Here is who is providing the floor to the residential real estate market:

Wall Street has made a mountain of money available to house flippers, and selling move-in-ready rehabs has rarely been easier. The challenge is finding beat-up and out-of-date properties that can be renovated and resold for a profit.

“Investors like me, we’re like ants on a sugar hill all fighting for the same projects,” said Ed Stock, who started fixing and flipping houses on New York’s Long Island after the 2008 mortgage meltdown. “It’s the greatest time to be in this market; it’s just hard to find the inventory.”

Foreclosure moratoriums have shut off a big source of fixer-uppers since last spring’s lockdown. Meanwhile, competition is stiff from regular home buyers armed with superlow mortgage rates and inspired by cable-TV renovators. Rising costs and limited availability of labor and building materials, such as lumber, cut into profits and stretch out jobs.

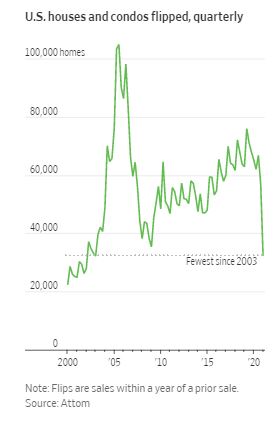

Just 2.7% of home sales were flips—sales within a year of a prior sale—during the first quarter, according to property data firm Attom. That is the lowest portion of sales since at least 2000, when Attom started counting flips. The number of flipped houses and condos were the fewest in a quarter since 2003.

That was two housing booms back and long before measured-in-months loans to house flippers became some of the hottest properties on Wall Street. Mortgage trusts, pensions, hedge funds, private-equity firms, investment banks and insurance companies all want so-called flip loans, drawn by yields in the range of 8% to 12% at a time when one-year Treasurys pay less than 0.1%.

Mr. Stock’s lender, Roc360, last week received a $2 billion infusion from insurer Athene Holding Ltd. to make more loans to house flippers as well as landlords, who buy a lot of rehabbed houses. Arvind Raghunathan, Roc360’s chief executive, said his firm would have little trouble raising several billion more given the hunt for yield that has sent investors into less-familiar pockets of fixed income.

“These notes have done extraordinarily well the last eight years,” Mr. Raghunathan said. “There have been hardly any losses, and 8% for one-year paper is extraordinary.”

Many flip loans are repaid even sooner, allowing investors to recycle their capital by lending anew or buying additional loans to boost returns.

New York Mortgage Trust Inc. said it ramped up its investment in flip loans last fall and ended June with $622 million worth, carrying an average coupon of 9.33%. The firm bundled $167 million worth of loans into two-year securities, sold them to other investors and expects that replacing repaid loans with new notes before the securities mature will produce returns in the high teens or low 20s.

“There’s not many markets where you could achieve that type of return,” the firm’s president, Jason Serrano, told investors last month.

Toorak Capital Partners, which has been buying flip loans and pooling them into securities since 2018, in June sold a $339.5 million security, its first deal since before the pandemic. To supplement the scarcer house flips, CEO John Beacham said Toorak has been buying loans that fund renovations of small apartment buildings. There is much less competition for these than houses. Additionally, the firm is bundling longer-term notes to rental-house investors, who have accounted for more than 1 in 5 home sales in some of the country’s hottest markets.

“We’ve seen a lot of competition come into the space,” Mr. Beacham said. “It’s hard for investors to find deals in a lot of places.”

On Long Island, Mr. Stock works his real-estate connections and estate-sale scouts to find deals before they hit the market. He looks for houses that need so much work that they won’t qualify for typical government-backed mortgages. Such homes have become hard to come by in the working-class neighborhoods where he used to do most of his flipping. So he has moved up market and into new areas, such as the Hamptons, where more people are living year-round, and even Florida.

Mr. Stock expects to do about 15 flips this year, well below the 53 he undertook in 2014 when foreclosures flooded the market. Most houses he buys are gutted to the studs, windows and roofs replaced, plumbing and electrical systems brought to code, mold remediated. Walls are knocked down and floor plans opened. Marble countertops, stainless steel appliances and other modern trappings are installed.

Roc360 finds flippers such as Mr. Stock with a team of data scientists who sift through public property records for houses that have been bought and quickly resold for gains. Once the people behind profitable flips are pinpointed, Roc360 targets them with advertisements and on social media, offering cheaper financing and deals on property and casualty insurance, appraisals and at home-improvement retailers.

“These are highly entrepreneurial crews,” Mr. Raghunathan said. “People who have really learned to keep their costs down and keep churning.”

Mr. Raghunathan, who has a doctorate in computer science, and others started the firm in 2013. It seeks to adapt the sort of technology his team at quantitative-trading hedge fund Roc Capital Management used to pick stocks and bonds to find the best borrowers in the realms of flip and rental houses.

Since it began, Roc360 has funded about 15,000 loans, which average roughly $350,000. This year, the firm expects to lend $3 billion and with the Athene investment plans to boost its output to more than $4 billion in 2022, he said.

https://www.wsj.com/articles/wall-street-cant-get-enough-fixer-upper-houses-11631007001

0 Comments