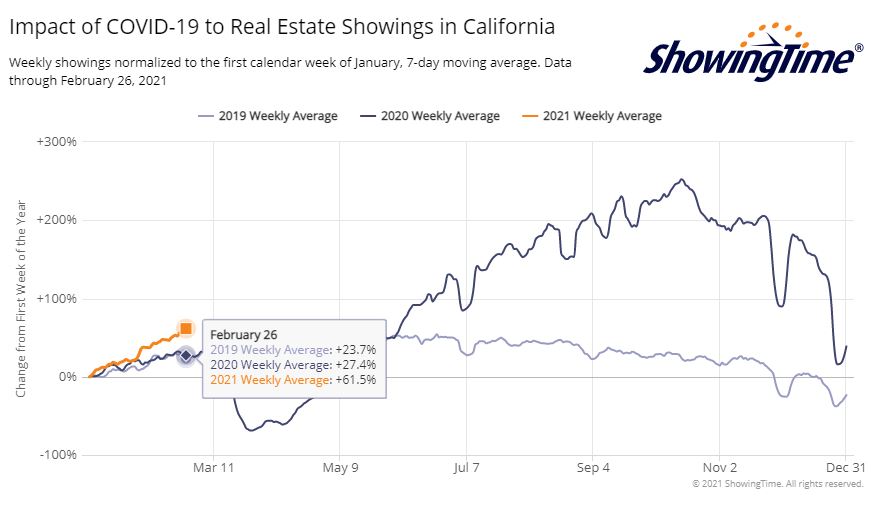

by Jim the Realtor | Feb 27, 2021 | Market Buzz, Showings |

No surprise here, given what we see in the market today.

But interesting that 2021 is off to 2x the start we had last year – which was pre-covid! New listings are down 20% to 25% while twice as many people are looking!

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

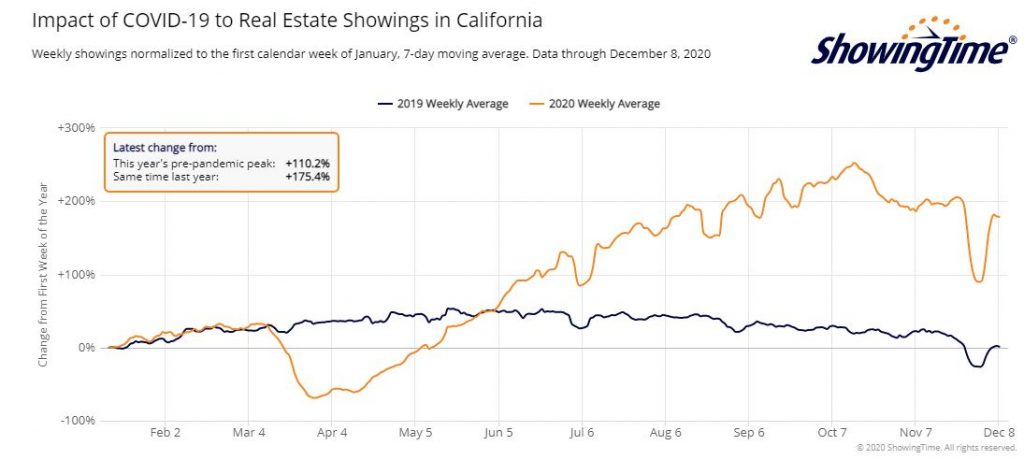

by Jim the Realtor | Dec 17, 2020 | Frenzy, Jim's Take on the Market, Showings |

Two weeks from today, the year 2020 will come to an end.

We are heading into 2021 with a strong surge of buyer interest. In spite of the current active inventory being far less than it was in 2019, there are more than twice as many people looking at homes today.

It has to carry over to next year! Hopefully there will be something to buy.

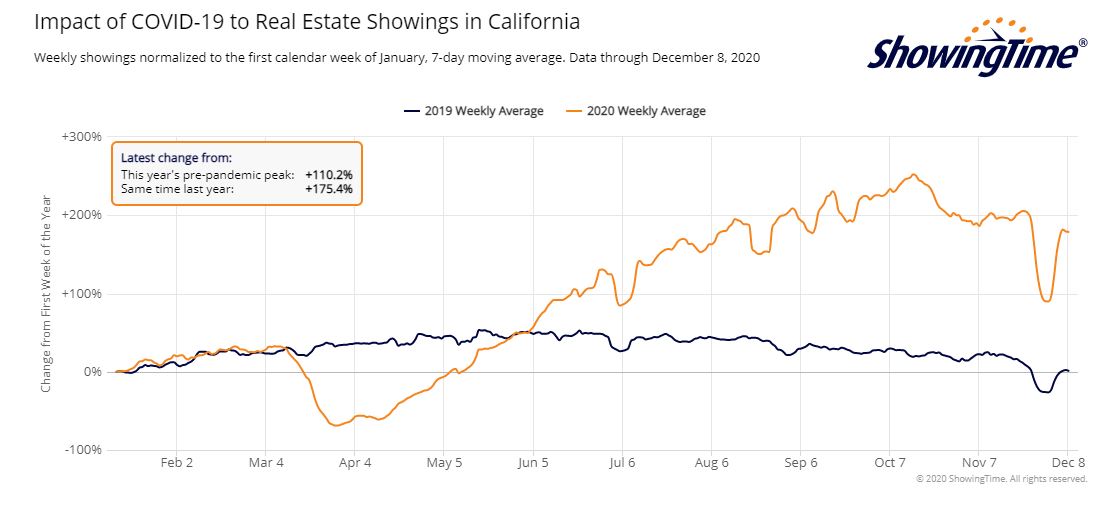

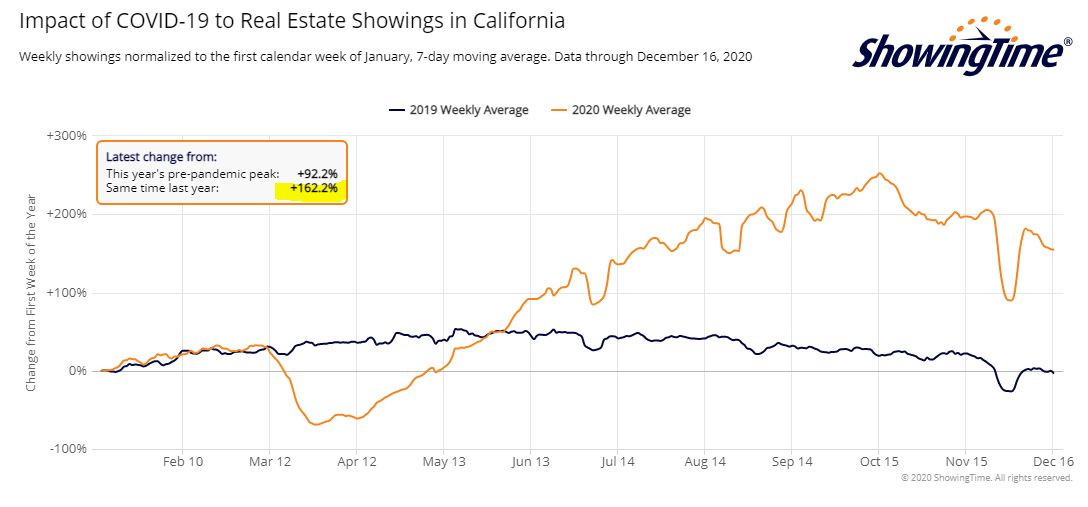

by Jim the Realtor | Dec 9, 2020 | Jim's Take on the Market, Market Surge, Showings, Virus |

Last year, the showings in early December ended up about where they were during the previous January. But this year we had a huge post-Thanksgiving bounce, and are now 175% above the same time last year!

Next year is going to go nuts!

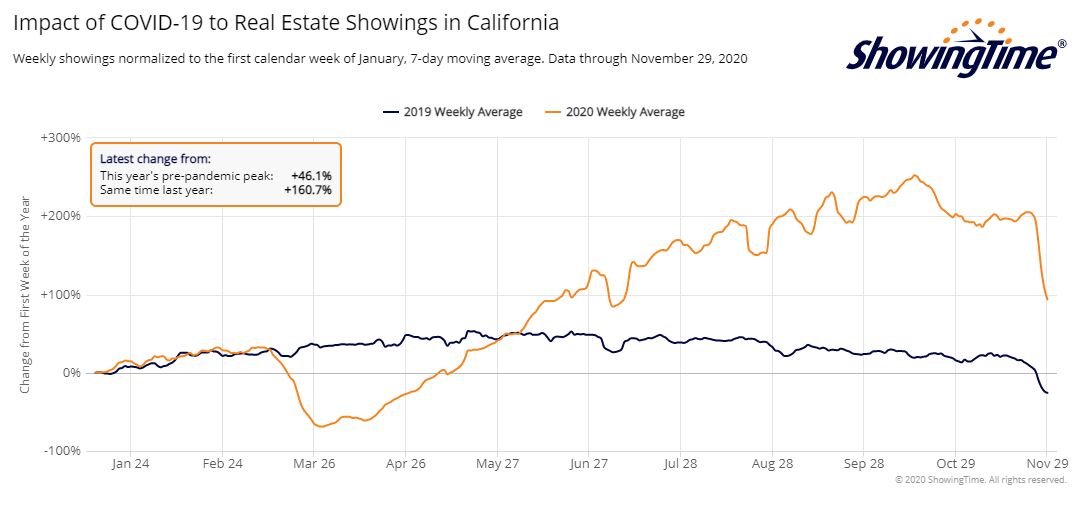

by Jim the Realtor | Nov 30, 2020 | 2021, Jim's Take on the Market, Market Surge, Showings, Virus |

This looks like a dramatic drop-off in showings but we are still 160% above where they were last year, and way above where they were in February. If there were just more homes for sale!

We got off to a hot start in 2020, and you can see how showings in January of this year picked up immediately compared to November, 2019. Let’s compare the December showings over the next few weeks to give us a feel for how fast the market will get started next year!

https://www.showingtime.com/impact-of-coronavirus/

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

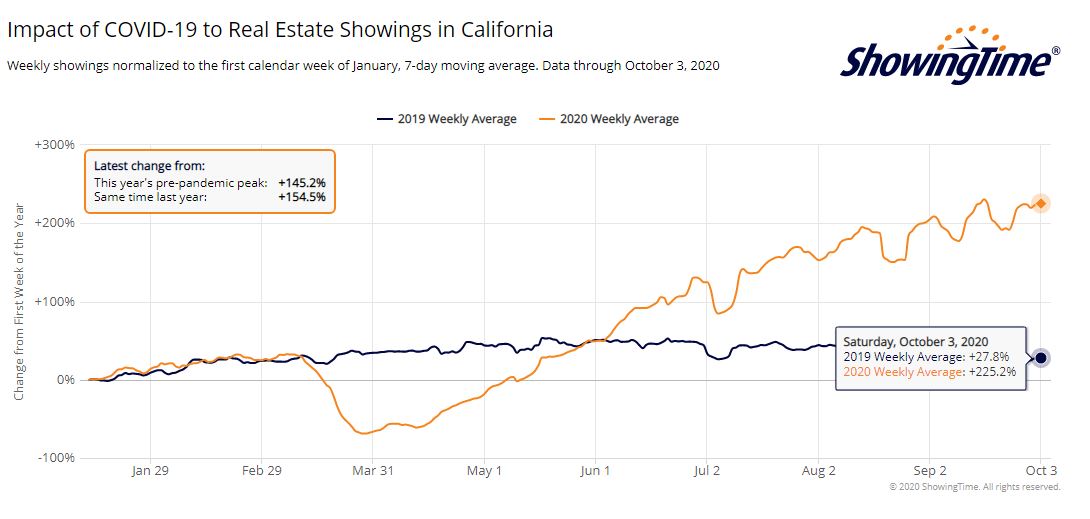

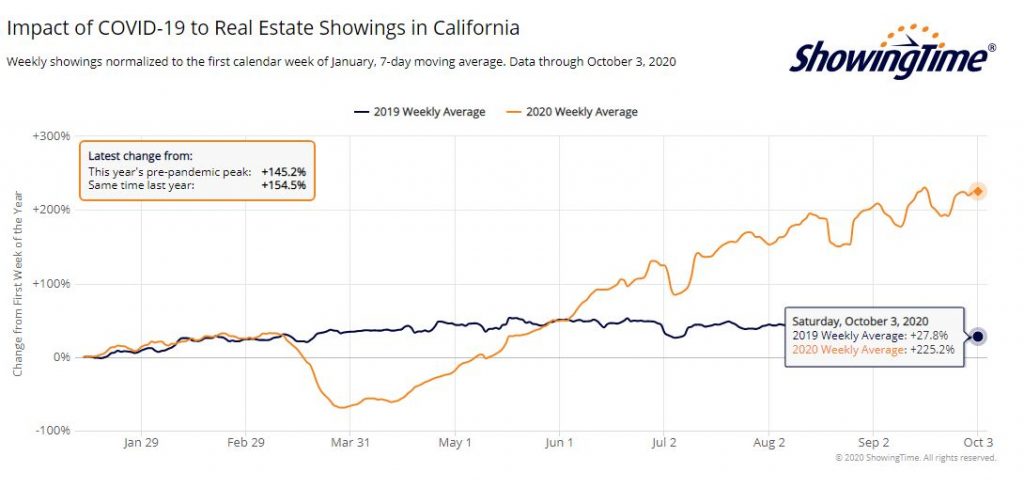

by Jim the Realtor | Oct 5, 2020 | Jim's Take on the Market, Market Buzz, Market Surge, Showings, Virus |

Click to enlarge

Not only does the current level of showings make up for the dip we had at the beginning of the Covid-19 market, but the 7-day moving average was higher on Saturday than all but two days this year (now 225% higher than it was during the first week of 2020).

As long as mortgage rates are under 3%, people will be looking!

https://www.showingtime.com/impact-of-coronavirus/

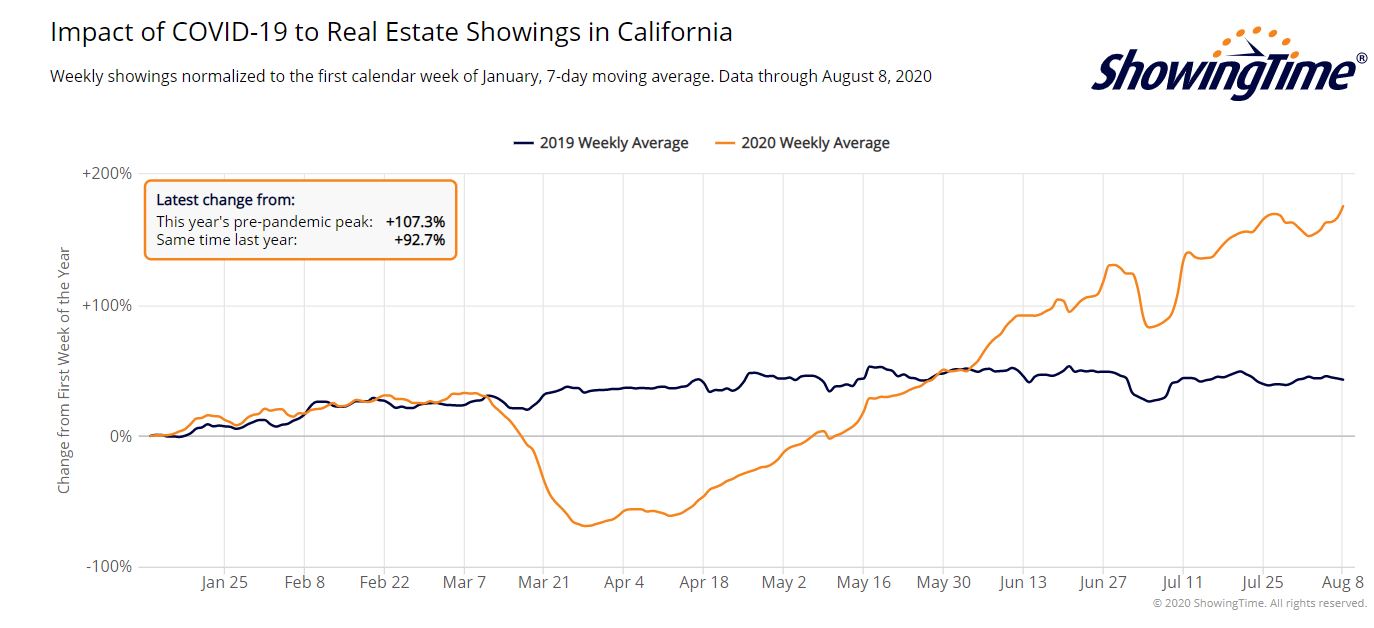

by Jim the Realtor | Aug 9, 2020 | Jim's Take on the Market, North County Coastal, Sales and Price Check, Showings |

Not only are there 92.7% more showings this year than on 2019, but this has to be the most people looking at homes for sale in the history of California!

Has there been a surge of new inventory lately?

Locally, the number of new listings has been normal:

NSDCC New Listings Between June 1 and July 31:

2017: 856

2018: 925

2019: 903

2020: 918

There are just more people looking than ever, and it’s translating into sales.

Our July count of NSDCC closed sales is up to 347, which is 23% higher than in July, 2019.

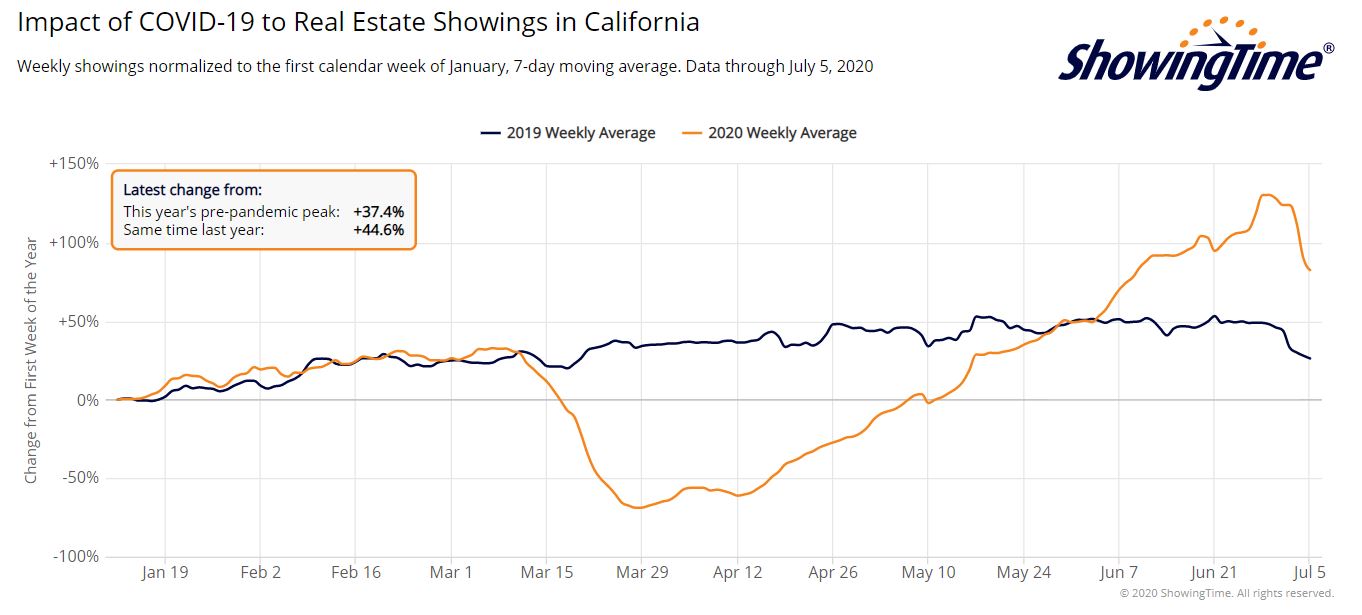

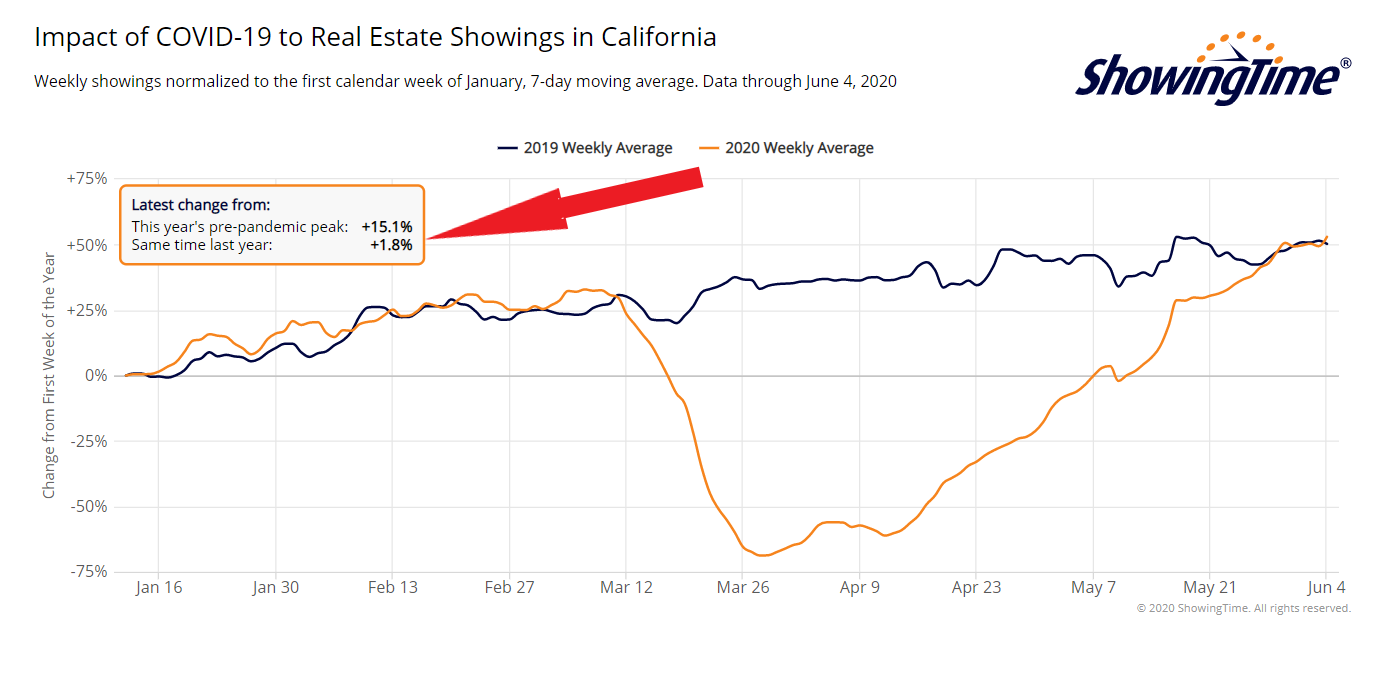

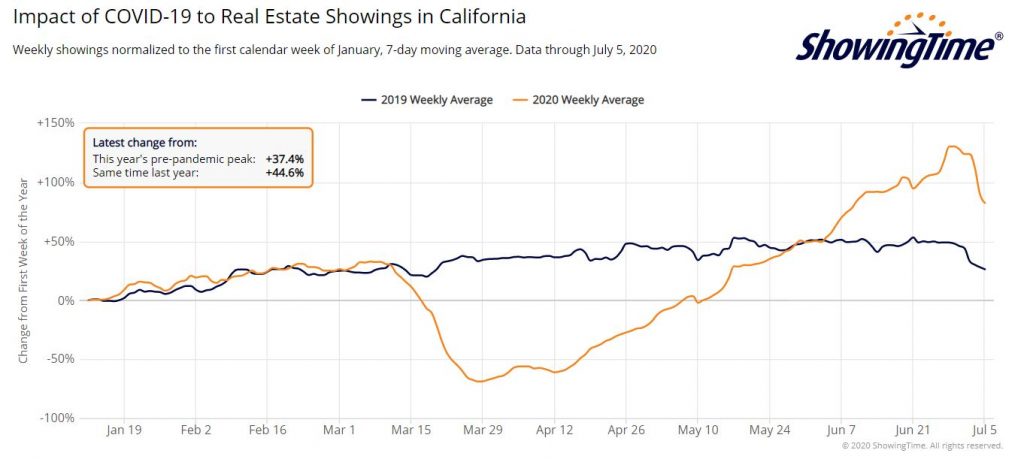

by Jim the Realtor | Jul 6, 2020 | Jim's Take on the Market, Showings, Thinking of Buying?, Thinking of Selling?, Virus |

I’m not alarmed here with a statewide drop-off in showings:

- Showings are 37.4% above those in early March.

- They are way ahead of last year!

- It was going so good that a drop-off was inevitable.

- Showings declined this time last year too – might be seasonal.

If you would have predicted this market bounce-back in April, nobody would have believed it!

by Jim the Realtor | Jun 5, 2020 | Interest Rates/Loan Limits, Jim's Take on the Market, Market Surge, Mortgage News, Mortgage Qualifying, Showings |

Just like the price of gasoline, mortgage rates are very slow to come down, but they tend go up like a rocket – and with the surprising employment news today, we’ll probably get back into the mid-3s by Monday. We’ll see if the lowest rates in history were the sole reason why showings rebounded so quickly. From cnbc:

What’s good news for the U.S. economy is suddenly bad news for mortgage rates. A far-better-than-expected May employment report only added to a growing sell-off in the bond market, pushing yields to the highest level since March. Mortgage rates loosely follow the yield on the 10-year Treasury.

Rates have been rising this week, after sitting around a record low for the last two weeks. Friday, the average mortgage shopper may see rates on the 30-year fixed as much as a quarter point higher, according to Matthew Graham, COO of Mortgage News Daily, which runs daily averages from lenders.

For those with top-tier credit and financials, they may only see an eighth of a point increase, but for those with lower scores and down payments, the jump could be as much as 0.375%.

“It’s going to be ugly,” said Graham. “Today is the first time since the Covid-19 market reaction settled down in March that interest rates truly have a reason to panic. Until further notice, this looks like liftoff.”

This is not, of course, the last word in a mortgage market that has been on a rate roller-coaster ride fueled by a massive spike in mortgage delinquencies, an initially confusing and risk-ridden government bailout, and an overstressed loan servicing system. The mortgage bailout has been clarified, with parts rewritten to help servicers, the number of borrowers in forbearance plans is shrinking and mortgage companies are on a massive hiring spree.

(more…)

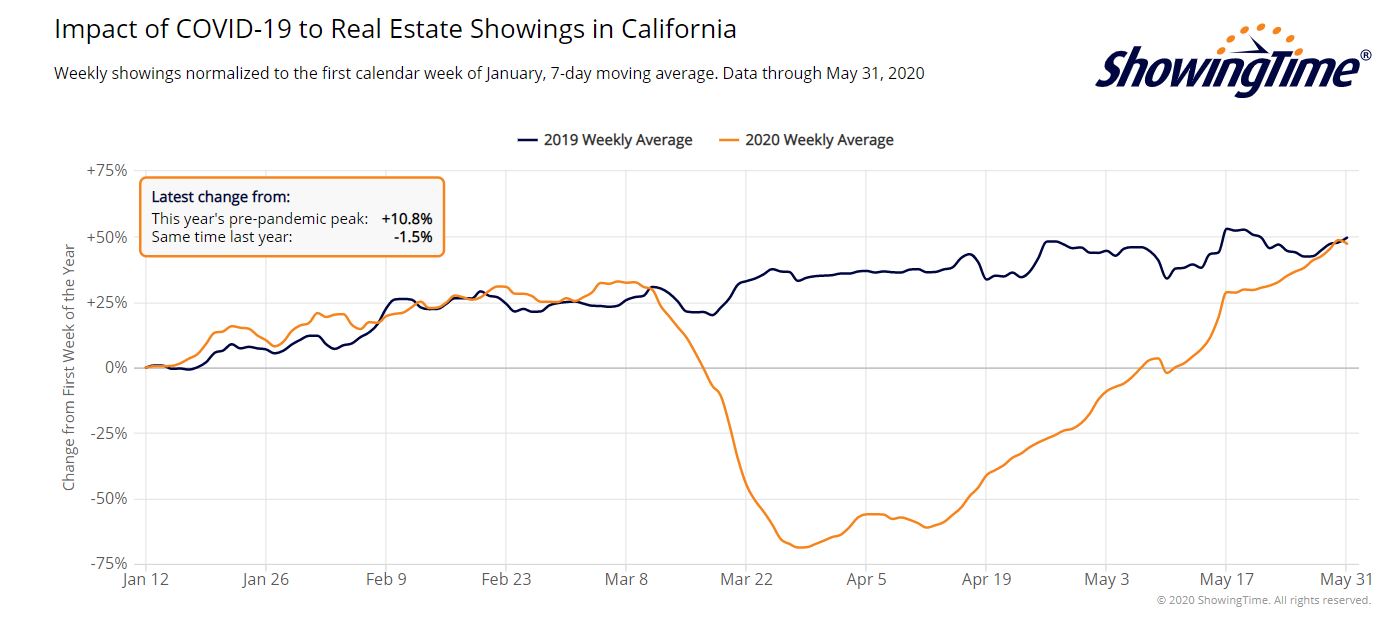

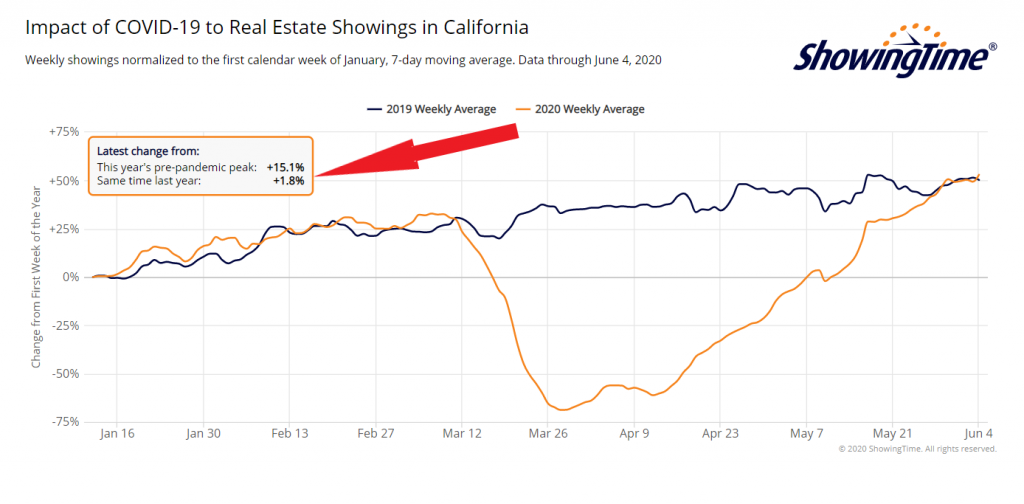

by Jim the Realtor | Jun 1, 2020 | Jim's Take on the Market, Market Buzz, Showings, Virus |

Our coronavirus showing disclosure form changes every week (sometimes multiple changes per week) and now it’s literally up to EIGHT pages long. Every buyer has to sign a new form for every house they want to see, in advance, and by electronic signatures only.

But it hasn’t slowed down showings – we are back to where we were last year!

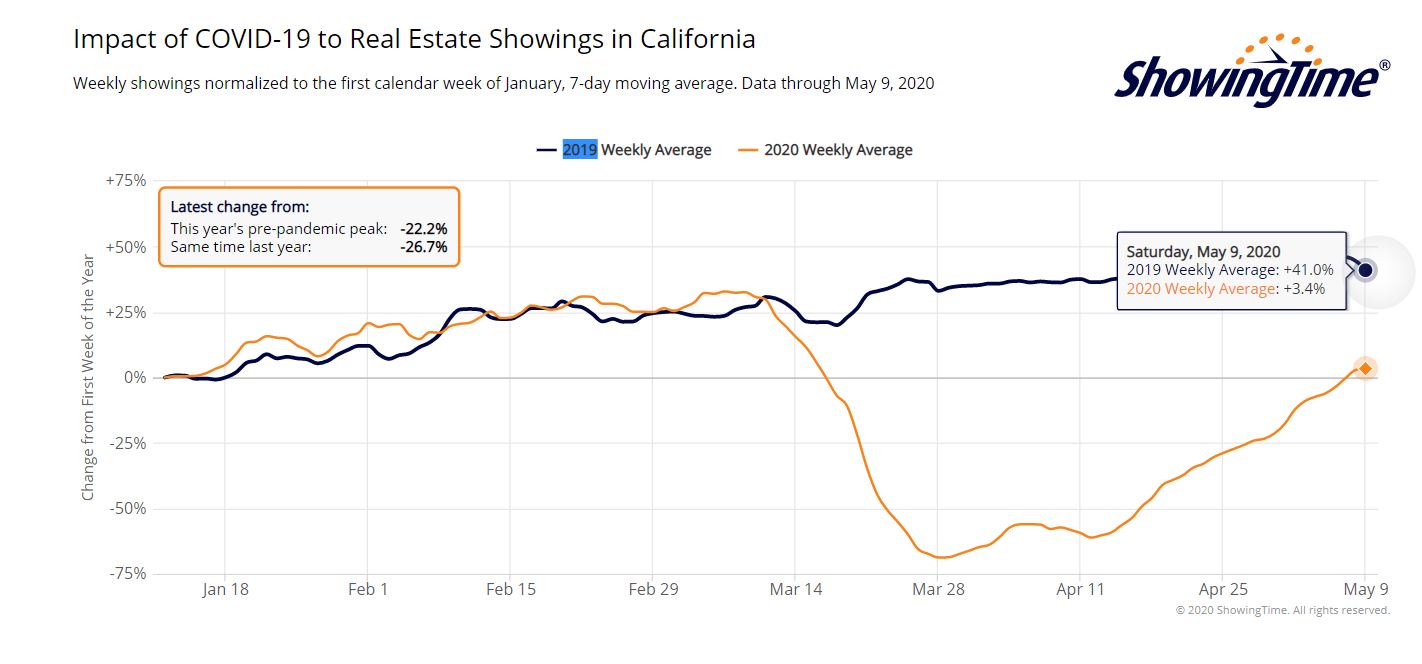

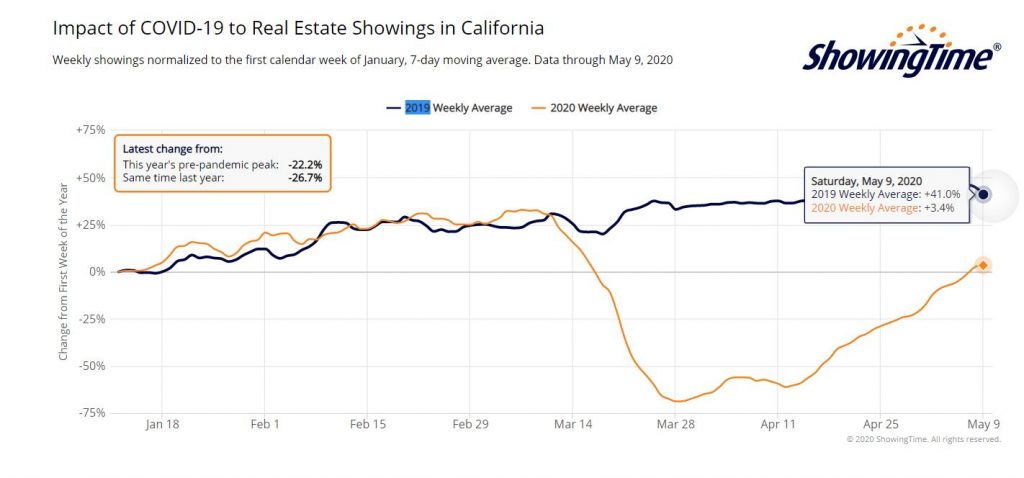

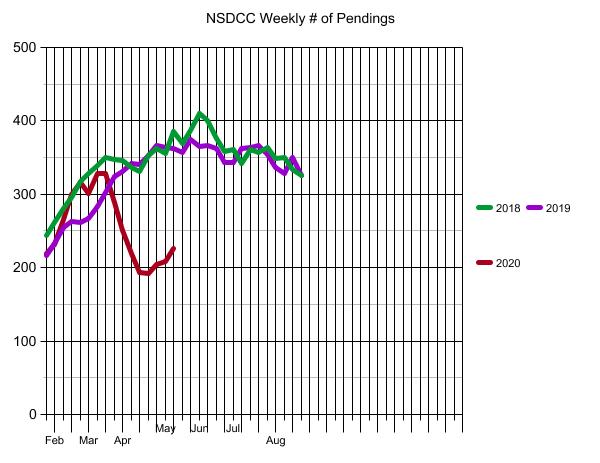

by Jim the Realtor | May 11, 2020 | Inventory, Jim's Take on the Market, Showings |

It looks like we are beyond the worst of it, and we’re on our way…..as long as rates stay in the low-3s and nothing really bad happens for the next 2-3 months.

The active and pendings counts have been rising steadily for four weeks, so we can say that the bottom was in mid-April. Here are the weekly numbers for the last two months:

Weekly NSDCC New Listings and New Pendings

| Week |

New Listings |

New Pendings |

Total Pendings |

| Mar 16 |

83 |

55 |

329 |

| Mar 23 |

59 |

31 |

289 |

| Mar 30 |

63 |

31 |

251 |

| Apr 6 |

57 |

21 |

219 |

| Apr 13 |

48 |

17 |

194 |

| Apr 20 |

63 |

29 |

192 |

| Apr 27 |

79 |

40 |

205 |

| May 4 |

86 |

40 |

208 |

| May 11 |

91 |

48 |

226 |

There is some concern in the Over-$3,000,000 category. The active inventory jumped +7% this week, and now there are 252 houses for sale, and 23 pendings. But nothing new there!

(more…)