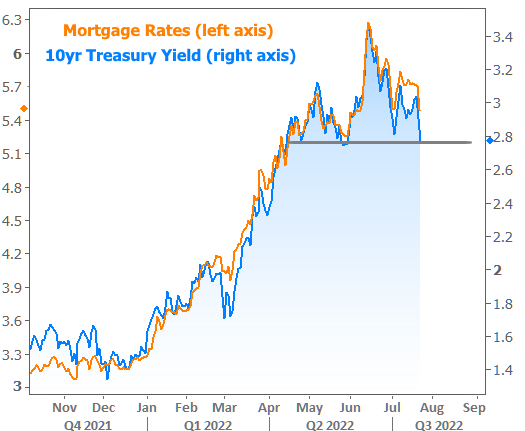

The traditional spread between the 10-year Treasury Yield and the 30-yr fixed mortgage rate has been 1.75%. Today it is 2.7%, which sure makes it look like the next Fed increase is already priced in. This week, we will see if mortgage rates will moderate and stay in the fives after the Fed bumps again!

When 10yr Treasury yields are dropping, mortgage rates are typically following, even if the proportion can vary. Mortgages definitely don’t benefit as much when it comes to overseas developments, but the sense of a big picture reversal is the same in either case. By Friday afternoon, the average mortgage rate was just a hair lower than those seen in early July. You’d have to go back another month to see anything lower.

Any conversation about big drops in rates requires an asterisk right now. Rate quotes can vary greatly depending on the scenario and the lender, but they’re not necessarily as different as they may seem. The reason is the role of “upfront costs” in the current market. Historically, it tends to make more financial sense to avoid paying additional upfront costs (aka “points”) in exchange for a lower rate. Many borrowers may still agree.

Nonetheless, points are packing a bigger punch than normal due to trading levels in the bond market, and that is having an impact on many loan quotes. For example, there are some scenarios where a single discount point can drop the rate by more than half a percent. Historically, that point would only be worth 0.25%.

There’s no universal recommendation here. If you find yourself comparing one quote to another, just make sure you’re taking the upfront costs into consideration.

https://www.mortgagenewsdaily.com/markets/mortgage-rates-07222022

I wonder if the Chinese mortgage rebellion will affect global markets? That and climate change calamities might skew traditional migration patterns. I don’t think Texas would be my first choice as a retirement destination. Interesting times…