Dear Liz: My husband died in November 2022. I was told that if I sell the house within two years of his death, I can benefit from two capital gains exclusions, his and mine, each for $250,000. The house was appraised at $912,000 based on his date of death. I don’t imagine it would sell for much more than that now. Can you tell me approximately what I would owe in capital gains? My tax rate is 24%.

Answer: That’s a great question to ask a tax pro, since there are a number of variables involved.

If you live in a community property state such as California, then both halves of the property got a favorable step-up in tax basis when your husband died. That means the house’s new tax basis would be $912,000.

If you don’t live in a community property state, then only half of the house got the step up at his death (to $456,000, or half of $912,000). The other half — yours — retains its original tax basis. If the original purchase price of the home was $300,000, for example, your basis would be $150,000. The home’s total basis would be $606,000 (which is $456,000 plus $150,000). If you sold the house for $912,000, your capital gain could be $306,000, which would be well below the $500,000 exemption you could take if you sell the house within two years of the death. If you sell after the two-year mark, the gain above your single $250,000 exemption would be taxable.

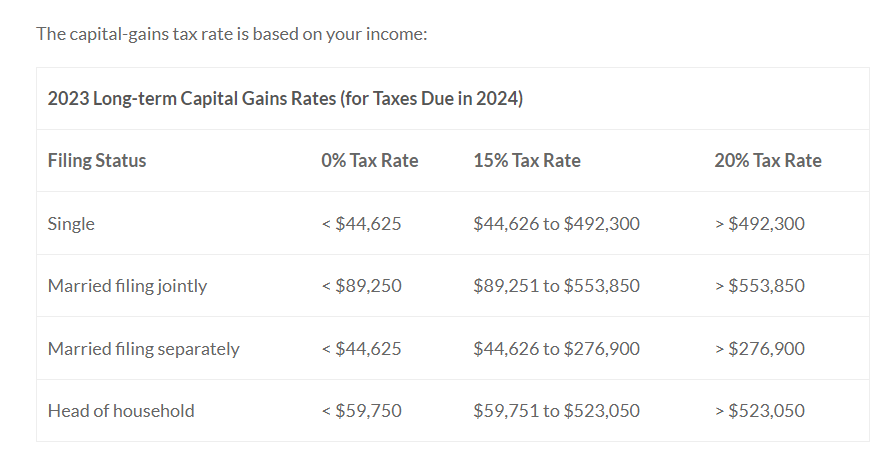

The rate you would pay depends on your taxable income and what state you live in.

For example, a single person with taxable income of between $47,026 and $518,900 in 2023 would pay a 15% federal capital gains rate, plus whatever rate their state imposes. (California doesn’t have a separate capital gains tax system, so any taxable gain would be subject to the state’s regular income tax.)

These numbers are just to give you an idea of how capital gains taxes work. Your mileage may vary. If you renovated the kitchen or did any other significant improvements on the home, those costs could be added to your tax basis to reduce any potentially taxable gain. Also, selling costs will reduce what you actually pocket from the sale and your potentially taxable gain. For more information, see IRS Publication 523, Selling Your Home.

Taxes shouldn’t be your only consideration, of course. Relocating can be disruptive and expensive. Getting the house sold before the two-year mark makes sense if you were planning to move anyway, but don’t let fear of taxes scare you out of a home that otherwise suits you.

0 Comments