The area’s history is punctuated by such major back-to-back storms, but many residents say they are becoming more frequent and severe, and scientists agree.

“More people die here than anywhere else from floods,” said Sam Brody, a Texas A&M University at Galveston researcher who specializes in natural hazards mitigation. “More property per capita is lost here. And the problem’s getting worse.”

Why? Scientists, other experts and federal officials say Houston’s explosive growth is largely to blame.

As millions have flocked to the metropolitan area in recent decades, local officials have largely snubbed stricter building regulations, allowing developers to pave over crucial acres of prairie land that once absorbed huge amounts of rainwater. That has led to an excess of floodwater during storms that chokes the city’s vast bayou network, drainage systems and two huge federally owned reservoirs, endangering many nearby homes.

The region was once home to acres of prairie grass whose roots extended far underground, with a capacity to absorb water for days on end or even permanently. Most of that land has now been paved over. The Katy Prairie northwest of Houston was once about 600,000 acres of flood-absorbing land; recent development has reduced it to a quarter of that capacity, according to estimates from the Katy Prairie Conservancy, an advocacy group.

That means the rain is now falling on what are called impervious or impermeable surfaces, like concrete, preventing the ground underneath from absorbing it. So the rainfall becomes “runoff,” traveling to wherever is easiest for it to flow. The water might flow to a nearby stream, but on its way the water could flood homes, cars and businesses, or the stream might be overwhelmed by that water, causing more flooding nearby.

As she was getting on in years and her resources dwindled, Virginia Rayford took out a special kind of mortgage in 2008 that she hoped would help her stay in her three-bedroom Washington rowhouse for the rest of her life.

Rayford, 92, took advantage of a federally insured loan called a reverse mortgage that allows cash-strapped seniors to borrow against the equity in their houses that has built up over decades.

But the risks of the financial arrangement are stark — and today the frail widow finds herself facing foreclosure.

Under the terms of the loan, Rayford can defer paying back her mortgage debt that totals about $416,000 until she dies, sells or moves out. She is, however, responsible for keeping up with other charges — namely, the taxes and insurance on the property.

The loan servicer, Nationstar Mortgage, says Rayford owes $6,004 in unpaid taxes and insurance. If she cannot come up with it, she stands to lose her home in Washington’s Petworth neighborhood.

“I’ve cried a million nights wondering about where I am going to be,’’ Rayford said.

I appreciate our clients who are willing to go on camera to express their thoughts about their experience – thank you Eddie89!

A key point for buyers in a bidding war is to know when to increase your bid, and by how much. I help you determine which houses are worthy of a higher bid – and most aren’t, so you will lose a few!

In what has to be one of the most bizarre developments in real estate this year, the ivory-tower folks at the Fed, of all people, dreamed up a creative new loan that would not require a down payment. Then they used the dreaded COFI term from neg-am mortgage days! No word on when these might be available, if ever:

Abstract: The 30-year fixed-rate fully amortizing mortgage (or “traditional fixed-rate mortgage”) was a substantial innovation when first developed during the Great Depression. However, it has three major flaws. First, because homeowner equity accumulates slowly during the first decade, homeowners are essentially renting their homes from lenders. With so little equity accumulation, many lenders require large down payments. Second, in each monthly mortgage payment, homeowners substantially compensate capital markets investors for the ability to prepay. The homeowner might have better uses for this money. Third, refinancing mortgages is often very costly.

We propose a new fixed-rate mortgage, called the Fixed-Payment-COFI mortgage (or “Fixed-COFI mortgage”), that resolves these three flaws.

This mortgage has fixed monthly payments equal to payments for traditional fixed-rate mortgages and no down payment. Also, unlike traditional fixed-rate mortgages, Fixed-COFI mortgages do not bundle mortgage financing with compensation paid to capital markets investors for bearing prepayment risks; instead, this money is directed toward purchasing the home. The Fixed-COFI mortgage exploits the often-present prepayment-risk wedge between the fixed-rate mortgage rate and the estimated cost of funds index (COFI) mortgage rate.

Committing to a savings program based on the difference between fixed-rate mortgage payments and payments based on COFI plus a margin, the homeowner uses this wedge to accumulate home equity quickly. In addition, the Fixed-COFI mortgage is a highly profitable asset for many mortgage lenders. Fixed-COFI mortgages may help some renters gain access to homeownership. These renters may be, for example, paying rents as high as comparable mortgage payments in high-cost metropolitan areas but do not have enough savings for a down payment. The Fixed-COFI mortgage may help such renters, among others, purchase homes.

Keywords: COFI, Cost of funds, Financial institutions, Fixed-rate mortgage, Homeownership, Interest rates, Mortgages and credit

JtR: This sounds like the reverse of a neg-am mortgage, or a positive-amortizing loan where borrowers have a fixed payment as a ceiling, and then when rates float down, the difference is applied to the principal. But how much potential is there for your rate to drop when we’re at all-time lows? Maybe they are preparing a loan option for the day that rates rise substantially?

The impact of losing the mortgage-interest deduction has been blown out of proportion by NAR lobbyists. Let’s tinker with it now when rates are low and see if lower taxes could spur additional demand.

There may be rumblings about lowering the cap on mortgage interest rate deductions, but it would have a “rather small effect” on the housing market, Nobel Prize-winning economist Robert Shiller told CNBC on Wednesday.

The popular deduction is “limited to a small percent of taxpayers. It’s just not that big an effect compared to the big things,” the Yale economics professor said in an interview with “Power Lunch.”

“What’s really driving the real estate market is our sense of where we’re going and the uncertainty at the time with the new administration in Washington and all this talk.”

For example, things like the deadly white supremacist rally in Charlottesville, Virginia, slows down people’s willingness to make a big financial transaction, noted Shiller, who co-founded the Case-Shiller index.

The mortgage interest deduction enables homeowners to deduct the interest paid on their home loans from their income taxes. It is currently capped at loans up to $1 million for married couples filing jointly. The cap is $500,000 for those filing separately.

Industry sources have told CNBC that reducing the deduction is on the negotiating table as Republicans work to hammer out a tax reform package.

However, most homeowners don’t claim the deduction and instead use the standard deduction, Shiller said. Therefore, he believes lowering the cap would have more of a psychological effect on home prices than a calculated one.

“This is part of American culture. It goes back to the American dream,” he said. “It stands for something. It stands for ‘the government is behind the homeowner.’ It’s a political thing.”

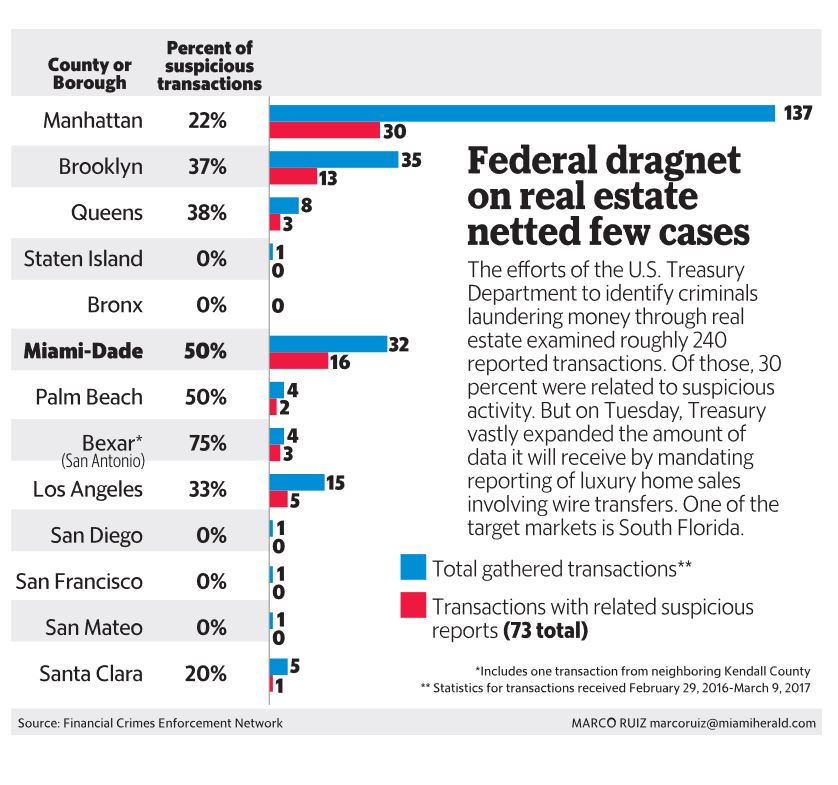

In San Diego, this applies to cash sales over $2,000,000 to LLCs.

Wake up and smell the dirty money.

That’s the message federal regulators are sending to the real estate industry in Miami and other high-priced housing markets.

On Tuesday, the U.S. Treasury Department announced it would extend and expand a temporary initiative designed to uncover criminals laundering money through real estate. The decree targets secretive shell companies — corporations that don’t have to reveal their true owners — buying luxury homes. The feds have already renewed the rules twice since announcing them in January 2016.

But this time, there’s a big difference — and it’s putting Miami’s struggling condo market under even more scrutiny.

The rules, previously so limited in scope that they applied only to a few hundred deals, will now cover every big-ticket cash transaction by shell companies in seven major markets. They are the South Florida counties of Miami-Dade, Broward and Palm Beach; all five boroughs of New York City; San Antonio, Texas; Honolulu (included in the order for the first time); and Los Angeles, San Diego and San Francisco.

“This is going to gather much more information,” said Andrew Ittleman, a South Florida attorney who specializes in anti-money-laundering laws.

Critics dismissed Treasury’s original anti-money laundering rules — first deployed in Miami-Dade and Manhattan last year — as so narrow that they were practically toothless.

That’s because only less common methods of cash payments such as money orders, personal checks and hard currency had to be reported.

But the latest order includes wire transfers, which are electronic exchanges of money between banks. In most home sales that don’t involve bank loans, money is sent from buyers to sellers through wire transfers. Regulators were missing out on a huge swath of transactions.

“It exempted most people from disclosure,” said Alan Lips, a partner at Miami accounting firm Gerson Preston. “In today’s world, people wire money.”