Hat tip to Richard for sending in this article about California workers encouraging their employer to leave the state in order to achieve the American dream – affordable home ownership:

Sure, the low taxes, relaxed regulatory environment and Central Time Zone are nice. But none of those factors tops the list of reasons Toyota decided to plant its North American headquarters in Plano, bringing in more than 3,000 jobs, mostly from California.

The main driver of Toyota’s move from Torrance, California, was housing costs, according to Albert Niemi Jr., dean of the Cox School of Business at Southern Methodist University, who has inside knowledge about the move. Niemi shared the anecdote at an SMU Cox Economic Outlook Panel on Friday morning.

“It wasn’t so much that we don’t tax income,” he said. “It was really about affordable housing. That’s what started the conversation. They had focus groups with their employees. Their people said, ‘We’re willing to move. We just want to live the American Dream.’”

Toyota did the math and found that housing costs in Los Angeles County, where Torrance is located, are three times per square foot the cost of a house in Dallas-Fort Worth.

“They’re paying the same salary,” Niemi said. “So in real terms, they’re going to triple the affordability of housing they can buy if they move to Texas.”

The Redfin Estimate has the lowest published error rate of any valuation estimate in the U.S., with only a 1.96 percent median error rate for homes that are for sale, and 6.25 percent for off-market homes. This means that when a home that is currently on the market sells, the Redfin Estimate will be within 1.96 percent of the sales price half of the time. For off-market homes, the Redfin Estimate will be within 6.25 percent of the eventual sales price half the time. The Redfin Estimate is more accurate for homes that are for sale because there is more data available about those homes.

As a real estate brokerage, Redfin has 100% complete, direct access to Multiple Listing Services (MLSs), the databases that real estate agents use to list properties. This gives us information about homes that non-brokerage websites don’t have, like whether the home has a water view or is located on a busy street. The Redfin Estimate algorithm considers more than 500 data points about the market, the neighborhood, and the home itself. When all of this data meets the massive computing power of today’s best cloud technology, you get the Redfin Estimate.

(bold added by JtR)

More than 500 data points?

Massive computing power?

Today’s best cloud technology?

Those sound great from a marketing perspective. They want you believe that they have developed a proprietary tool that is better than all others – especially better than anything from those dastardly folks at Zillow.

But it sure looks like their estimates are just closely tied to the list and sold prices, not some superior algorithm.

Let’s consider some evidence.

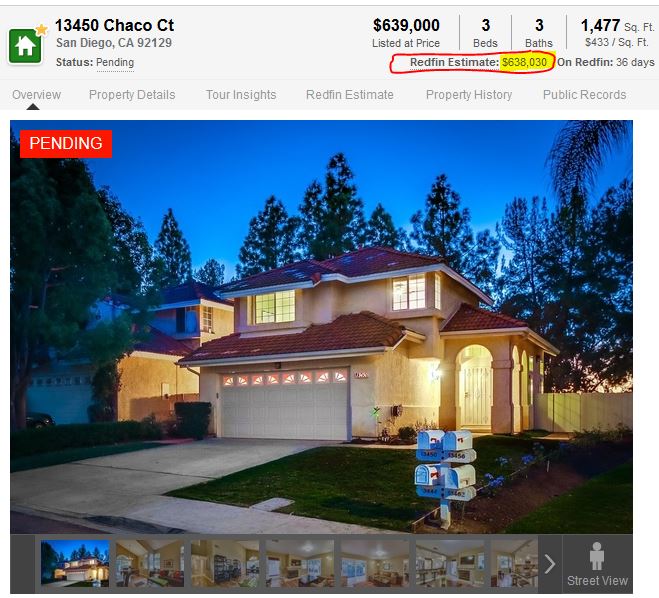

Prior to it hitting the open market, no one would have estimated the value of my listing on Chaco above $620,000. The average cost-per-sf of the solds over the last six months is a lofty $400/sf multiplied by 1,477 sf = $590,800. There was a larger one-story house that had just closed around the corner for $605,000, and the current CMA shows that there hasn’t been any evidence before or since the sale that would indicate a value much higher:

Yet once the listing hit the market, the Redfin estimate is $638,030. The only way it could be that high was if the estimate was tied to the list price, and they add or subtract their 1% to 2% to make it look legit:

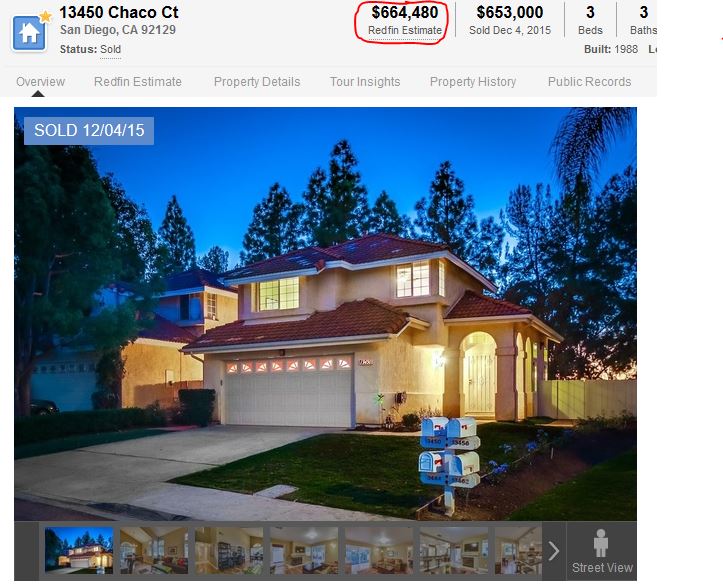

The snip above was clipped the day before escrow closed. Two days later, their estimate rose four percent to 1.8% ABOVE THE ACTUAL SALES PRICE.

But looking at the CMA, there wasn’t any other evidence to support a change in value over the three-day period. It appears that they just added a fairly random 1.8% to the sales price, which kept them within their pledge that half of the sales will close within 1.96% of their estimate:

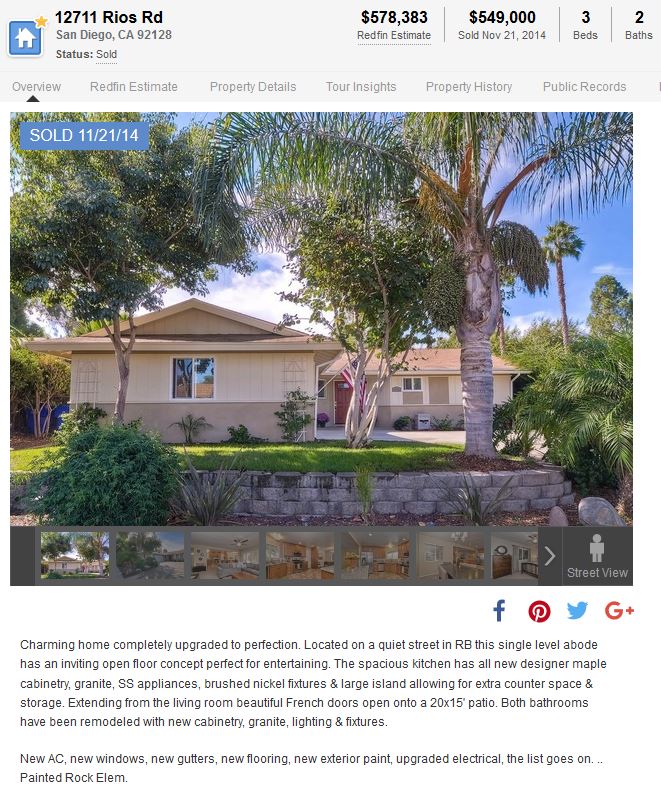

Here’s another example.

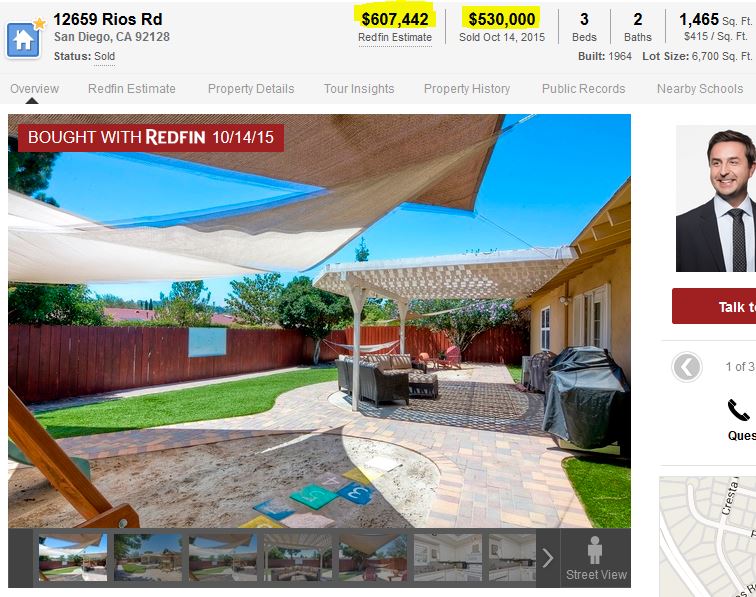

The day the Rios property listed on the MLS, I first snipped the Redfin old ad:

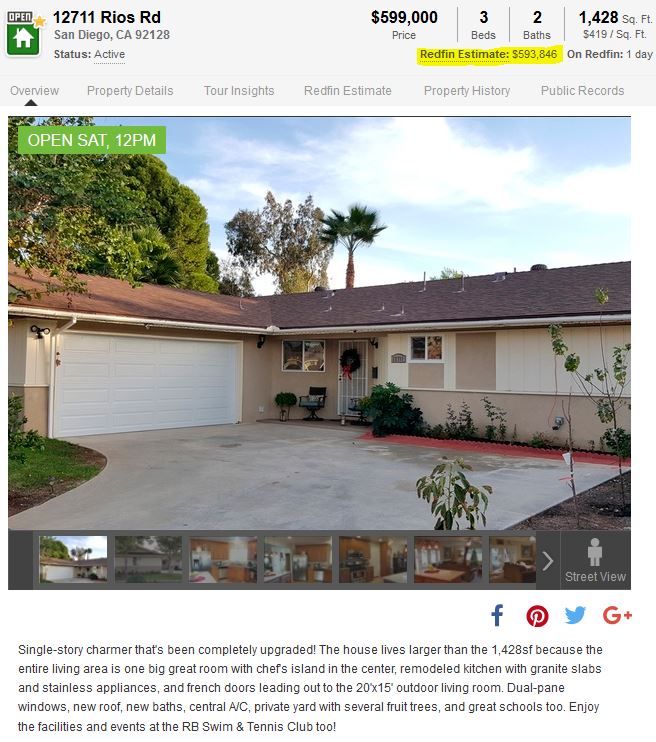

After the new listing was inputted onto the MLS and populated to Redfin, their estimate has magically risen $15,463 in just three hours, to $593,846 – and conveniently within their range of +/- 1.96%:

If all they are doing is adding or subtracting a couple of percentage points from the list and sales prices, then fine – they should state that.

But they give the impression that it’s their new whiz-bang technology that is generating their estimates, and claiming it to be the new and better-than-all-the-rest value estimator.

It also makes you wonder about their end game – will they also use their estimator to hype Redfin agents, and dog the other non-Redfin agents?

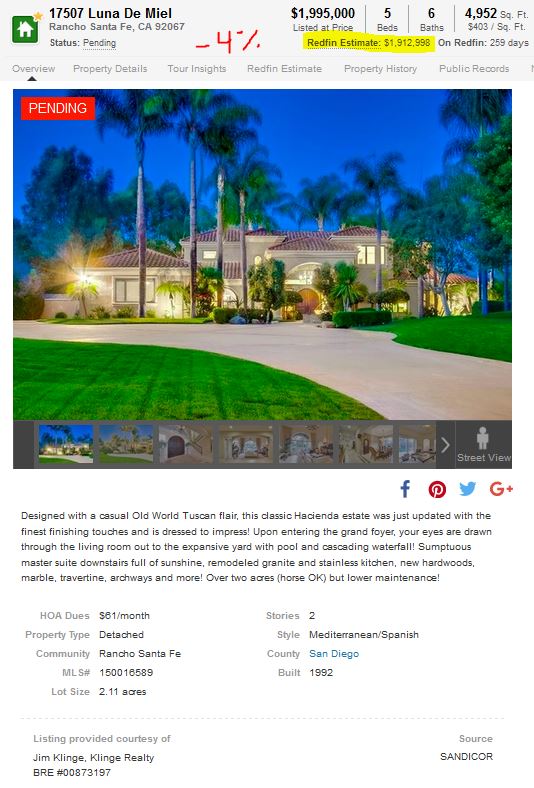

This buyer below was represented by a Redfin agent, and now the Redfin estimate of value has increased a whopping 15% in two months:

They state that their estimate is based on six solds over the last year, and they list the comps. Considering the evidence they provided, do you come up with a $607,442 value?

Redfin will probably be able to shrug off any general criticism of their estimates by just calling it a rounding error. If they are deliberately pegging their estimates to within a couple of percentage points of the actual list and sold prices in an effort to play nice with their fellow realtors, it would be understandable – and playing nice has been their track record.

If they also want to add a little juice to their own agent’s history to make them look better, I guess it wouldn’t be a surprise – heck, every realtor fluffs their sales record.

But this is where they are going to get themselves in hot water.

When a zestimate is below the list price, the Zillow folks are quick to say that it is just a starting point, and to consult with a realtor to pinpoint the exact value. The realtor community will live with that approach.

But what happens when a Redfin estimate is well under the list price?

Don’t the agents who have listings that aren’t selling have a right to be upset with their fellow realtors at Redfin if they have a low estimate? Yes, indeed.

A Redfin estimate – generated by more than 500 data points, massive computing power, and today’s best cloud technology – that comes in low and then is published on one of the most popular real estate websites will publicly undermine the chances of selling the house.

Listing agents won’t tolerate other realtors publishing low estimates online to a wide audience of buyers – especially when the estimates (and motives) are suspect from the beginning.

Lately, the number of weekly new pendings has been higher than last year, and a little under those in 2013 – I’ll take it.

All eyes will be on the Fed’s likely bump of the fed-funds rate on Wednesday, but it should already be priced into the current mortgage rates. We might see mortgage rates drop later this week – current 30Y rate is 3.98%.

Click on the link below for the complete NSDCC active-inventory data:

A family member in a hot market is trying to move up.

They have lost out a couple of deals, so the right kind of frustration is starting to set in, but they keep coming across the same tactic – sellers who want to occupy after closing.

It’s not enough for these sellers and listing agents to get a premium price. On top of that, they make more outrageous demands that gives you the feeling that you’re being toyed with – just to see how high you will jump.

In this case, the sellers are wanting to rent the house after the close of escrow for 90 days at $2,000 per month UNDER the current market rate. There are multiple offers, so they’re figuring one of them will bite.

What are the pitfalls?

The loan documents require owner occupancy within 30 days. Most lenders do random checking by having a fraud detector knock on your door to see if you live there yet. If not, the bank could call your loan due.

Buyers are now landlords, and bill collectors. Try to collect the total rent due at the close of escrow, and a deposit if possible. Most sellers reject the thought of a deposit, so make sure all of the rental terms are clear before signing the purchase deal.

The insurance policy should be for a rental property. If the sellers/tenants fall down and break a leg, you could be sued, and you need the proper coverage.

Sellers asking for 90 days must not have found their next home yet – how do you know that they will move out? Make a provision that any holdover rent will be double the current rate – sellers usually object, but it doesn’t cost them a penny extra as long as they move out as agreed.

Damages? Hopefully a deposit was tendered, but either way, make sure to conduct a Pre-Move-Out inspection so any damages caused by the sellers are acknowledged and remedied.

I told the family member that if they have any major objections to seller rentbacks, then they aren’t desperate enough yet – because it’s likely that one of the bidders will comply with the demands, and you’ll lose another one.

As long as you have a solid agreement in the beginning, you’ll forget all about it six months from now.

If these types of demands are too uncomfortable, there is an alternative. Buy an inferior house – they don’t have nearly as much competition.

It is still hotly competitive on the lower end of each market – this house listed yesterday and I already have two written offers. For buyers looking for a house in excellent condition, there is no off-season:

How many of the long-time owners are selling the family homestead, and downsizing now that the kids are gone?

We don’t know for sure who falls into that category – people with older kids could have bought a house 5-8 years ago and already be empty-nesters. But a growing trend of long-time owners selling could open up some flexibility on price, which could slow down the appreciation trend.

We could also assume that the longer it’s been since the last sale, the more renovating the house could need. The long-timers should have ample equity, which could enable them to cave on price, rather than remodel just to sell. Those who went off to the pearly gates are more likely to have their heirs dump on price too.

Our research department checked the last 125 house sales between La Jolla and Carlsbad – the closings dated back to 11/23/15. These are the number of sales in groups based on when the seller purchased the house:

La Jolla to Carlsbad House Sales – Previous Sale Date

New houses: 3 (2%)

2012-2015: 22 (18%)

2009-2011: 19 (15%)

2004-2008: 29 (23%)

2000-2003: 18 (14%)

0-1999: 34 (27%)

The last two categories combined for 42% of the total sales. Not only are those houses at least 12 years old (most were much older) and probably need renovating, but in almost all the cases, the equity positions were huge.

If there is some future softening of home values, it will be more likely due to the long-timers being more reasonable on price, rather than the ‘bubble’.

Other facts:

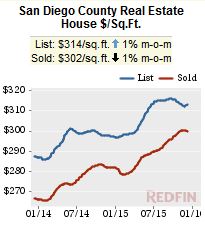

A. The median sales price was $1,080,000

B. The average cost-per-sf was $505/sf.

C. The average market time was 60 days.

D. There were 24% of the total that sold in the first 10 days on market.

E. Eleven sellers sold for less than they paid (9%).

F. In 14 of the sales, the listing agent represented the buyer too (11%).

G. Five were ‘sold before processing’.

The first two categories – homes purchased since 2009 – totaled 33% of the sales. Those sellers enjoyed a nice windfall of quick appreciation, and may be move-up buyers?

Those who bought in 2004-2008 (23%) were probably glad they waited!

When Christophe Choo helped a couple purchase a $15 million Los Angeles home, he wanted to buy them a closing gift that was equally impressive. So instead of leaving a bottle of Champagne in the fridge, he and his wife ushered them onto a chartered jet bound for Vegas.

Mr. Choo, a real-estate agent at Coldwell Banker Beverly Hills, said he spent about $30,000 to accompany his clients on an all-expense paid weekend in Las Vegas, which included suites at the Encore Resort at Wynn and a visit to Tryst nightclub. Mr. Choo said his over-the-top closing gift strategy, which includes giving the most lavish gifts to clients who spend over $10 million, pays off. “My business is 70% repeat clients,” he said. “Creating memories is important.” He declined to say how much in commission he earned on the sale.

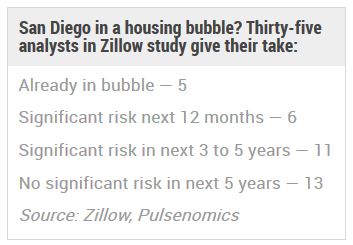

After the recent article by Zillow on whether the San Diego market is in a bubble, the UT conducted their own investigation. Thankfully, they talked to our old friend Rich Toscano:

Toscano, a partner at Pacific Capital Associates, said overvaluation can best be tracked by looking at rent, income and home prices together. In mid-2005, home prices shot up 75 percent over historic median levels. Today, they are 19 percent over those historic median levels.

“Valuations (now) are like prior cyclical peaks but nothing like the bubble,” he said. “A lot of people say prices are like the bubble so that means it’s just like the bubble. So they kind of ignore we’ve had 10 years of rents and incomes going up.”

He said the mood back in 2005 was “you’re a complete idiot if you don’t buy” because housing can only ever go up. An example of the psychology changing is that people are asking all of the time if housing is in a bubble.

“What you really care about is if you are way overpaying,” Toscano said. “Sure, housing is expensive but it is nothing like it was during the bubble.”

The Zillow survey, conducted by Massachusetts-based Pulsenomics, listed the St. Louis market as the least likely to face a bubble with 34 out of 36 analysts saying there was no significant risk in the next five years.

Pulsenomics interviews more than 100 economists, investment strategists and housing market analysts in quarterly surveys. Not all respondents answer every question so the number of analysts responding to the bubble question varies.