When I made the comment that people are soft, it was because I was thinking about the guy who came to the open house and said he would have bought it…..except for the power lines.

If he had issues with the house, yard, etc. and the power lines were just one of the objections, then fine.

But are you going to pass on an otherwise perfect house because of power lines that are a 1/2 mile away? They don’t have flashing lights on them, and they are far enough away that you won’t hear any buzzing. With the hill behind them, they blend into the landscape – and once you move in and life takes over, you probably won’t notice them much at all.

Why should you compromise?

Because other people are compromising in order to actually buy something – it’s what happens once you realize that you’re probably not going to find a perfect house.

What if prices came down 10% to 20%? Wouldn’t that mean the chances would improve?

I guess yes, technically, the odds would be better. But if you did find a perfect house, you’d have to beat out the other buyers to win it, which will probably take over-bidding by 10% or more.

Look at the featured La Costa house of the week. It didn’t have a full bathroom downstairs to go with the 4th bedroom, but that didn’t stop ten people from making an offer. Or think of the buyers of my $7.75M listing in La Jolla. They had to live with three staircases and a one-car garage and they still paid $800,000 over the list price.

Why compromise? Because it shortens your timeline, and makes the process more manageable.

If you are looking for any reason NOT to buy a house, then you are one of the non-compromisers – which is fine. But have you noticed that every house seems to have an issue, and there is no telling when you will find the perfect home….if ever? You may never buy a house!

Instead of looking for one reason NOT to buy, be intent on finding reasons TO buy the house.

Know that every house is probably going to need at least $25,000 to $50,000 in upgrades, so look for those first, and get them out of the way. Then if you can find a house that just has more positives than negatives, you’re doing good. If positives outweigh the negatives by 3-to-1 or more, you got a winner!

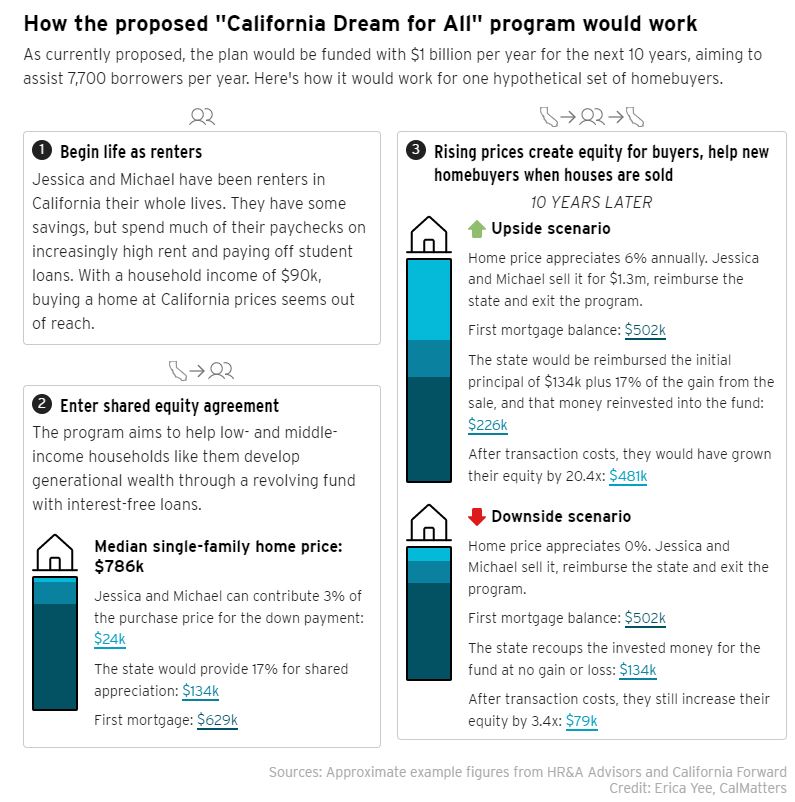

More on one of the proposals to spend the state’s budget surplus. It doesn’t make the homes any cheaper, so home buying will still be limited to the affluent who can afford the payments:

First-time buyers often rely on family gifts to afford the down payments on their homes. Now California Legislators want the government to fill the role of generous relative.

Lawmakers are proposing creating a billion-dollar fund in this year’s state budget that would provide California’s first-time buyers either all of the money they need for a down payment, or very close to it, in exchange for partial ownership stakes in those residences.

Atkins said the California Dream for All program is aimed at creating opportunities for lower- and middle-income buyers in a rapidly rising market, including those who have faced racial and economic barriers to homeownership.

“The California Dream for All program will give more people the chance to break free from the cycle of renting,” Atkins said last month. “This has the ability to change people’s lives.”

The proposal is the subject of negotiations between the Legislature’s Democratic supermajority and Gov. Gavin Newsom, also a Democrat, on how to spend a projected budget surplus of $97.5 billion. The legislature passed a budget on Monday that includes the proposal, though negotiations with Newsom continue on a final overall spending plan.

A spokesman for the governor declined to comment on the proposal, citing the ongoing negotiations. It was not included in the governor’s original budget nor in his May revised budget.

The housing proposal – which would call for issuing revenue bonds of $1 billion a year for 10 years to create the fund — is the largest in a slew of proposals intended to promote homeownership this year. The proposal also includes $50 million in the budget this year, and $150 million per year after that to pay for the administrative costs of the program and the interest costs of the revenue bonds.

The program envisions helping some 7,700 borrowers a year, according to estimates made by the program’s designers based on home price projections. A start date for the proposed program has not been indicated.

It is a true honor to have listed for sale my favorite home of all-time!

365 Marine St., La Jolla

3 br/3.5 ba, 2,894sf

YB: 2018

LP = $6,950,000

This custom contemporary was designed and carefully-crafted for over three years to be the ultimate beach house just 100 yards from the sand! The main living area has floor-to-ceiling glass panels that open dramatically to create the perfect indoor-outdoor experience with breath-taking 180-degree ocean views over Marine Street beach! The interior is loaded with so many custom features that they make this home downright sexy! Ample off-street parking and an easy walk to the village too. Architect Mark Morris said in his 20+ years of designing super-custom modern-contemporary homes in the area, this is his favorite project of all-time. The ultimate in modern contemporary design – it’s a trophy property!

A top California lawmaker is proposing to spend $10 billion to help families buy homes in the state with some of America’s highest housing prices.

Democratic State Senate Leader Toni Atkins on Wednesday unveiled details of a proposal she’s pushing to create a revolving fund that would provide interest-free loans for up to 30% of the purchase price of a home for low- and middle-income households.

If implemented, it would be the largest program of its kind in the nation, according to the people who designed it. Proponents hope that it will be included in the state budget that must pass by June 15 and go into effect as soon as January. The aim is for it to eventually help about 8,000 families a year.

The proposal calls for the state government to share in any appreciation in the value of houses it helps purchase when they are sold and then invest those proceeds back into the fund.

“The purpose of this is to create a long-term endowment,” said Gene Slater, chairman of CSG Advisors, which advises public agencies on affordable housing and helped design the program. “We’re investing in the future value of the home so we can help other people.”

Under the proposal, California would spend $1 billion a year for 10 years. Participation would be limited to households making 150% of the median income in an area. There would be limits tied to a region’s median home price allowing home buyers in the most expensive markets such as the San Francisco Bay Area to benefit.

In Los Angeles County, households earning up to $120,000 a year could qualify for assistance, while in low-income areas like the agriculture-heavy Central Valley, that number would be closer to $107,000, according to data provided by the researchers who drafted the framework. Proponents want to target certain groups through outreach, including residents of largely Black and Latino neighborhoods and those with high loads of student debt.

The homeowner would repay the loan when they sell or refinance the home, along with a cut of the profit from any appreciation in value based on how much assistance the state provided. If the home price declines, Mr. Slater said, the state would be repaid if money is left over after the purchaser pays back their mortgage loan and recoups their portion of the down payment.

The program would be limited in scope to cover only about 2% of home sales volume statewide in an effort to avoid pushing prices higher.

Participants would be chosen on a first-come, first-served basis, with slots set aside for certain geographic areas and income brackets.

To become law, the proposal would have to pass both chambers of the Democratic-controlled state legislature and be approved by Democratic Gov. Gavin Newsom. A representative for Mr. Newsom declined to comment on the pending legislation. In a statement, Assembly Speaker Anthony Rendon praised Ms. Atkins’s work on the issue but didn’t say whether he supported her proposal.

When people are looking for the perfect ‘forever’ home that will last them for a lifetime, any additional cost isn’t going to phase them – or at least it won’t affect the affluent folks. Most are making it up elsewhere when they sell their previous home or rental properties, inherit big money or receive a gift, and/or sell their businesses/stocks or other assets and just want a trophy property.

If they weren’t bothered by home prices rising 60% to 80% over the last two years, a measly 2% increase in the mortgage rate isn’t going to stop them.

Like most real estate talk, half of this is horsepucky:

Don’t Let FOMO Drive You

Just because everyone is buying a house, doesn’t mean you should be too, said Donald Olhausen Jr., owner of We Buy Houses in San Diego. “I have seen many people force bad decisions because they have fear of missing out (FOMO). Forcing a bad deal will not rectify itself because there were no other options or because you felt stuck. Being patient in this market is hard, but overpaying for a faulty property will ultimately lead to more regret.”

There Are Markets Within Markets

There is not one universal housing market, but rather “many smaller micro-markets,” said Michael Shapot, Esq., licensed associate real estate broker. “Some of those submarkets are ‘hot, less hot or more hot’ and they may change week by week, or month by month.”

Elisa Uribe, a realtor with Wells and Bennett Realtors added that “real estate is hyper-local,” so consider the source. “You can withstand any market changes if you don’t have to move in a specific time frame.”

2022 Is a Slightly Better Time To Buy

Real estate experts like Marina Vaamonde, the founder of PropertyCashin, said that 2022 would be a better time to buy because, “The demand for residential real estate is still vastly overshadowing the inventory.”

Indeed, now that 2022 has arrived, experts still agree that is the case, even with decreasing inventory. According to Time, home prices will not increase as rapidly and home values will also likely increase at a less vigorous rate than the peak of 2021, which bodes well for buyers.

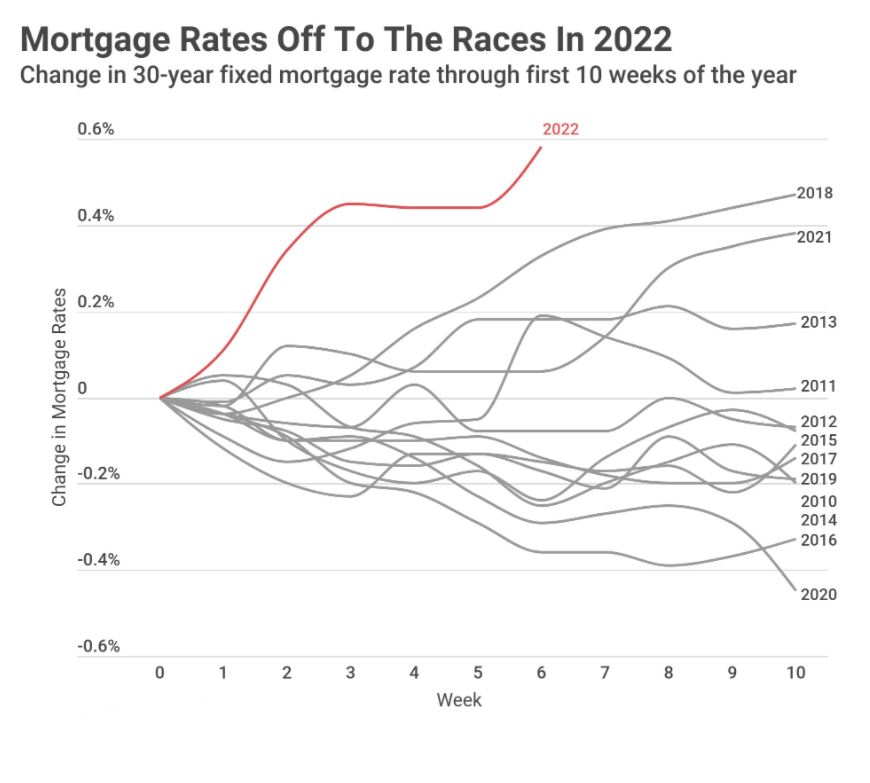

However, the Fed Just Raised Interest Rates

What made 2021 unique was extremely low interest rates, according to David Friedman, CEO of investment property platform Knox Financial. “There have been very few times in history when we’ve seen 30-year fixed mortgage rates hovering around 3.3% and 15-year mortgage rates slightly above 2.6%,” he said.

However, on March 16, 2022, The Federal Reserve raised rates for the first time in years by 0.25%. What this likely means, according to NerdWallet, is that mortgage rates will follow suit by increasing, meaning homebuyers will pay more in interest.

No One Can Predict the Next Drop

Despite these slight increases in interest rates, and decreases in inventory, this doesn’t necessarily mean the market is going down.

Khari Washington, a broker and owner of 1st United Realty & Mortgage, added, “No one knows if the housing market will drop and when it will drop. Most reports talk about the market slowing in 2023 but not falling. Builders have not built enough housing and interest rates remain low.”

“The right time to buy is when a person is ready,” adds Washington.

Don’t Wait for a Better Price

Waiting can be a gamble, said Jeff Shipwash, CEO of Shipwash Properties LLC. “You could be waiting to purchase with the thought of prices coming down, but…even if home prices do pull back some, if rates increase it will all be for nothing. You may be able to afford a $300,000 house at current rates. But if those rates increase by 1% while you wait, that same payment may be on a $250,000 house.”

Rents Are Sky High

If not buying means renting, consider that “the current rental market is on fire with rents skyrocketing and landlord incentives eliminated,” said Shapot. Renting will not be a cheaper option in the long run.

This Market Is Stable

Unlike the unstable market leading up to the economic crash of 2008, this market is stable, said Jennifer Shannon, a broker associate with Keller Williams Realty. “This market run-up hasn’t been driven by investors, flippers and bad mortgages. It’s been driven by legitimate buyers who are more free to determine where they live than ever.” While demand will start to slow eventually, she says there are no indicators of prices going down anytime soon.

You’re Ready When You’re Ready

“You’re ready to buy a home when you’re ready, not when there’s a frenzy,” said Tabitha Mazzara, director of operations at mortgage lender MBANC. “The frenzy is a seller’s market, so missing out on a frenzy is a good thing for buyers.”

Chase Michels, owner of Compass, The Michels Group, added, “If a client is fully committed to buying and is in the appropriate financial position to do so, then they should be looking. You may buy at a little lower or higher price at different times of year but that is typically unpredictable in a smaller market.”

I guessed that we’d have 5% more NSDCC sales this year because I expected a surge of delayed sellers who would finally come to market in order to cash in on the record pricing.

But it’s not happening, at least not yet.

The number of NSDCC listings for the first two months of the year is 32% BELOW last year! It means buyers are only going to have a few shots at winning a home.

Here’s what home buyers will have to endure in 2022 to succeed:

Long Waits – Days and weeks will go by without any quality new listings to review. It makes you soft and it’s difficult to keep your chops up.

Coming Soon – Listing agents will tease you by advertising a home for sale, but you can’t see it yet. It’s not always clear when you can see it, and you better not miss the date because…..

Quick Exposure – Once the listing agent is willing to show the house, they will be overcome with the demand, and will likely hit the panic button.

Many will insist that you show them a bank statement and pre-approval letter just to see the house! If you get an appointment, it will be limited to a 15-minute period that is convenient for the listing agent AND be subject to cancellation prematurely because they already took an offer before your scheduled time. Hopefully, you don’t have a job or other responsibilities that limit your scheduling. You will get the feeling it is best to quit your job so you can devote your entire life to home-buying.

No Transparency – If you want to buy it, then just make an offer and you will hear back in a few days.

Over Pay – Not only will you have to pay well over the list price to win, but there won’t be any recent sales to justify any of it. The logic and common sense you usually employ will be your enemy here.

Waiving the Appraisal – What was once an insider trick to improve an offer has turned into a standard on every deal. If you refuse, the listing agents will think you aren’t a serious buyer, and move on.

Shorten the Contingency Periods – You will have 7-10 days to sign off all contingencies. You will need to have a great home inspector on speed dial and who can schedule quickly.

60-Day Free Rentback – Listing agents demand free rentbacks whether the seller needs them or not. Those homes that provide immediate occupancy is a bonus for which buyers will pay extra.

No Repairs – Most buyers are submitting a blank repair-request form with their initial offer.

In spite of all those hurdles, there will still be stiff competition for the quality buys. Once the listing agent has collected enough offers that fit the criteria above, they will then huddle with the sellers in the back room and decide on a winner. This is where having a great agent with a good reputation in the community will pay off. Discount agents, out-of-town agents, buyers who are agents, and agents who don’t look good or don’t smell right are ignored and/or sent to the back of the line.

If you can endure that much and successfully get into escrow, you will be treated with disdain and disrespect that makes you will feel like a suspect, not a valued buyer. The contempt that listing agents have for their prey is palpable – they don’t trust that their initial mistreatment of you will be enough of a lesson, and they will keep it coming because they think that’s their job.

And get this – you will probably lose a few bidding wars before you get up to the desperation level of the other buyers. Oh, you’re not desperate? Then this market probably isn’t for you.

Give it a try and you might get lucky. But if you want a quality home in a good area, then don’t be surprised if the desperation among the competing buyers is higher than you could ever imagine.

The Super Bowl is complete, and the spring selling season begins today!

Judging by the quick jump in the total number of pendings, homebuyers aren’t waiting around. Mortgage rates have risen faster than any time in the last dozen years, and the number of homes for sale is scary low:

There was heavy activity over the weekend, and on the hot buys, the offers seemed to be starting at 10% over the list prices – which is now the new normal. Waiving contingencies and giving sellers free rentbacks for 60 days will be part of the landscape for the next few months.

Will rising rates cool off the market? Only for those who are on the fringes and sensitive to payment shock. The affluent – the buyers who are controlling the market – are less impacted, and a measly 1% rise in your loan rate only changes the payment by $1,116 per month on a $2,000,000 mortgage.

How long will the 2022 frenzy last?

It should stay hot until one of the following happens:

Mortgage rates hit 5%

A flood of inventory

Mid-summer

By summertime, the pool of highly-motivated buyers should be diminishing, and we’ll be left with those who haven’t been willing to pay these prices. Remember that when you see another crazy-high sales price, there was only one buyer who was willing to pay that much – the rest all wanted to pay less!

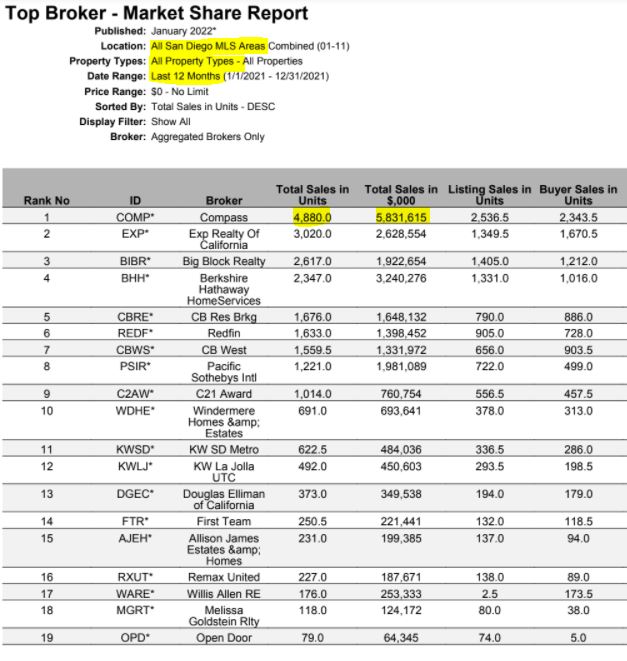

I screwed up the national rankings the other day. Donna sent me that clip but it was the 2020 list, not from last year. Anyway, who cares about the national – real estate is local!

In just 3+ years, Compass has become the dominant real estate brokerage in San Diego County, and it’s not close. Even if you add the two CBs together, our volume last year was almost double any other brokerage.

How will this affect consumers in the future?

As buyer-agents are phased out over the next 1-2 years (and it could happen sooner), there won’t be a need for the MLS. Inputting our listings onto Zillow will become voluntary, and only used if the homes can’t be sold in-house.

It will be just like the commercial side of real estate, where all the good deals are kept in-house, and only when they don’t sell, are the listings inputted onto LoopNet.