Between trying to watch the Padres game on my phone and the crowds of people looking at the house yesterday, I couldn’t get any more footage than this:

After having roughly 300 people attend the two open houses, we have received 14 offers!

We have countered all of the offers because agents don’t know who will go higher – why limit the seller response to just the top 3 or 5 offers? We countered $1,150,000 to every buyer to narrow down the group of contenders willing to go to at least that amount, and then I’ll do the jimjamalama.

Stay Tuned!

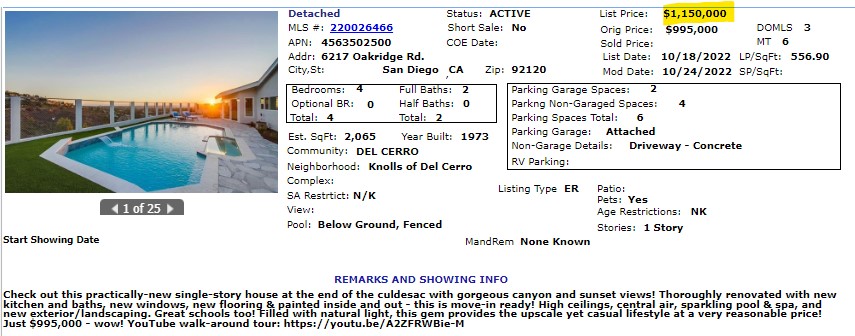

We did adjust the price upward this morning to alert the newcomers to our new starting point:

There were a few comments, mostly from neighbors, that accused me of deliberately starting with an ultra-low price to attract more people. Given the recent sales nearby, the current market conditions, and especially the active listings sitting around unsold, I thought it was an attractive price. I never fear pricing too low because I know how to handle a fair bidding process so everyone has a chance to pay top dollar.

The national bashing of the real estate market continues unabated, and I’m sure there are individual markets that are really feeling it. But real estate is local, so let’s examine the facts.

To get a sense of what has been happening since rates got into the 6s, let’s review NSDCC homes that have gone pending recently. You don’t have to know the streets or the particular homes – just scroll through the bunch and you’ll get the feeling that frenzy pricing is still lingering. Click on any for the full listing:

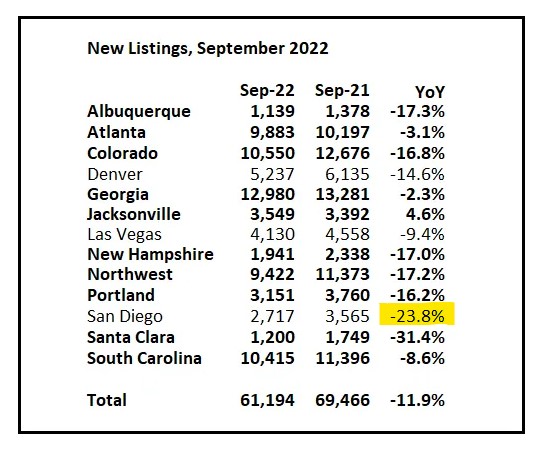

Bill has been following the inventory in different markets, and San Diego is faring much better than other areas. He is showing a 23.8% drop in new listings YoY, but last year was the record low. Look at the previous years:

September New Listings, San Diego County Detached and Attached Homes:

2005: 6,325

2006: 5,735

2007: 5,448

2008: 5,101

2009: 4,328

2010: 4,696

2011: 4,013

2012: 3,578

2013: 4,265

2014: 4,367

2015: 4,185

2016: 4,267

2017: 3,953

2018: 4,506

2019: 3,959

2020: 4,389

2021: 3,570

2022: 2,853

Everyone talks about the demand-side, but our market is being impacted by the lack of supply too.

Could there be demand that isn’t being satisfied because there aren’t more quality homes for sale listed by good agents at attractive prices?

I had 100+ people come to open house this weekend, and there were legitimate buyers in the group.

I wanted to show a house this weekend, and the showing instructions said to text the listing agent. I started via text on Wednesday, but literally never got a response, so I didn’t show it. The listing is still active today.

Higher rates haven’t changed the frustration of finding the right house, at the right price.

The inventory is probably going to dry up further and more sellers get convinced that now isn’t a good time to sell. With a tight selection of quality homes for sale, those who are willing to sell now aren’t going to be deterred from trying peak pricing, or close.

Example: My $1,800,000 listing in Aviara? This just popped up around the corner, priced at $2,295,000:

Those folks might sell, and they might not, but they should help me with mine! My point is that we are not seeing an increasing flow of new listings being priced lower and lower in an attempt to get out now. It’s actually quite the opposite.

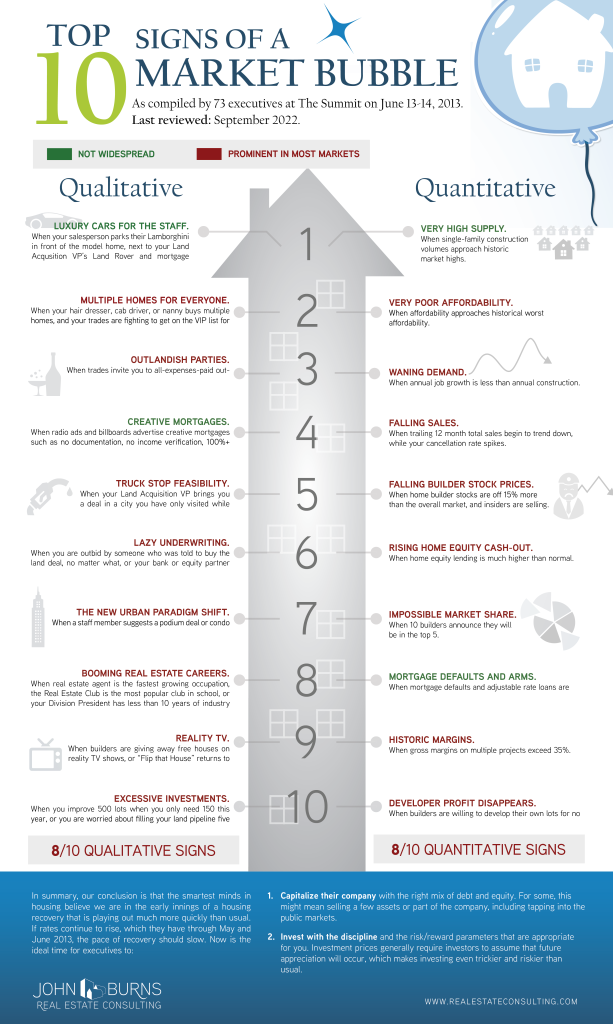

In 2013, fresh off the biggest housing downturn in their lifetimes, 73 housing industry executives compiled the Top 10 Signs of a Housing Market Bubble at our Summit Conference in Laguna Beach, CA. Assessing the criteria that we set almost a decade ago (10 quantitative and 10 qualitative), we have found that 16 of the 20 housing bubble signs are now flashing red.

In last month’s client-exclusive housing outlook webinar, we called out some signs we are seeing:

There will always be an occasional low sale here and there.

What would cause home prices to really slide?

There would need to be a series of low sales in the same area to create downward momentum. The next seller would have to be convinced that lower prices are a fact, and without an obvious trend, they will be reluctant to believe it.

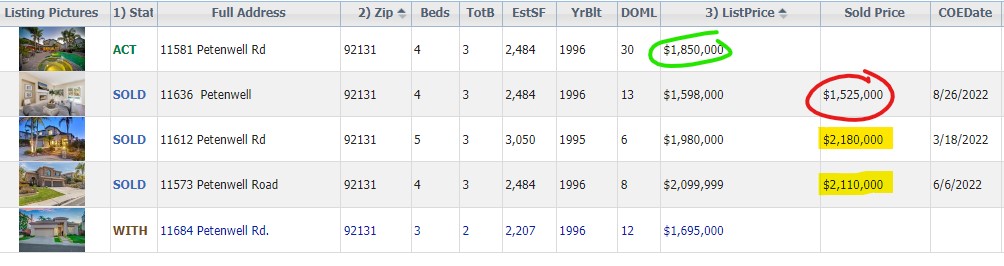

Here’s an example. Even though this lowball listing (in red) undermined the two comps over $2 million, the next seller wasn’t convinced, and they listed their home for $1,975,000. They have lowered it since, but you can bet they are digging in now – and the market is in their hands:

If they hold out and get close to their price, then the lowball sale will be dismissed as one-off, and other sellers in the future will ignore it….and hope the buyers do too.

These are the standoffs happening everywhere now. ALL sellers have plenty of equity and could go down in price if they really wanted – or needed – to make the sale.

But will they?

Generally speaking, the agents might go along for 30 days or so, but they aren’t used to sitting on unsold listings for months. They are going to nudge the sellers to lower their price, but those drops need to be in 5% increments to cause a meaningful reaction from the buyers.

Will some sellers surrender? Yes, but only when confronted with a lower offer. Currently we are in the Buyer-Vacation stage where few are in the game and making offers, and without solid proof, the sellers are more likely to wait, than dump.

The 2023 Selling Season will be the most anticipated market in the history of the world!

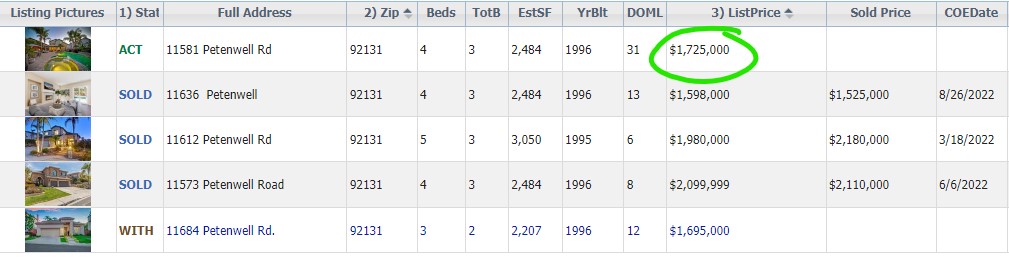

New update – another price reduction. Buyers are on vacation now, we’ll see about 2023:

Dr. Doom said in his podcast here that the California markets have had the most significant price declines, and the Bay Area, LA, and San Diego have ‘gotten creamed’.

He didn’t provide any data to back it up, so let’s look at what we have from the MLS which includes September data so we’re including the most relevant information.

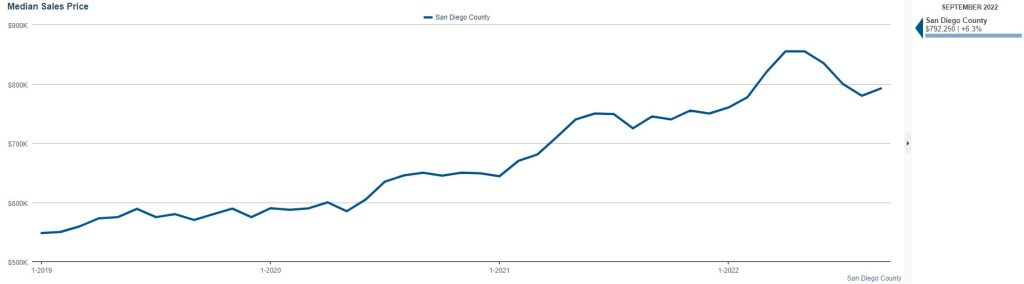

San Diego County, All Property Types:

The San Diego County median sales price was $855,000 in June and July, and last month it was $792,500 – which was a 7% decline from the peak this summer. It was also 2% higher than in August. Is that creamed?

We’re coming off the greatest real estate frenzy of all-time, and now the Fed has caused mortgage rates to double in less than six months. All considered, I think we’re doing great, and better than expected.

These guys who just fling it around on their national platforms are doing undue harm to our market. Don’t listen to them until they get out of their mom’s basement and actually investigate what’s really happening!

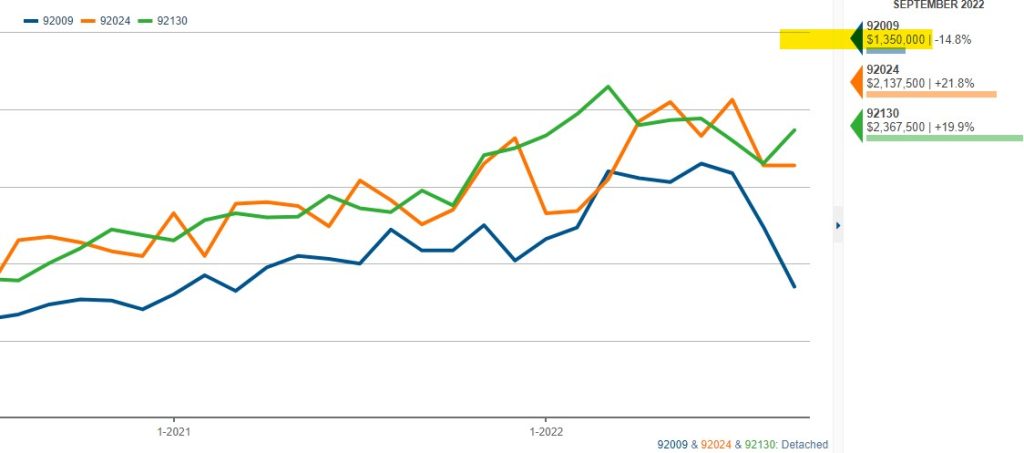

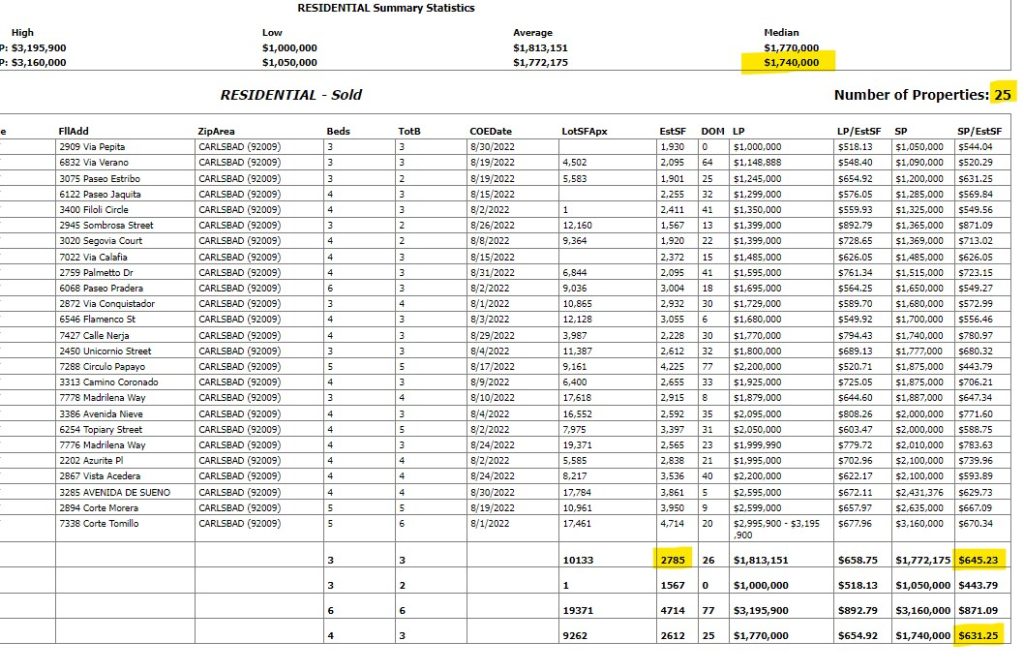

Last month, the 92009 median sales price declined 14.8% YoY, and was -22% MONTH-OVER-MONTH.

Keyboard warriors everywhere will be jumping all over news like this.

What really happened?

The facts:

Last month, there were 52% fewer sales than in September, 2021.

The homes that sold last month were 13% smaller than in August.

The average and median $$-per-sf were higher month-over-month.

There were only 23 sales last month. Fewer sales means more volatility in the data, and the numbers will be bouncing all over the place. The average SP:LP was 97%, so nobody was giving it away, and when you look at sales like the last one on the list on Corte Luisa, know that it was an agent selling his own house for a $980,000 profit above what he paid in 2020.

You have to look deeper into the data to get the full picture of what’s really happening!

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

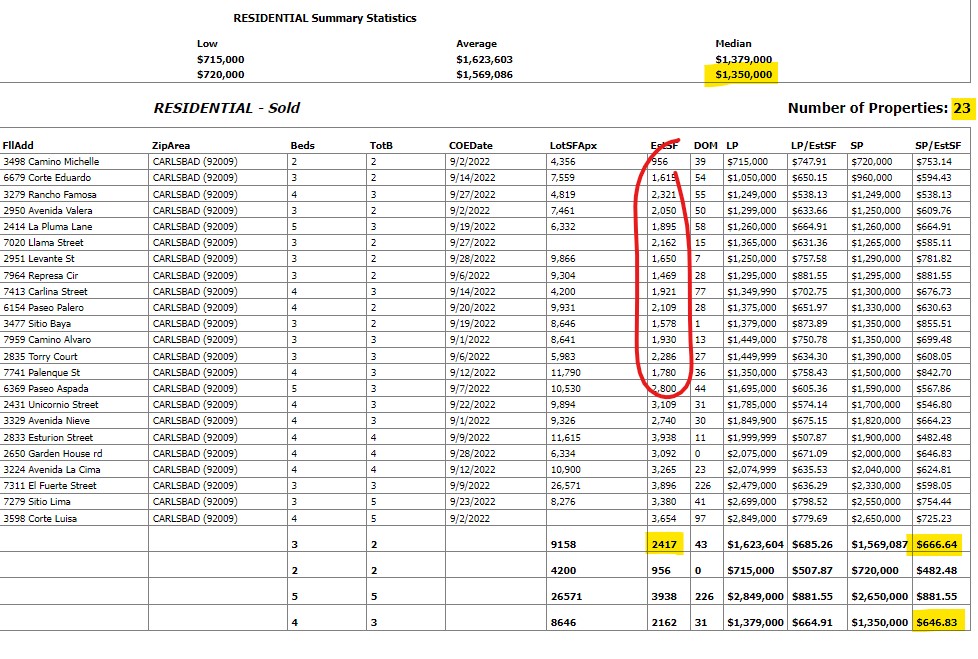

Here are the August and September stats:

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

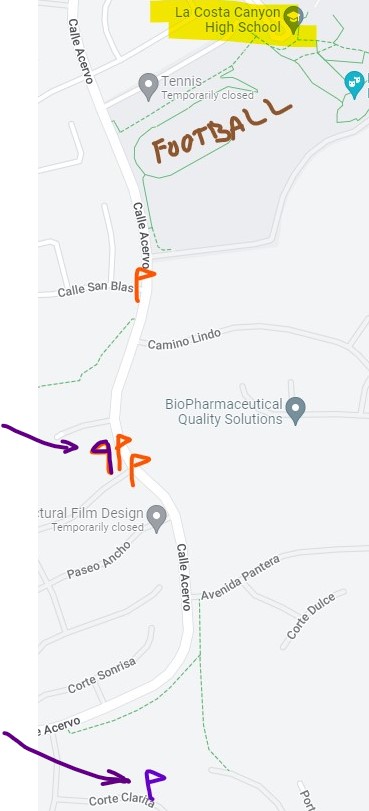

Let’s revisit a previous blog post for an update, and more detail.

I featured a group of listings near La Costa Canyon HS a couple of weeks ago. The day the blog post ran, the most-expensive listing was pending, but it fell out of escrow that day. It’s back in escrow this week, and judging by how the listing agent ran my rather-sizable nose in it, they must have gotten pretty close to their list price. Tracey sold hers too, and together the two highest-priced listings are the ones that are pending, which demonstrate that buyers want quality and are willing to pay for it.

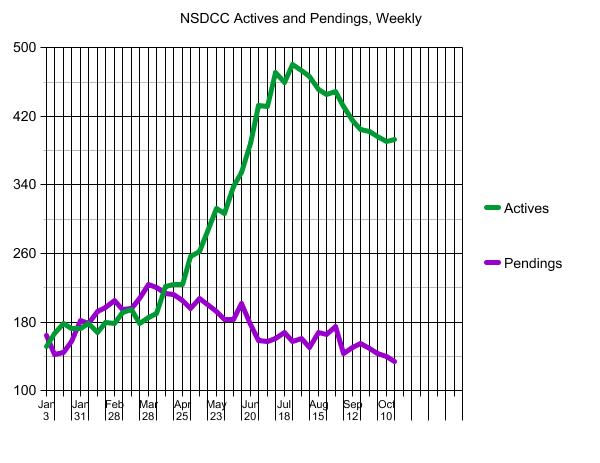

Pendings = purple:

Realtors who have no game will be reading juicy headlines on social media and be telling their sellers to dump on price, rather than dig for the truth and get to work.

GET GOOD HELP!

And just wait until I tell you the story about this one!

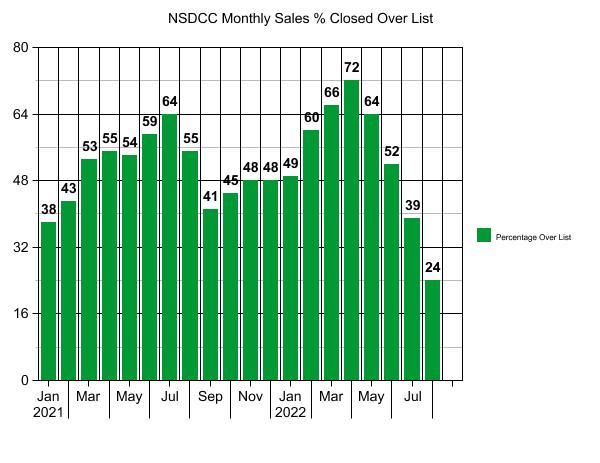

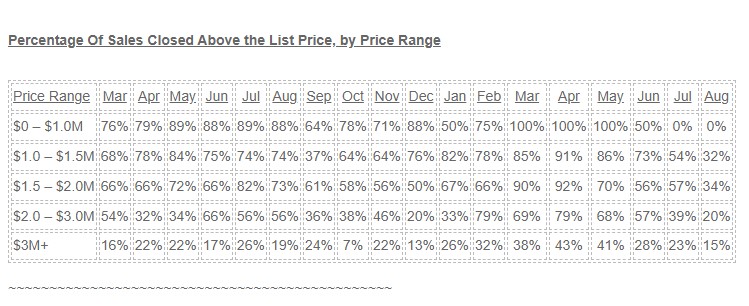

The over-bidding is winding down to more manageable levels as just 24% of August buyers were willing to pay over the list price. As usual, the $1,000,000 to $2,000,000 range was the most active, where inventory is low and the number of quality homes for sale even lower:

The number of sales in August were higher than they were in July, but still well under recent history:

NSDCC August Sales

2018: 275

2019: 263

2020: 351

2021: 268

2020: 161

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

NSDCC Average and Median Prices by Month

Month

# of Sales

Avg. LP

Avg. SP

Median LP

Median SP

Feb

224

$2,298,797

$2,257,334

$1,719,500

$1,758,000

March

252

$2,295,629

$2,260,524

$1,800,000

$1,825,000

April

357

$2,396,667

$2,403,962

$1,799,900

$1,828,000

May

300

$2,596,992

$2,581,715

$1,900,000

$1,994,500

June

348

$2,509,175

$2,537,953

$1,900,000

$1,967,500

July

311

$2,421,326

$2,442,738

$1,795,000

$1,855,000

Aug

268

$2,415,075

$2,438,934

$1,897,000

$1,950,000

Sept

278

$2,479,440

$2,445,817

$1,899,000

$1,987,500

Oct

248

$2,754,470

$2,705,071

$1,899,000

$1,899,500

Nov

199

$2,713,693

$2,707,359

$1,999,000

$2,100,000

Dec

189

$2,686,126

$2,664,391

$1,985,000

$2,157,500

Jan

140

$2,828,988

$2,855,213

$2,234,944

$2,240,000

Feb

158

$3,063,331

$3,108,907

$2,149,500

$2,386,500

Mar

207

$3,247,251

$3,337,348

$2,400,000

$2,625,000

Apr

227

$3,190,161

$3,251,604

$2,350,000

$2,550,000

May

214

$2,941,080

$3,030,794

$2,350,000

$2,480,000

Jun

188

$2,871,956

$2,881,314

$2,297,500

$2,350,000

Jul

152

$2,892,729

$2,833,588

$2,272,000

$2,280,000

Aug

161

$2,953,967

$2,849,332

$2,200,000

$2,150,000

This is much more normal – the average and median sales prices are under their list prices!