Prop. 19 will reduce or eliminate some generous tax breaks that families get when property is transferred between parents and children. But it won’t change the rules for trusts themselves.

Some transfers are exempt from reassessment. Transfers between spouses are always exempt.

Another exclusion applies to transfers between parents and children, and between grandparents and grandchildren if the parents are not alive. For simplicity, we’ll assume here the transfer is from parents to children, but it also works in reverse.

Under current law, parents can transfer — by sale, gift or inheritance — their primary residence to their children and it won’t be reassessed, no matter how much it’s worth or how the kids use it.

In addition to a primary home, each parent can transfer “other property” — such as a vacation home, rental or commercial property — and exempt up to $1 million in assessed value (not market value).

Prop. 19 changes these rules on parent transfers that take place after Feb. 15 in the following ways:

- It abolishes the exemption on “other property.”

- It preserves the exemption on primary residences, but only if the child also uses the home as a primary residence and to the extent the difference between the home’s assessed value and market value does not exceed $1 million (indexed for inflation)

- If it does exceed $1 million, it will be partially reassessed, but not to full market value. If the child does not use the home as a primary residence, it will be reassessed at market value.

Prop. 19 is not retroactive and won’t apply to any property until it is transferred (or deemed transferred) after Feb. 15.

When property is placed in a trust, assessors will “look through” the trust to determine whether a change of ownership has taken place.

If it’s a typical revocable trust, also called a living trust, whoever set it up (called the grantor, trustor or settlor) is deemed to be the owner as long as that person is alive. Putting property in, or taking it out of, a revocable trust won’t trigger reassessment because the beneficial ownership has not changed.

“It’s the same as owning it” in your own name, said Chelsea Suttmann, an estate planning attorney with Barulich Dugoni & Suttmann Law Group.

When the grantor dies, however, the trust becomes irrevocable and the property is deemed to have been transferred to the new beneficiary or beneficiaries. This generally will trigger a reassessment to market value, unless it qualifies for a parent-child, spousal or other exclusion.

If this transfer takes place before Feb. 16, the current parent-child exclusions apply. If it takes place on or after that date, the new rules will apply.

If a couple sets up a revocable trust in a way that full ownership of the property transfers to the surviving spouse, it won’t be reassessed when the first spouse dies. “The spousal exclusion will apply,” said Steve Hartnett, director of education with the American Academy of Estate Planning Attorneys.

In this case, the trust will become irrevocable when the second spouse dies.

What if the trust was irrevocable when it was set up? It’s very hard to say, because these trusts are not standardized.

But in general, the county assessor will determine who is the “beneficial owner” of the property. This is generally “anyone who has a claim on income or principal from the trust,” said Bradley Marsh, a tax attorney with Greenberg Traurig. If it’s not the grantor, the assessor may determine that a transfer took place when it was placed in the trust.

In the simplest case, where parents set up and transfer property into an irrevocable trust and the first beneficiary is a child, “because you cannot revoke it, it’s a change of ownership at that moment,” Marsh said. “You would need to file your parent-child exclusion.”

Some parents are transferring investment property to their children in an irrevocable trust before Feb. 16 so they can get the parent-child exclusion before it expires.

“Because the estate and gift tax exemption is so high, they want to make that transfer now, if the parents don’t need the income,” said Yin Ho, a real estate attorney with Withersworldwide.

Parents wanting to do this should not retain any rights to the property, except possibly the power to shift assets among the children who qualify for the parent-child exclusion, Hartnett said.

Remember that before Feb. 16, the exclusion applies to only $1 million in assessed value per transferor on property other than a primary residence.

The downside of transferring assets to children now (within or outside a trust) is that the children generally will lose the step-up in basis that applies to appreciated assets when the owner dies. This huge tax benefit lets heirs avoid tax on the capital gains that occurred during the owner’s lifetime.

Attorneys say there may be ways to preserve the tax base and the step-up in basis, but they are too esoteric to get into here.

Not all irrevocable trusts convey ownership. For example, if parents put property into a trust for their own benefit during their lifetimes and thereafter for the children, “in that case the assessor would not consider it a change of ownership until the parents passed away,” Marsh said.

Some readers asked whether changing the trustee would trigger a change in ownership for property taxes. The answer is no. By the same token, keeping the same trustee won’t prevent a reassessment if there is a change of ownership. “The trustee is totally immaterial,” Ho said.

Suttmann pointed out that Prop. 19 won’t affect people who own property in a corporation, limited liability company or other legal entity. “They are under different rules,” she said.

Now I’m more confused than before. What parts of Props 60 & 90 are overwritten?

There is a lot to digest – I think it was poorly written.

Prop 19 Changes to Prop 60/90:

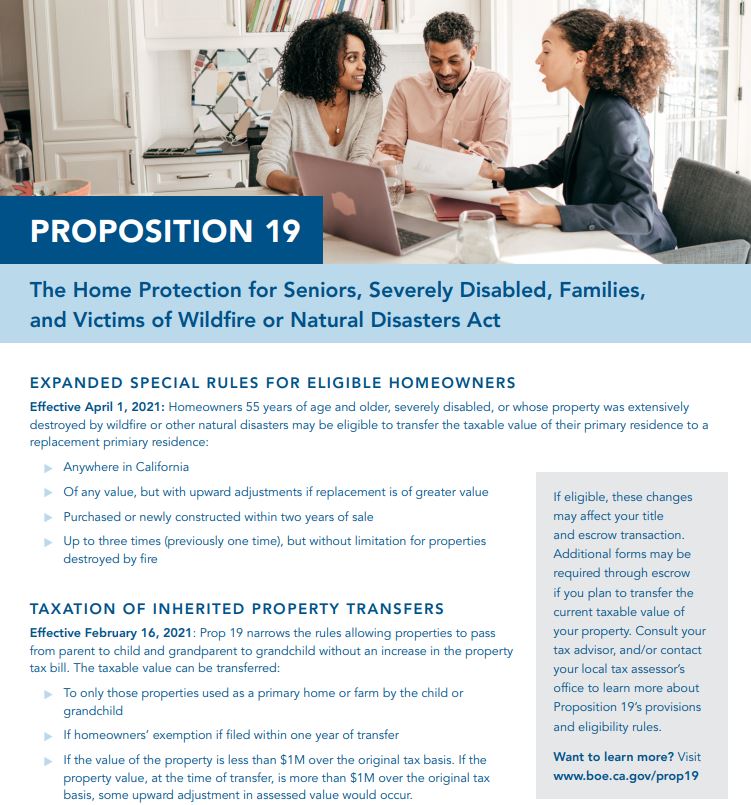

Seniors who are 55+ in age can transfer their primary-residence property-tax basis to a new primary residence purchased in any county in the state (60/90 only had ten states included).

Seniors can buy a more-expensive home, and only be taxed on the difference above the price of the home sold. (60/90 only allowed seniors to buy equal or less).

~~~~~~~~~~~~~~~~~~~~~

The inherited-property rules have changed too.

It used to be that you could inherit your parents’ primary residence and vacation home (or grandparents if parents died first) and maintain their property-tax basis. Prop 19 Changes:

1. Preserves their property-tax basis only on their primary residence (not vacation homes).

2. Only preserves their property-tax basis if one of the inheritees moves into the home as their primary residence.

For those who transfer their primary residence or vacation homes to their children prior to Feb 16th, they may dodge the Prop 19 changes for now.

But the downside of transferring assets to children now (within or outside a trust) is that the children generally will lose the step-up in basis that applies to appreciated assets when the owner dies. This huge tax benefit lets heirs avoid tax on the capital gains that occurred during the owner’s lifetime.

If the parents were on a short runway, the additional appreciation between now and their death may not be much. But if they live another 10-20 years, the capital-gains tax paid on the difference in values (today’s vs. the date of the second-spouse’s death) could out-weigh the savings on property taxes.

So what happens if your kids inherit and make it their primary but move out later and convert to rental later. Is there a mechanism to reassess if they do? I think this is where it could get dicey

Agree – how close is the county assessor going to be watching? And if their only trigger is when a new deed is recorded, will they contact the seller and ask for their tax returns to see if they rented out the home later?

What happens when the kid who inherits the home dies – does his kids get to keep the previous tax basis? It looks like it, so if they live there too – and their kids too, then the ultra-low tax basis could go on forever…..

What about putting the kids on title now?

What about putting the kids on title now?

Check with your attorney but it looks like transferring/assuming the property-tax basis would work if done before Feb 16th and you don’t mind the potential income-tax on the gift.

Here is a Google opinion on gift vs. inherit:

While you may not have to pay gift taxes on the gift, if your children sell the house right away, they may be facing steep taxes. The reason is that when you give away your property, the tax basis (or the original cost) of the property for the giver becomes the tax basis for the recipient. For example, suppose you bought the house years ago for $150,000 and it is now worth $350,000. If you give your house to your children, the tax basis will be $150,000. If the children sell the house, they will have to pay capital gains taxes on the difference between $150,000 and the selling price. The only way for your children to avoid the taxes is for them to live in the house for at least two years before selling it. In that case, they can exclude up to $250,000 ($500,000 for a couple) of their capital gains from taxes.

Inherited property does not face the same taxes as gifted property. If the children were to inherit the property, the property’s tax basis would be “stepped up,” which means the basis would be the current value of the property. However, the home will remain in your estate, which may have estate tax consequences.

Beyond the tax consequences, gifting a house to children can affect your eligibility for Medicaid coverage of long-term care. There are other options for giving your house to your children, including putting it in a trust or selling it to them. Before you give away your home, consult your elder law attorney, who can advise you on the best method for passing on your home.

https://www.elderlawanswers.com/giving-your-home-to-your-children-can-have-tax-consequences-9667

The effective date of proposition 19 is February,16, is this the recording date, or signing the document date?

It’s usually the recording date but this wasn’t the best written proposition in history!

There are actually two different effective dates:

February 16 – date for inheriting a property and moving in to preserve the parents’ low tax basis.

April 1st – Buy a replacement home and take the old tax basis with you.

If the revocable trust grantor dies prior to February 15 and gives the successor trustee the authority and power to divide the assets of the trust to the 5 beneficiaries in their discretion as allowed by the trust, and decide to give the entire house to one of the 5 beneficiaries which is the only real property asset of the trust and has a fair market value equal to that one fifth of the fair market value of the entire trust. Then would the transfer from the trust to that beneficiary which takes place after February 16 2021 also be exempt under the parent-child exclusion as it existed prior to proposition 19 because of the look through to the original transfer when the trust became irrevocably or date of death of the grantor. TIA

Good one – check with your lawyer. They are on me about not practicing law here.

Just to clarify about putting your child on title now, I own my main property with my mother as joint tenants and we want to put my daughter on title as a joint tenant as well before this proposition takes effect…so that avoids the consequences of this proposition, right ? But it is still considered a gift?

Yes plus she won’t get the step-up in basis when she finally inherits.

Check with your attorney – don’t trust that a part-time blogger knows enough.

In your answer above to John:

“February 16 – date for inheriting a property and moving in to preserve the parents’ low tax basis.”

I hadn’t heard about the date being a requirement for moving in – only for the transfer of ownership. This seems somewhat at odds with the point of transferring ownership to avoid falling under the new rules. Is this actually spelled out in the Proposition itself, or is this just how it will likely be interpreted?

Thanks!

Sue

There is likely to be a few clarifications in the coming months/years.

But the county is going to charge the full rate until they receive the form from the heir who moved in, so that date will probably matter somewhat.

I am one of five beneficiaries of my mom’s living trust and a co-trustee with a sister. None of us plan to live in the house. My mom passed away in 1998 and the house is rented currently.

How will this new law affect us. Will we be grandfathered or reassessed?

Thank you

Will we be grandfathered or reassessed?

I think you will be grandfathered. Prop 19 applies to transfers after February 16th.

But check with your tax people – they don’t want me giving legal advice here.

If my parents transfer their current primary residence to my husband and I, even after Feb 16th, and we make it our primary residence and transfer the Homeowner’s Exemption to it, would we be able to keep the original tax base? The property is less than $1M. They are still allowed to move to a new residence to claim as their new primary?

I’m not the authority so check with your attorney but you would have to inherit their property for old tax basis to transfer.

Hello,

Your blog postings are better than most of the fluff out there on this law.

Stating that it was “poorly written” is the best understatement of the year. Prop 19 intentionally gutted Prop 13 and Prop 58. There are no clarifying regulations at all, and it was sold to the taxpayers inaccurately. The 1994 taxpayers protection act was specifically intended to address “surprise” tax increases. Prop 19 should be legally challenged for violation of the 1994 Taxpayer Protection Act.

Add in the fact that it was a huge presidential election, smaller issues were swept under the carpet. Even the title of the Prop is misleading. Add in the fact that ALL court recording offices in California have been closed to the public for over a year.

There is no e-filing for recording deeds because you are required to have a ‘wet’ signature – original docs. Also, it’s not just a deed. You have to file multiple (five separate additional legal and tax forms) for your deed recording to be accepted.

I am an attorney with over 20 years of experience and I can’t figure out how anyone without a legal background would be able to navigate this process. I’ve had the following responses from various recording offices to filings I’ve submitted in the past 30 days:

– Transfer value of a Gift Deed unstated in document (Um, it’s a gift deed, for no money?) The clerk told me that I would need to document the home value. A property value assessment? No, just an estimate. But you can’t put $100. So she told me to print out the Zillow estimate of the houses’ value – as if that’s a legal document.

– Following day, I returned and another clerk told me, “You didn’t even need that.” I pointed out the clerk and she said, “Oh, I’m not surprised she didn’t give you the correct information.” The second clerk recorded the documents without any issue.

– Recorder would not accept Grant Deed to and from the same person. Owner was changing title from Nor Cal Company, Mr. Smith, sole owner, to Mr. Smith’s Living Trust. Clerk told me she would not accept the deed without a copy of the Articles of Incorporation for his single member LLC to prove that he was the only one with ownership in NorCal Company, Mr. Smith, sole owner. Yes, you read that right. Clerk rejected a deed transfer from the property owner to the property owner. Once again, there are no records of requiring corporate articles of incorporation for deed transfers.

– Recorder’s office will only take a physical check. They do not take cash, no credit or debit cards, no online payments, no e-check payments, online payments, or in person or online credit or debit cards. Only a written check is accepted. (Does anyone even use a checkbook anymore?) That is why so many of the on line filing services do not record deeds in California, but will efile any other cases, like criminal, civil, family law.

– Out of a 22 page packet, claimant failed to date by ONE signature out of 17 different signature lines on a fully complete and officially notarized document. All other 16 signatures were dated correctly. Clerk stated that she would not accept me, the attorney, writing in the date for the client “because then you are changing a previously notarized document, and that would be fraud.” She also stated because the document had been rejected, it would have to be re-notarized. So, I had to get another deed prepared and notarized for one signature on one page.

– After waiting 2.5 months, (Nov to Jan) I received a returned deed packet from Solano County Recorder’s office because the check was made for $435 (the amount on their website) instead of $465 (as they had not updated their website with the correct fee amount). The documents were filed in mid-November, and were returned by mail over a month later, on December 23rd with the check and a denial notice for the additional $35 due.

– Entire deed recording packet was rejected because the packet was stapled as one large packet of 22 pages, instead of seven separate packets. They mailed it back over three weeks later, again, refusing to process the deed.

– Another court refused to accept the filing because the signature was in black ink, not in blue ink.

I’ve been a practicing attorney for over 20 years. The process of recording deeds in the past 30 days due to Prop 19 has me pulling my hair out. Only Title Companies can e-record deeds and pay online. The average person cannot do this, attorneys cannot do this either. Joe Taxpayer will have to jump through tremendous hoops to get a legal deed recorded, in the middle of a pandemic. It’s just not right.

The additional property tax transfer statement, the additional documentation needed adds up to an additional 15 or so pages. Some signatures require a notarization, some don’t. Forms are unclear and exemptions are a rats’ maze of language.

I have been at various courthouses every day for the past three weeks working only on Prop 19 transfers. The courts are a ghost town. Due to Covid-19, court staff is not available by phone or in person. There are no clerks available to provide forms or provide assistance and the self-help center has been closed for months. Staff has not been trained on Prop 19, so they refuse to answer any questions, due to its vagueness and lack of clarity.

The idea of imposing a million dollar tax on seniors during a pandemic is terrible. Seniors are the most at-risk population in our society for death due to Covid.

Adult children are dealing with the loss of a parent, and now they are looking at over $50k in taxes coming due every year. It’s impossible for the average person.

I know that you are a realtor, and I commend you for at least recognizing the harm this will cause homeowners. Many realtors I have talked to claim they knew nothing about the provisions when the California Association of Realtors actually *wrote the Prop 19 law* and spent over $38 million dollars to get it on the ballot.

There is no legitimate legal basis to implement Prop 19 less than 60 days after it passed. Prop 19 should at least provide homeowners to actually take action to protect themselves and their kids from being financially strangled during a pandemic, while people haven’t been able to work for over a year.

In addition – the ONLY public meeting on Prop 19 through the Bureau of Equalization and Taxation, was – get this – **held at 10 a.m. on Feb 11th, the last legal day for anyone to file a deed transfer under Prop 19** Feb 16th is the actual deadline, but because of the four day weekend, the last day to file was Feb 11th.

I was up until 2 am the night before preparing multiple deed packages to drive to three separate courts on Feb 11th. My legal assistant was driving to two other courts because again, recorders require original documents and do not efile. I would love to participate in these meetings, but the timing shows its just window dressing. Sort of like the IRS holding public meetings on taxes on April 15th at noon. Ridiculous.

The public can’t object if they don’t know when these meetings are occurring. I don’t think it is coincidental that the public comment meeting occurred on the exact date the law goes into effect. There is no intent to include, educate or assist the taxpayers.

I’m telling all my clients to just sell their homes on Redfin or Zillow because the realtor fees are as much as one year of the increased taxes they created. At the very least,

taxpayers can vote with their wallets and deny realtors any commissions from this con job.

Thank you for allowing me to vent my frustration. Most people I talk to have no idea what Prop 18 actually means and seniors are devastated to think all they worked for is going to be taken away for taxes, exactly what Prop 13 was designed to protect.

(climbing off my soapbox now),

kindest regards ,

Katie Siemont

Law offices of Kathleen Siemont

701 Southampton Rd #211

Benicia, CA 94510

http://SiemontLaw.com

email: Katie@SiemontLaw.com

Almost a year and a half has passed since this law went into effect. Are there any possible solutions to this mess in the near future?

Join the Howard Jarvis Taxpayers Association. They are going to try to get prop 19 repealed maybe during calendar 2024. Prop 19 was a fraud; voters thought it would help firefighters and the voter pamphlet did not emphasize that this is a Death Tax.

I inherited a home along with my two siblings shortly before Prop 19 so we are OK as far as keeping the Prop 13 tax benefits. The home is still in a trust that our stepfather who is living has a life estate in but myself and two siblings each own a third of the home now.

I was told once that if I were to get both of my siblings to decline their inheritance I could keep their

2/3’s of the tax benefits under prop 13 if I wanted to keep the house for myself.

Any attorney’s know if that’s true or still a possibility? I’m willing to pay for a consult if that’s the case.

Thank you

Why this isn’t on the FRONT PAGE OF THE LA TIMES is beyond but also very suspicious. Kathleen Seimont should be the author !

Why isn’t there a lawsuit against all these issues? I’m so sick of all this gov’t jargon that messes up everyone’s life. Wish I was smart, I would start a lawsuit.

My brother and I inherited our parents’ home 2 weeks prior to Prop 19 going into effect. So we were safe on that one and are paying the same property taxes as they did. Phew!

We are renting the house and want to setup either a family trust or individual trust so that the property will go to my 2 sons (my brother has no children). But we are trying to limit the property tax increase as much as possible.

If we do 2 separate trusts (50% of the property in his and 50% in mine), what happens with the property taxes when the first of us dies? Will the property be reassessed? How will the property taxes be determined if only one owner at 50% dies?

If we have a family trust with the whole property in the name of the trust, what happens with the property taxes when the first of us dies? Will the property be reassessed? How will the property taxes be determined if only one grantor dies? I would think nothing would happen until both of us die, is that correct?

In the individual trust scenario, would it be better for my brother to make me the beneficiary of the property when he dies or would it be better for him to name my sons as beneficiaries, and vise versa? Are there any property tax benefits either way?