Editors know that there isn’t anything more eye-catching in real estate than talking about people losing their home. In California, lenders are required to offer every delinquent homeowner a loan modification before being able to foreclose, so those who want to keep their house will likely find a way to do it. Judging by the graph above, very few homeowners are giving it away!

Despite the declining rates and the robust economy that characterized the U.S. during the fourth quarter, the Federal Reserve’s pursuit of lower inflation has proven to be an obstacle for the American housing market.

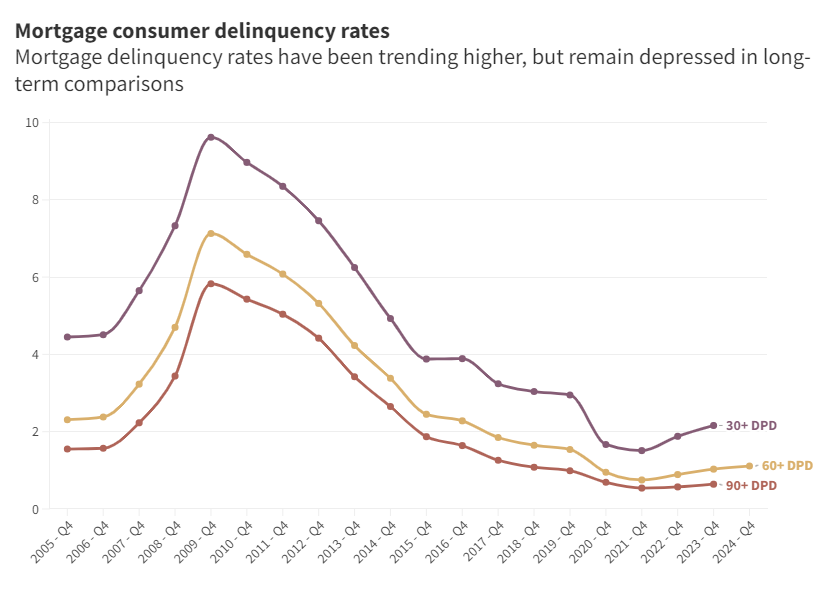

The consequence of that pursuit, which pushed up borrowing costs on U.S. households, is a 16 percent year-over-year surge in mortgage delinquencies (60 days past due), according to TransUnion’s fourth-quarter Credit Industry Insights report, exposing the growing struggle of consumers in the face of evolving macroeconomic uncertainties.

TransUnion’s report, produced from billions of updates received each month from banks, credit unions, finance companies, auto dealers, mortgage companies, retailers, student loan providers and public records, found that a total of 1.3 percent of all consumer-level mortgages in the U.S. were in serious delinquency in the fourth quarter of last year.

With roughly 84 million mortgages active in the U.S., according to data from LendingTree, that would mean about 1,092,000 Americans are more than 60 days past due on their mortgages.

While that may seem alarming to some, it isn’t nearly as bad as what happened in the aftermath of the great financial crisis (GFC) in 2008, according to Michele Raneri, vice president and head of U.S. research and consulting at TransUnion.

“We’re still in a pretty good spot, especially when you’re looking at 60 days past due,” Raneri told Newsweek during an interview on Wednesday. “So it has inched up a little bit, but it’s still not come back to what would be considered pre-GFC or probably even pre-pandemic.”

Asked whether or not the slight uptick is of concern, Raneri said, “I don’t think so. Of course, people in the industry are watching it to see if it’s becoming a bigger problem, but I don’t think that it’s something that is an indication of a bigger problem.”

She continued that the delinquency issue is not a “systemic” problem reflective of the GFC, partly due to stricter lending standards, and that back in 2008, people had “so little equity in their homes.”

Read the full article here:

The most important ingredient mentioned here is that last time people had no equity – and nothing to lose by walking away.

It’s different now.

Unless the higher delinquency rate can be attributed to job loss or catastrophic illness in the household, it seems to me that the “stricter lending standards” cited by the Transunion VP may still not be strict enough to prevent people from overborrowing.

We will never see foreclosures like 80w and 90s with loan modifications. Any foreclosures will be packaged up to large institutional investors or. Influential/unethical realtors who form LLCs with their friends to hide the true buyers. JTR will never get to bid on them like back in the day.