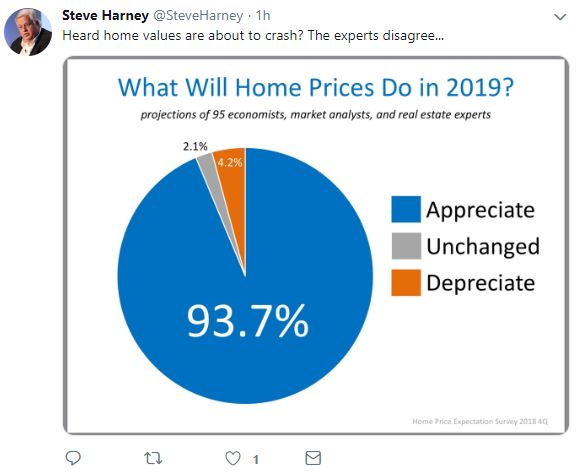

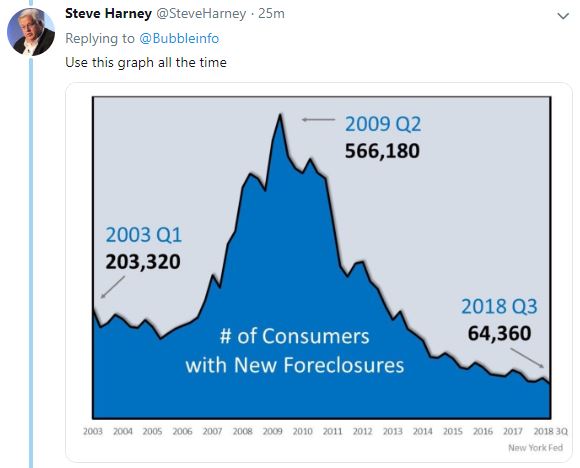

Here are graphs from one of the more bullish real estate prognosticators:

Steve is a residential real estate expert who specializes in market trends. He has been in the industry for over 25 years, first as an agent and then developing his own 500-agent real estate firm. Steve now helps producers achieve their true potential. He authors a monthly informational presentation for top professionals titled, “Keeping Current Matters” (also known as KCM), and is seen as a leading industry thought leader.

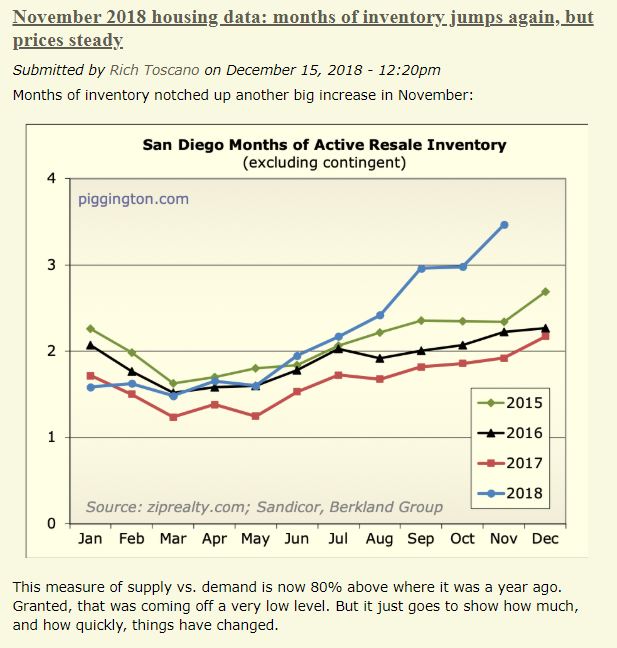

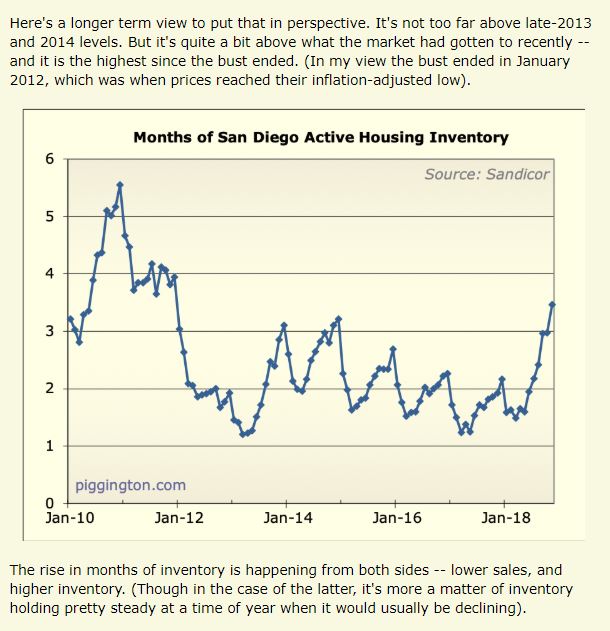

The worrisome spike last month did flatten out, but it does make you wonder if we should adjust our sights.

I agree with Rich that the months of active inventory will probably be rising from now on. But if the coastal market had 3 or 4 months of active inventory, it wouldn’t be a bad thing. Rancho Santa Fe is 7+ and doing fine.

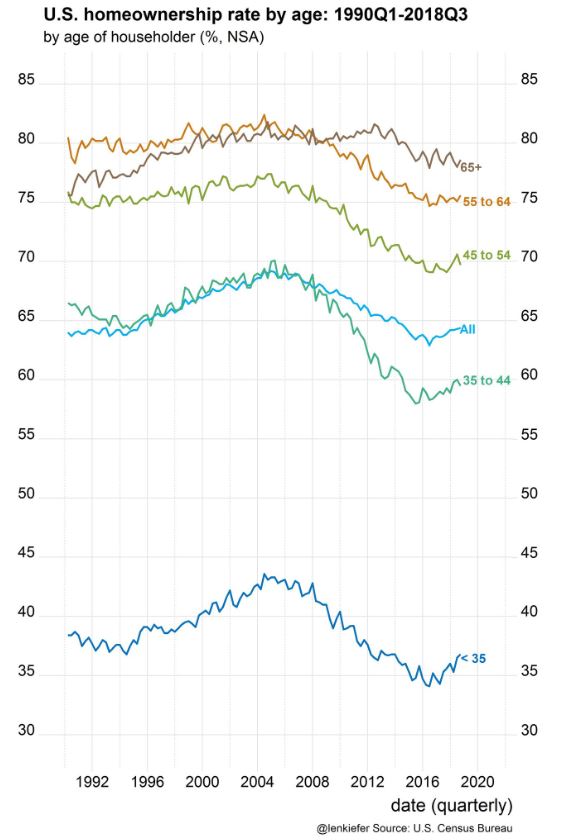

This is the Deputy Chief Economist at Freddie Mac:

It is incredible to see the trend change in every category around 2016 – as if there was a societal shift that gave permission to get back in the game.

Maybe that’s when the Bank of Mom and Dad kicked in, and their distribution of wealth made it possible to buy even though prices were soaring?

Or the resurgence from lower-end buyers enabled the move-up market?

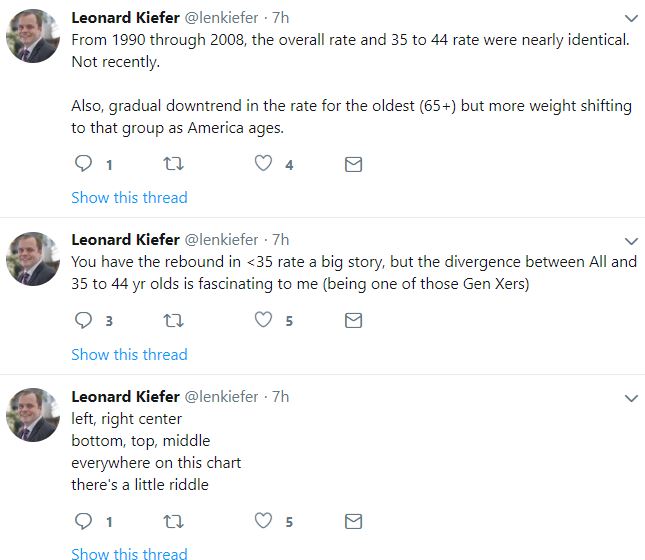

We have dispatched the lightweights around the Bay Area and have now passed those pesky VenCo guys, so only one more town in our way – Los Angeles!

We can do this! Keep being less-affordable San Diego!

The NAR didn’t list the criteria they used to create this graphic, so I’m not sure what we need to do to win, except tell your friends and family to move to Ohio or Scranton, PA?

But seriously. We’re America’s Finest City (though New York City is in the running – wow!). Shouldn’t more rich people be moving here to retire? And fewer retirees be willing to leave?

In a downturn, our housing market could survive better than other cities just because of the retiree influence.

Our favorite doomer is predicting 15% to 20% drops in pricing net year (link in twitter feed in right-hand column). Mark has been making these dire predictions for years now, and eventually he might be right.

But it would take surge in supply to start a downturn…..so all we have to do is keep an eye on inventory counts. If the number of homes increased modestly, sales should respond accordingly.

Where is the balance of too much supply? It will vary in each area, and be based mostly on price. You could have 1-2 over-priced homes not selling in one area, and look like a glut, while in other areas have 5-10 well-priced homes hit the market and all get gobbled up.

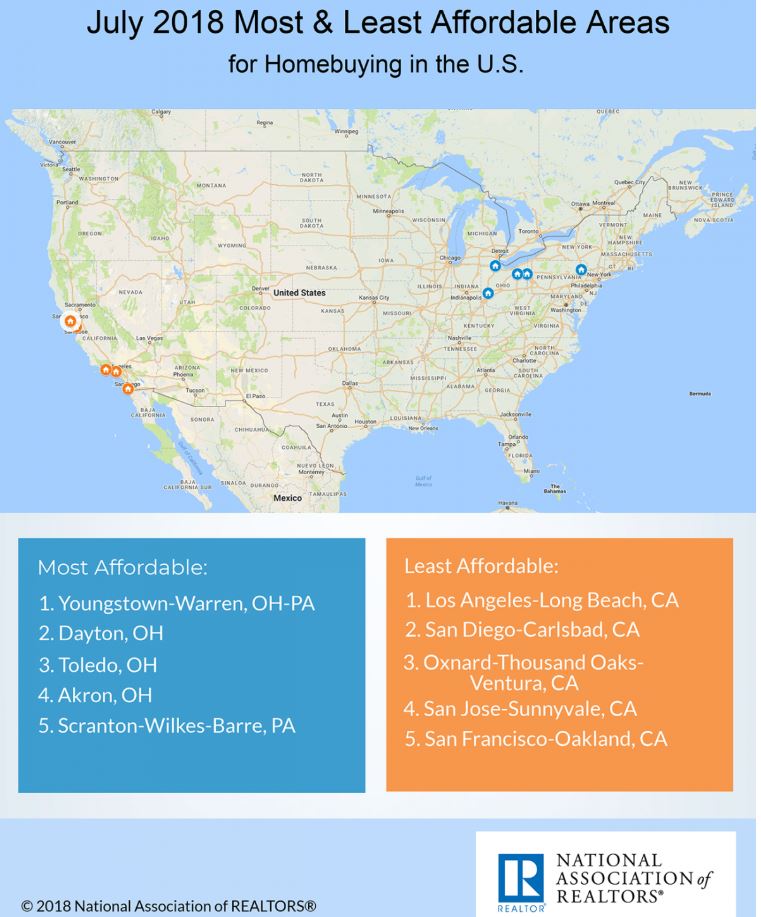

I’ll speculate that a surge of more than 20% in the inventory counts is cause for concern. How are we doing so far?

When comparing to the very consistent last few years, a 4% rise in new listings this year stood out. But compared to 2002-2011, the inventory has been remarkably predictable lately – we even had two years with identical counts:

In addition, this year’s increase could purely be due to old listings being re-freshed, an annoying trend that seems to be more popular than ever.

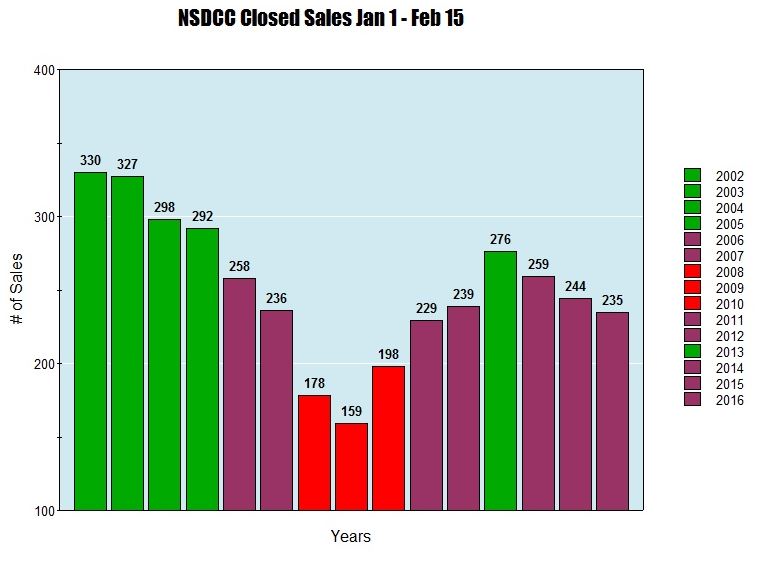

Can we learn from the sales count too?

Absolutely, and any drastic swing in the sales count is the ultimate sign of demand. We will still have late-reporters adding to this year’s count, which should easily get it above the 2015 sales:

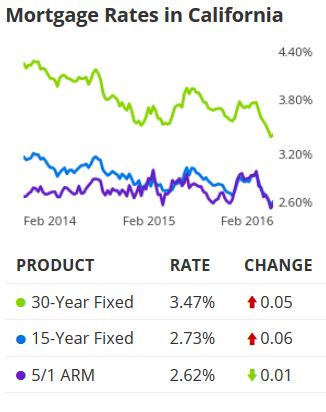

As long as rates are in the 3s, we should be fine this season!

When there are so few companies doing any exhaustive research about the market – especially at the local level – realtors will take whatever they can get and pass it along to clients. In this case, that message will be positive.

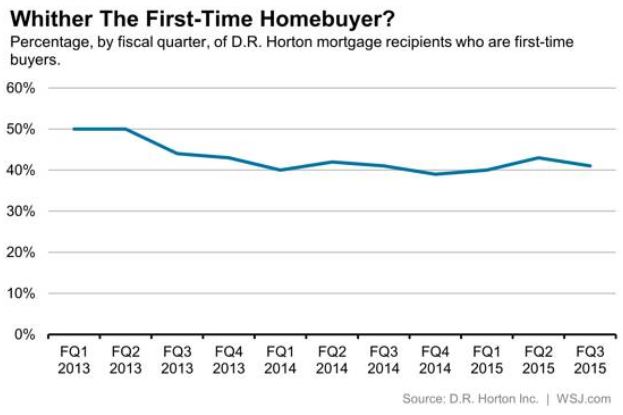

Recently we’ve wondered how many first-timers are participating, but actual data has been scant. D.R. Horton says that 41% of their buyers are first-timers, which is probably similar to the resale market and sounds fairly healthy:

Here are the current market conditions through the eyes of D.R. Horton:

It doesn’t do much good unless you’re selling, or planning to sell. Speaking of sellers, in April, there were 78% of them sold for a gain in San Diego: