going to get themselves in hot water.

When a zestimate is below the list price, the Zillow folks are quick to say that it is just a starting point, and to consult with a realtor to pinpoint the exact value. The realtor community will live with that approach.

But what happens when a Redfin estimate is well under the list price?

Don’t the agents who have listings that aren’t selling have a right to be upset with their fellow realtors at Redfin if they have a low estimate? Yes, indeed.

A Redfin estimate – generated by more than 500 data points, massive computing power, and today’s best cloud technology – that comes in low and then is published on one of the most popular real estate websites will publicly undermine the chances of selling the house.

Listing agents won’t tolerate other realtors publishing low estimates online to a wide audience of buyers – especially when the estimates (and motives) are suspect from the beginning.

Thanks to Susie for sending in this story of everyday realtor fraud – committed by the third-highest-producing agent team in the country – and an agent who just couldn’t be a do-gooder and turn them in. He tried to extort $800,000 from them instead:

As well as being outspoken, Tomlinson had earned a reputation as a whiz with an online database known as the Multiple Listing Service, which can only be accessed by brokers and Realtors, and supplies the data for web services such as Realtor.com.

He alleged that when the Jills couldn’t sell a home, they would sometimes hide it from other users of the MLS. That could mean, for example, changing the address of a mansion on North Bay Road so that it would appear to be located in Allapattah, where few high-end brokers would think to look.

To the untrained eye, it looked as if the Jills were better at selling homes than their actual record suggested. And even more important: the scheme prevented other brokers from offering their services to clients whose listing were expiring on the database. Realtors only have exclusive rights to sell a home for as long as their contract with the owner lasts. Once the listing expires, the home is fair game for competitors.

In his complaint to the board, Tomlinson cited 51 instances where the Jills had hidden homes.

Esther Percal, a top broker at EWM Realty International with nearly four decades of experience, blasted the Jills’ conduct.

“The Jills broke the rules. They have a near monopoly on the top of the market because they’ve branded themselves so well,” Percal said. “They say they’re the best and they can bring the best prices, but they don’t have a magic wand. Their listings can expire like everybody else.”

In a response to Tomlinson’s complaint — now evidence in the criminal case — the duo admitted using “poor judgment,” but said they never realized “the consequences” of the data jiggering. And they denied their conduct actually broke Realtor association rules.

About five years ago, the Jills explained, they got a call from an “irate client” whose property had not sold. The client had gotten “a barrage of unsolicited calls” from other Realtors looking to snag business as his listing had just expired.

The Jills said that a staffer — unnamed in the document — overheard the call and “indicated that, in the future, a client’s property could be kept off a list known as the ‘Hot Sheet,’ ” which Realtors scoured for new business. From then on, the Jills acknowledged, they would “from time to time” keep other unsold properties off the collection of the expired listings, according to the response.

When police responded to reports of a squatter at a San Francisco mansion over the weekend, they didn’t expect to catch an alleged art thief believed to have stolen and sold paintings valued at more than $300,000.

While squatting in the home, Jeremiah Kaylor, 39, took 11 paintings from the walls and sold them through social media and pawn shops, said Officer Carlos Manfredi, a spokesman for the San Francisco Police Department. Nine of the 11 paintings have been recovered.

Kaylor was charged with trespassing and 10 counts of burglary, Manfredi said.

The initial call about a possible squatter at the home on the 3800 block of Washington Street came Saturday just before 11 p.m. When police made contact with Kaylor, he produced documents allegedly showing he was going to be the proprietary owner of the home, police said.

“This individual produced some type of paperwork that looked like it was official, saying he had a right to stay there,” Manfredi said. “It is a little sophisticated … not typical for squatters to do.”

When police were unable to reach the homeowner and sales agent, they left. But the next day, the sales agent called police and said no one should be inside.

Kaylor may have been squatting there for as long as two months, Manfredi said.

There’s a consumer alert about an apparent scam targeting families in Rhode Island after a local couple lost $13,000.

Experts say this scheme is very sophisticated, and anyone who’s in the market for a new home needs to be on alert.

It’s a simple idea: pose as a real estate agent online and target home buyers. But in reality, it is anything but simple.

“The goal is to hack into the real estate agent’s email account,” said Connor Dowd, a broker with Keller Williams Realty of Newport. “Once they’re in, they try to learn about any real estate transactions that are currently going.”

Hat tip to W.C. Varones for sending in this article on Crisp and Cole, the two real estate agents in Bakersfield who were found guilty of defrauding banks out of nearly $30 million:

FRESNO — For their roles in a mortgage fraud case that rocked Bakersfield, David Crisp was sentenced Monday to 17 1/2 years in prison while his wife, Jennifer, received what the federal judge in the case called “the break of a lifetime”: five years probation.

David, 34, was immediately remanded to custody to begin serving what amounts to the same sentence given in February to his former business partner, Carl Cole, who like Crisp had pleaded guilty to conspiracy to commit mail, wire and bank fraud. Both former principals of Crisp & Cole Real Estate and Tower Lending were ordered to pay restitution of more than $28 million.

In a news release, federal prosecutors said David had finally “crashed hard” after flaunting his “ill-gotten wealth” and going around in exotic cars, Armani suits and a private jet.

“David Crisp lived in the fast lane, steering a real estate company that was all image and no substance,” U.S. Attorney Benjamin B. Wagner wrote.

As the housing bubble burst, Crisp & Cole’s projects fell through, home defaults mounted and lawsuits were filed. By September 2007 the IRS had slapped David and Jennifer Crisp with a $111,170 lien in back taxes and the FBI began investigating. Within days, more than 75 federal agents swarmed over 13 properties related to the former Crisp & Cole company.

In his plea agreement, David Crisp admitted that he and his co-conspirators caused losses of at least $29.8 million to defrauded lenders.

The Crisps’ guilty pleas brought to 14 the number of defendants who have done so in the case.

As for the success he appeared to achieve as a young real estate mogul, Crisp told the judge, “It got to my head, your honor.”

His Fresno lawyer, Eric Kersten, portrayed Crisp as an inexperienced “kid” caught up in a booming market. Kersten tried to shift some of the blame to Cole and the bankers anxious to give out loans during the real estate boom.

“Everybody was making money. It was like the wild West,” Kersten said.

Real estate and title agencies are being warned about a new fraud scheme in which email bandits target consumers who are in the process of purchasing a home.

Jason Hidalgo from the Reno Gazette-Journal found that dual-agency short sales with a prearranged cash buyer accounted for more than 10 percent of Northern Nevada’s 2,096 single-family home short sales last year. He looked me up in February to get my thoughts on short-sale flipping, and then in his story he lays out two offenders:

Krch Realty, which triple dipped commissions on more than half of its dual-agency short sales with cash buyers last year, did not respond to a request for comment for this article.

Marshall Realty accounted for nearly a third of such short sales in 2013. Broker-owner Marshall Carrasco defended his company’s transactions and referred further questions to his lawyer, who wrote to the Reno Gazette-Journal to “proceed with caution” on any article about Carrasco.

“Mr. Carrasco and Marshall Realty have represented many sellers in short sale transactions,” attorney James M. Walsh wrote. “As noted, full disclosure is made to the short sale sellers of the nature of the transaction. Mr. Carrasco, on occasion, presents these listings to individuals or entities that he knows are interested in purchasing short sale properties.”

Investor Jeremy Page of Harcourts NV1 Realty, a key player in the area’s real estate investment scene, stressed that all his short sale deals were done within the scope of the law. Page says his short sale purchases not only took distressed houses out of the market, they pumped more than $20 million back into the Northern Nevada economy in 2013 in the form of payments to suppliers and contractors who worked on his properties, as well as real estate agent commissions.

Real estate experts say such short sales come at the expense of the average homeowners, who do not fully understand how real estate transactions work, making them easy targets. It’s a problem that’s not limited to Nevada but is seen in other states as well where agents bend the rules for profit, said Jim Klinge, broker for California-based Klinge Realty.

“Typically, the homeowners don’t even know what they signed when these sharks get into their living rooms,” Klinge said. “I have had people call me asking if they have been taken advantage of, and in every case the answer is yes, but they never asked questions.”

The practice is especially a concern in Nevada, which saw the steepest decline in home values at the peak of the U.S. housing crisis. In recent years, the FBI identified the Silver State as a prime target for short sale fraud due to its high percentage of distressed properties.

Klinge called the lax environment surrounding short sales laughable.

“Nothing is done by anybody to stop this outright defrauding of banks, servicers and investors,” Klinge said. “There is no law enforcement or industry watchdogs, so it runs unabated. When other agents see people get away with it and make 5 percent or 6 percent commissions, then the amateurs give themselves permission to do it, too. It is going to take a district attorney vigorously pursuing this until we see perp walks nightly” for it to stop.

This stuff happened in every major city in America over the last 2-4 years, and thankfully it’s mostly over. Thank you Jason for a great investigative report!

Last summer I met with an FBI agent to discuss a local realtor. I submitted 32 pages of conclusive evidence that implicated the realtor in committing 19 cases of short-sale fraud.

Though the agent said he would pursue it, I never heard from the FBI again.

Hat tip to daytrip for sending in this article from the nytimes.com:

“The I.G. report confirmed what’s been clear for quite a while — that the D.O.J. has never taken mortgage fraud seriously,” Professor Levitin said. “There is going to be no comeuppance for crimes committed during the financial crisis. This sets a really bad precedent for future crises because we’re seeing that there is going to be no deterrent effect of criminal law.”

“The report fits a pattern that is scary for a democracy, that there really are two levels of justice in this country, one for the people with power and money and one for everyone else. And that eats at the heart of what I think makes this country great.”