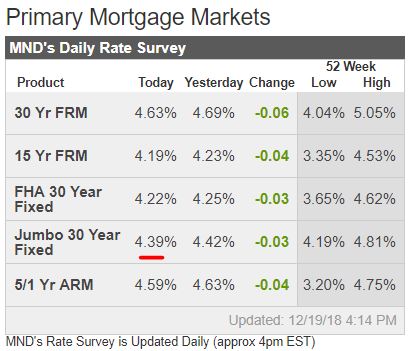

As with the other recent Fed hikes, mortgage rates actually dropped today on the news, and MND’s regular voice thinks it could keep going:

Today’s Fed Statement and forward guidance meshed with investors’ expectations, helping bonds maintain their recent gains. Treasury yields breached resistance, dropping to 2.78% and MBS improved slightly. While the trend to lower rates isn’t etched in stone, we do appear to be headed that way. I’ll lock applications closing within 15 days, and risk averse clients closing within 30. Looks like Christmas is coming a little early for borrowers and lenders! – Ted Rood, Senior Originator

We’ll hear how rates are historically low and two more rate hikes are coming in 2019 so hurry up and buy now, but it sounds like sales talk to those who were already going to wait-and-see anyway.

Jumbo mortgage rates around 4.25% might get them back in the game!

We can get a feel for how much the market is struggling based on the types of financing that are needed to keep homes selling.

When it’s hot, all we need is a 30-year fixed-rate mortgage.

What loan programs are available today?

Everything except a neg-am, and only because they were outlawed!

A lender solicited my business yesterday, so I asked him to send me a list of what he can do – decide for yourself, but it appears we are searching under every rock for potential buyers now:

Hi Jim,

Thanks for taking my call. I’m looking forward to helping you close more deals!

Asset depletion – We have the most aggressive program in the business. For every $1MM in assets, we give $16,666/month in income. Other banks are half to a third of that amount.

Foreign National Programs – no US Credit, no US Tax Returns, as little as 30% down, rates in low 5% range

Just closed $1.5MM purchase in Carmel Valley with a client from Myanmar – easiest foreign national loan in the market

Bridge loans (not hard money) –

No need to be contingent upon sale. Use equity in current properties to buy without selling first

Doesn’t need to be primary residence – can be second homes and investment properties too / great tool to get your investors to buy more property

Just closed the largest one in San Diego for $6.5MM with NO MONEY DOWN

Bank statement loans that actually work – we only look at the deposits (call all the people you know who are self-employed and writing everything off… now they can buy a house)

I am in contract now with a client for $1.6MM and she had a pre-foreclosure less than 2 year ago with just 15% down.

As little as 10% down

I have a lot more loan programs to save your deals or help you get new ones into contract that need more creative financing.

First, the WSJ posted an editorial on Sunday – a snippet:

If you think your job is tough, consider Federal Reserve Chairman Jerome Powell. He’s signaled for months that the Fed will raise interest rates again this week, but economic and financial signals suggest he should pause. Meanwhile, Donald J. Trump is beating him up almost daily not to raise rates.

What to do? The right answer is to ignore the politics, inside and outside the Fed, and follow the signals that suggest a prudent pause in raising rates at this week’s Open Market Committee (FOMC) meeting. Get the monetary policy that best serves the economy, and the politics will work itself out. Get the policy wrong, and Mr. Trump will be the least of Mr. Powell’s political worries.

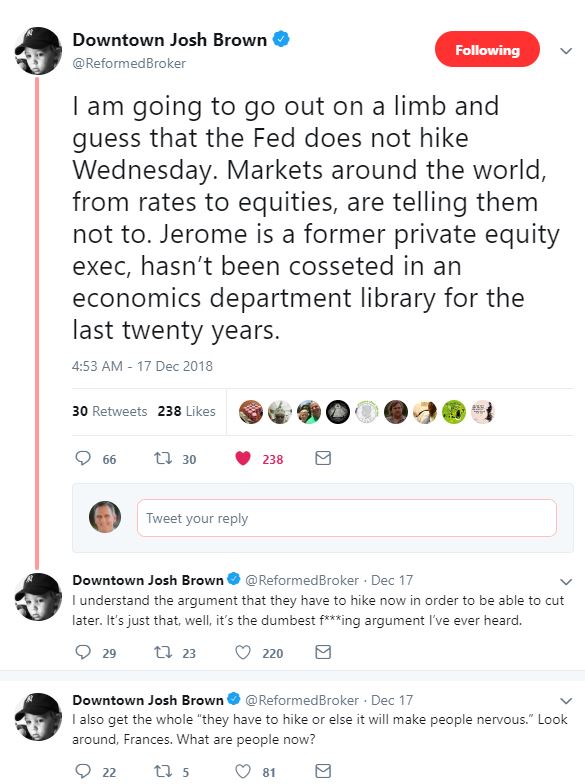

Josh agreed in his tweet above, and it looked like we had a shot!

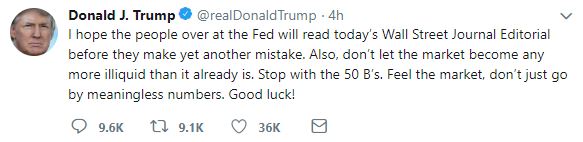

Trump could have just let it go…..but noooo, he had to tweet one more time:

In case the Fed is looking around for evidence, consider our recent home sales:

End-of-Year Detached-Home Sales and Pricing

Category

2017

2018

% change

NSDCC # of Sales, 10/1 – 12/15

600

537

-11%

NSDCC Median SP, 10/1 – 12/15

$1,200,000

$1,350,000

+13%

SD County # of Sales, 10/1 – 12/15

4,637

3,886

-16%

SD County Median SP, 10/1 – 12/15

$615,000

$640,000

+4%

The Fed is going to be tempted to make their rate decision based on politics, and show Trump who the boss is. Median pricing is like politics – it makes you want to make decisions based on less-relevant data.

Keep your eyes on sales – they are the precursor of what’s ahead.

Even if the Fed skips this rate hike, we are still going to see sales plummet next year. They could help make it a softer plummet though!

Home buyers and sellers might be concerned enough about the results of the Mueller report that it could impact their decision-making about real estate – as if they need one more reason to wait-and-see!

They expect that Mueller report to be filed within the first six months of 2019, but is could be a bit redundant as players are already being indicted and convicted of crimes.

I think we can count on this:

It would take two-thirds of the Senate to confirm an impeachment, so it’s unlikely Trump will be removed from office.

He ain’t going to quit.

No matter how bad the actual facts could be, will the hysteria be any worse than it is today? Trump will declare it all a which hunt, and he might incite some vigorous protests by his followers. The mainstream media will have a field day too.

But aren’t we numb to this already?

I think so, and while there will undoubtedly be some eye-popping events immediately after the report’s release, we’ll get back to business before too long. For some, it might be a relief that sets them free to buy and sell, and for others it could make them want to hunker down even more!

The OJ trial last for 8+ months, and that’s about as long as our society could stay distracted. You could also say that with the onslaught of multi-media we have today – which is far more intense and scattered than it was in 1995 – we won’t stay focused on any one thing for very long.

We had a good year for real estate locally during the OJ trial in 1995 – there wasn’t much, if any, impact. The real estate market had just hit bottom, and began what was a 12-year run!

My biggest real estate concerns for 2019:

Mortgage rates

Do we have enough ready, willing, and able buyers?

The biggest impact on the early-2019 market could be the Chargers getting into the Super Bowl! The Patriots look vulnerable, and the Bolts’ victory on Thursday had to demoralize the Chiefs:

If the Chargers win the Super Bowl, everyone will be happy about real estate!

We have about the same number of NSDCC houses for sale as usual this time of year, and the list-pricing appears to have plateaued too:

NSDCC Active Listings, 3rd Reading in December

Year

# of Active Listings

4Q Median List Price

2014

878

$1,199,000

2015

821

$1,348,500

2016

798

$1,377,500

2017

641

$1,549,900

2018

818

$1,550,000

The Fed meeting will be the biggest news of the week – if mortgage rates would improve between now and mid-January, we could see an active start of the year. If not, then the wait-and-see mode will be irresistible for buyers.

As blogger-in-chief here, I’ll stay on the lookout for the positive housing news – because you won’t have any trouble finding the alternative, like this guy who has been calling for home prices to drop 10% to 30% for several years now:

Here’s a Bloomberg essay that draws some comparisons to the 1994 market, which is another time we had a spike in mortgage rates. We had neg-am and no-doc mortgages then, and were coming off a multi-year downdraft of housing prices due to the S&L crisis, but if mortgage rates are the big decider, then it’s a fairly good comparison – note the 20% drop in new-home sales:

Housing market softness in the back half of 2018 has investors and the public wondering how bad things might get. It’s understandable that people would be worried, considering that the last housing downturn led to the worst economic crisis since the Great Depression.

But housing market fundamentals in this cycle are nowhere near as risky as they were in the mid-2000s. Real-time data on mortgage applications suggest a milder path. Coincidentally, it looks a lot like 1994.

Compass realtors and staff volunteered today to help with the 36th Annual Holiday Baskets put on by the Community Resource Center of Encinitas. It is a fantastic event where families below the poverty line receive food, clothes, presents, and bikes:

Earlier this week the grays were on their way out, but it may take a while. Can you believe that 34% are removing the bathtub? From Houzz:

Anticipating Aging Needs: The majority of baby boomers (ages 55 or older) are addressing current or future needs of aging household members during master bathroom renovations (56%). One-third of boomers are addressing current aging needs (35%), while nearly a quarter are planning ahead for future needs (21%).

Curbless Enthusiasm: Nearly half of boomers change the bathroom layout and one-third remove the bathtub (47% and 34%, respectively). Other upgrades include installing accessibility features such as seats, low curbs, grab bars and nonslip floors in upgraded showers and bathtubs.

The Suite Life: Homeowners are focusing on the master suite as a whole, with nearly half of master bathroom projects accompanied by master bedroom renovations (46%). Master bathrooms command the second-highest median spend ($7,000) in home remodels, behind kitchens ($11,000), while master bedroom spend rivals that of living rooms ($2,000 versus $3,000, respectively).

Premium Features Galore: A surprising one in 10 master bathrooms is the same size or larger than the master bedroom (11%). Beyond size, premium features in master bathrooms are on the rise, with dual showers, one-piece toilets, vessel sinks and built-in vanities showing significant increases in demand in the last three years.

Bathed in Gray: Gray palettes continue to lead in walls and flooring and are increasingly popular in cabinets. Newcomer styles continue to overtake contemporary style, with farmhouse more than doubling in popularity, from 3% in 2016 to 7% in 2018. Matte nickel and polished chrome are the most common metal finishes.