Our YoY home sales are in decline, and it makes you think, ‘Here we go again”.

We know that sales are the precursor, and historically prices are the last to go. But with so many different variables this time around, could it actually be different this time?

Let’s consider the changes:

During the last two local declines (1992-1996 and 2007-2009), banks were the main culprits. They were visibly foreclosing and dumping homes, which affected the whole marketplace. Regular home sellers were burdened with the lower comps, and had to give them away if they wanted to move.

But now they’ve changed the accounting rules for banks, and they don’t have to dump everything they own. In fact, they can do whatever they want now.

Remember this McMansion in Carlsbad?

BofA first began the foreclosure process in 2011, but didn’t get around to actually foreclosing until July, 2017 – six years later! Then they off-loaded it to an investor in March, without having to put it on the open market. Bernanke told bankers in 2011 not doing anything that would harm the economy, and they took him up on it!

BofA first began the foreclosure process in 2011, but didn’t get around to actually foreclosing until July, 2017 – six years later! Then they off-loaded it to an investor in March, without having to put it on the open market. Bernanke told bankers in 2011 not doing anything that would harm the economy, and they took him up on it!

I think it’s safe to say that no matter how bad any future recessions might get, we don’t have to worry about a flood of foreclosures ever again.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

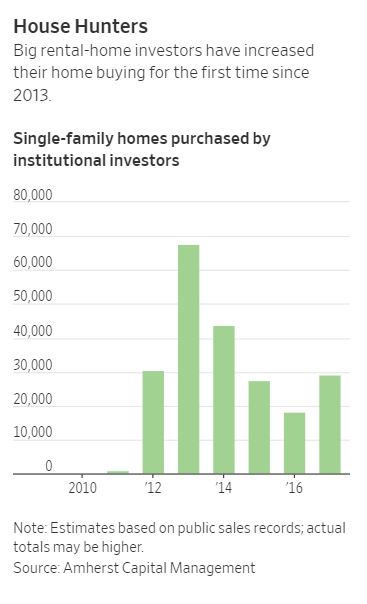

Ok, so if the banks don’t/won’t foreclose and dump, then what about the institutional investors? They are smarter and more nimble – certainly they will be selling once they sense the top!

Not so fast – according to the WSJ, investor buying is on the upswing:

An excerpt:

Wall Street is betting that more well-off Americans will want to be renters.

Wall Street is betting that more well-off Americans will want to be renters.

Financiers who loaded up on homes after the housing bust for pennies on the dollar are buying yet more—despite home prices in many markets being at all-time highs.

Their wager: High prices, higher mortgage rates and skimpy inventory are making homeownership harder. Well-to-do families who might have bought a single-family home in another era are willing to rent a house now, especially if it means access to a good school system.

The number of homes purchased by major investors in 2017 was at least 29,000, up 60% from the previous year, estimates Amherst Capital Management LLC, a real-estate investment firm that made nearly 5,000 of those purchases.

This year, investors have raised billions of dollars from bond buyers, pension funds and even wealthy Chinese individuals to purchase more homes. They have been particularly aggressive buyers in places like Atlanta, Phoenix, and other metro areas with good schools and faster-growing economies.

Cash to acquire and renovate homes has become so abundant lately that some rental investors can’t spend it fast enough. Without enough homes to buy, some investors are now building their own in popular residential markets like Miami and Nashville, Tenn.—upending a traditional pattern of Americans buying starter homes and moving up.

“The American dream no longer includes homeownership,” said Jordan Kavana, chief executive of Transcendent Investment Management LLC, a south Florida firm that has been a big acquirer of rental homes. “You will earn your equity in other ways, not your home.”

Link to Full ArticleThe big-time Wall Street investors are betting on the affluent taking over the real estate market, and turning the country into a renter’s society. It may only affect 10% to 20% of the market for now, but that might be enough to keep it all propped up.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Local flippers and ibuyers are providing another floor. Any homeowner that will sell for 10% under value today will have a host of choices to pick from. If you play it right, and have a great realtor help you, it could turn it into a retail sale quite easily!

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

The biggest threat? While there are still people underwater, today’s market has to be the most equity-rich in history. If sellers had to dump in order to sell, they could – and still make a profit.

But for there to be an extended trend of declining prices, there would need to be a series of sellers in the same neighborhood that were all in the same boat. For now, we only see an occasional dump, and it doesn’t need to be more than 10% off to attract a crowd.

With the vast majority of recent buyers having to qualify for their mortgage, and use a regular down payment in order to buy their house, you have to like the prospects of them fighting to hold on to it, no matter what. Back in the last bust, too many people got in with little or no down payment, and got stuck with exotic financing that exploded on them. Those days are gone.

We’re most likely going to live in Stagnant City, with fewer sales in most areas. But it’s not the end of the world.

Get Good Help!

“Then they off-loaded it to an investor in March, without having to put it on the open market.”

This same scheme has been going on for years which has caused big retailers to go bankrupt.

The real story when housing takes its next dump will be why didn’t anyone question where all these LLC’s came from. The banks that created them as a separate arm collected the profits and shielded themselves from failure.

I didn’t mention it this time that reverse mortgages are a new entrant in the save-a-boomer plan.

There was a change in the R-M HUD underwriting at the end of last year, and the number of reverse mortgages has dropped considerably. There is hope that private lenders may pick up the slack, but it’s such an odd mortgage I can’t see them being as big as they’ve been, unless there are lenders willing to go to 80% LTV.

“Things are different now” is the understatement of the year.

For the doubter’s, I will point out… the month of June. For those still not convinced, July promises to be just as, if not more dynamic.

We’re in the middle of the biggest social/international upheaval since World War II. NAFTA is about to be gelded, NATO is about to lose it’s welfare check, China is about to get some lessons on being a gentleman, and the WTO doesn’t know whether to sh*t or take tickets. Where’s all that extra money gonna go? Could another tax cut for Workin’ Joe be on the horizon for October? I’m gonna say “yes, trump willing!”

Meanwhile, prognosticators are trying to figure out what a typical homebuyer is thinking. THEY don’t even know what they’re thinking!

Conclusion: Just look at the Case Shiller index, plot a long term trend line if you must, and stay the course. It’s a pretty good mob indicator. Birds generally like to flock, and most people generally will run with the mob, whether it’s to their benefit or detriment, and figure out why later.

Sometimes they do figure it out. Sometimes… they never do.

https://youtu.be/RE-uhXKO-nk

Just another $1B here for buying rentals:

https://www.housingwire.com/articles/46012-progress-residential-bags-1b-to-boost-single-family-rental-business

The only thing different this time is the date and the players. The banks have actually tightened lending standards so they are much less at risk but they will have some pain. The risk is non-bank or private lenders. They will not be saved by the FED. They will liquidate once rents do not cover their costs. Trees do not grow to the sky and gravity or physics has not been suspended. Deviations from the mean will be balanced by equal and opposite reactions.

Wow Michael, that sounded so much like 2010!!

Just one more example – check the difference between 2012 and now:

http://www.mortgagenewsdaily.com/07102018_mba_mcai.asp

Do you have information on private or non-bank lenders that makes you think they have, or will have, lots of REOs?

Would you consider that the vast majority of home buyers since 2009 have bought their primary residence, and have no plans to move no matter what the value? And if there was a cataclysmic event, it’s really only those from the last couple of years who might be at risk of a price drop that could put them underwater? And that we learned a lesson from the last crash that people have to live somewhere, and just because they are underwater doesn’t mean they will sell their home?

Nobody likes making payments on underwater, depreciating assets. Accept the fact that the business cycle is long in the tooth and the RE asset bubble has been blown exceptionally large by near-ZIRP FED policy. Every monthly gain is driven by greater fool theory. Is today’s economy sustainable? Tons of cash sloshing around due to stock index appreciation…yup. Not a lot of equity cash outs like 2007…yup. However, there will be a unforeseen black swan like there always has been and all assets will decline…prob not as a far as 2008 though because we have all seen the movie before right? Except bubbles don’t repeat they echo, an we will all be surprised how this chapter ends.

“However, there will be a unforeseen black swan like there always has been and all assets will decline…prob not as a far as 2008 though because we have all seen the movie before right? Except bubbles don’t repeat they echo, an we will all be surprised how this chapter ends.”

Again, there’s a HUGE paradigm shift occurring nationally and internationally. We ain’t moved like this since WWII.

Construction guys I know are all working their asses off, and are happy campers. I know Volvo is about to open a very large factory in Tennessee. First time in America for those picky Swedes, I understand. Steel factories are ramping up. And on, and on, and on.

Everything significant going on, foreign and domestic, points to extra cash flow to the government like we haven’t seen since everyone paid off their WWII debts. I would expect the infrastructure plans that President “Shovel Ready” never got around to will start picking up at some point, owing to the need, and having the extra cash, as well as our current President’s predilection towards getting construction work done.

This is gonna be a great summer! And it’s gonna get even better! Relax, and enjoy!

https://www.youtube.com/watch?v=FkTi9T7Tg_w