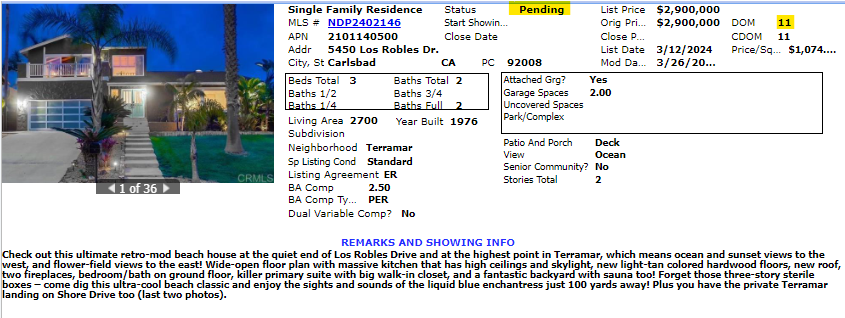

Entry-Level Frenzy

This is as far east as you can get in Oceanside, so it’s not really much a coastal home when it’s 4-5 miles away. But this is a great example of what is happening at the entry level of every market today!

This is as far east as you can get in Oceanside, so it’s not really much a coastal home when it’s 4-5 miles away. But this is a great example of what is happening at the entry level of every market today!

How thin is the margin between winning and losing?

I heard this story yesterday about a house for sale in Carmel Valley.

It had 14 offers.

The sellers selected what they thought was the best offer, and headed off to escrow. But the buyer and their agent had made offers on other properties, and chose a different home instead.

A month later, the subject property is still for sale.

It was unethical what that buyer-agent did, but you gotta keep the losers hanging around, just in case.

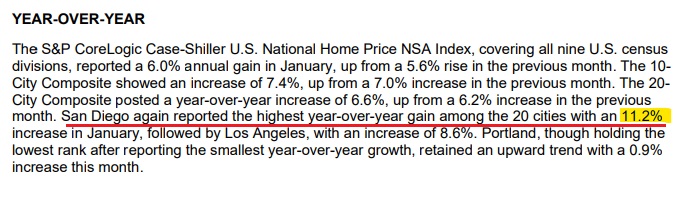

San Diego Case-Shiller Index, Non-Seasonally Adjusted

| Month | |||

| Jan 22 | |||

| Feb | |||

| Mar | |||

| Apr | |||

| May | |||

| Jun | |||

| Jul | |||

| Aug | |||

| Sep | |||

| Oct | |||

| Nov | |||

| Dec | |||

| Jan 23 | |||

| Feb | |||

| Mar | |||

| Apr | |||

| May | |||

| Jun | |||

| Jul | |||

| Aug | |||

| Sep | |||

| Oct | |||

| Nov | |||

| Dec | |||

| Jan 24 |

It has felt like prices have been surging this year, and here is more evidence. The record high was 427.80 in May, 2022, and it should be back to that level by the next reading.

We’re in the midst of all-time record-high pricing today!

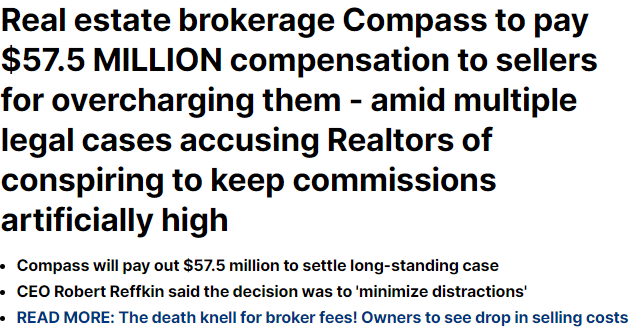

From the CEO of a large Sotheby’s brokerage based in Florida:

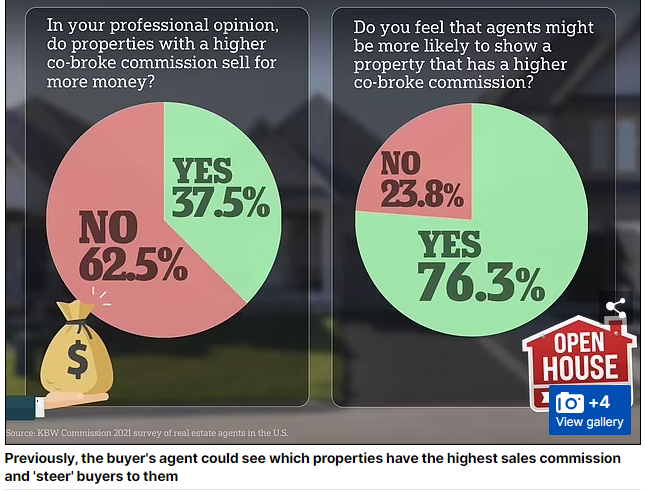

Last week the National Association of Realtors announced a settlement agreement in the Sitzer Burnett case that would take effect in July. For those who missed the declarations in the media that this outcome will render transacting real estate almost free, protect consumers, and make homeownership affordable once again, the settlement does none of that.

Here’s the truth.

1. The settlement forces brokers to reduce their compensation. False.

The settlement in no way establishes a standard or limitation on Realtors for what they may charge, nor services they elect to deliver. Those fees have always been negotiable and there has never been any collective bargaining. In every market, there is a wide variety of fees, just as there are levels of marketing, service and competence.

2. The settlement will, for the first time, allow sellers to no longer pay compensation for an agent bringing the buyer. False.

There has never been an obligation for a seller to pay buyer agent compensation, yet it is a practice that’s worked well. A past rule requiring an offer of some amount of compensation was a rule of display on a Realtor-owned MLS, yet it could have been as low as $1. That limitation was removed and today the MLS accepts all listings, regardless of buyer agent consideration.

3. The settlement prohibits sellers from paying a commission to a buyer’s agent and relieves sellers of the financial burden. False.

The mandate restricts properties with an offer of buyer agent compensation from displaying on association-owned MLS, yet the practice can’t be restricted in any other form of marketing. Sellers may still elect to pay buyer agent compensation to differentiate their properties. While sellers can elect not to pay buyer agent compensation, that doesn’t mean they will avoid the economics as buyers may write into any offer a contingency requiring the seller to cover the cost or request other concessions.

4. The settlement will serve to meaningfully lower prices and make homeownership affordable again. False.

Values in real estate are determined by supply and demand. Fees in a real estate transaction represent additional expenses, yet these include not only commissions but many other related charges. Should real estate commissions be reduced by 1% because of compression, that $500,000 home will now cost $495,000. Not only is the potential impact marginal at best, but do you think the seller now believes the home is worth less and will happily give the difference to the buyer? The reason home ownership is increasingly less affordable is that homes in our market have significantly risen in value these last few years.

5. The settlement is a win for buyers who will now be able to negotiate the fee for representation. Questionable.

For readers who have purchased homes, it is more than likely you were happy to have the seller compensate your agent so you didn’t have to. For buyers who had to provide the down payment and closing expenses, having the commission paid by the seller and incorporated in the home price allowed them to finance the amount over time instead of coming up with additional cash at closing.

6. The settlement will result in significant restitution to consumers who were “harmed” over recent years in their transactions by Realtors. False.

The settlement is huge, yet when one divides the amount by the number of potentially qualifying consumers it works out to about $10 per person. Those benefiting are the attorneys who have submitted a request to the court for over $80 million in fees.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

As a real estate professional for over 40 years, I have had the privilege of working with Realtors who represent the public in what is likely their largest investment. What I have witnessed are the countless situations where an agent has gone above and beyond to help buyers realize their dreams and sellers maximize their returns, often serving in ways far beyond their job description.

Everyone would like to see costs lowered yet I do not see the Department of Justice going after attorneys or other professions we wish would charge less. I always believed in the concept of free enterprise. If one is willing to assume the risk of running a business, one may do so at rates that allow a reasonable return for the capital investment and time. As my dad would say during his 60-year career, you wake up every day unemployed and have to find a job. Then you spend out of pocket and don’t make a cent unless you achieve someone else’s goals.

The brokerage community has always adapted to best represent buyers and sellers whenever there is a shift in the environment. And we will again. Yet when an industry I love is singled out and the justification is for false reasons, I will not be quiet.

Nobody was overcharged, but the media will feed the hysteria for another week or two with baseless claims and lies just to attract more eyeballs! Meanwhile, buyers are hurrying up their quest to buy a home before they have to pay their agent’s commission!

Hat tip to Gerry for sending this in:

I haven’t seen any evidence that paying 3% or higher commission to the buyer’s agent would result in a higher sales price. But those homes offering 2% or less commission usually sell for less, though that is mostly due to an overall weak listing agent, not solely because of the rate.

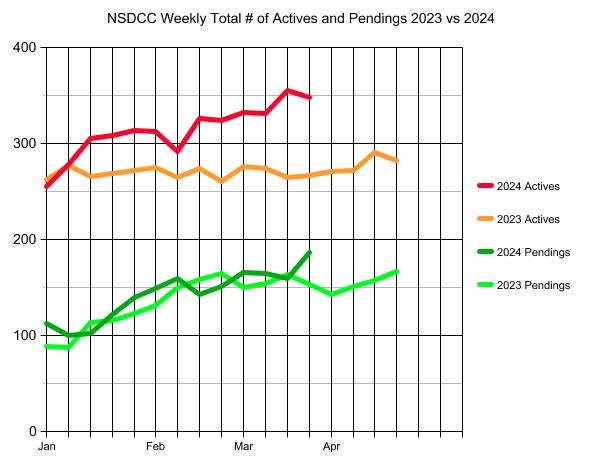

Just when I thought having more active listings might slow the market, the buyers responded!

There were more new pendings (46) this week than we’ve had all year, and they out-numbered the new listings count of 45 – which hasn’t happened in months!

Wow!

The conspiring events – softer market, fewer and less-experienced agents, and lower commissions – are all leading us to the same place:

The destruction of the traditional model of residential real estate sales will be triumphed by the unknowing, but it will be the worst thing to ever happen for consumers because agents will be so tempted to tilt the table.

The only savior will be the company that brings home auctions to the masses.

My only thought when seeing thas property was whether Kellen Winslow Jr would affect the outcome or if whether we are beyond that now. He bought his new for $2,871,000 in 2015 and had to cheap sell it for $2,850,000 in 2019 when he got into trouble.

But even his house resold for $4,800,000 last year, so no lingering after effects, apparently.

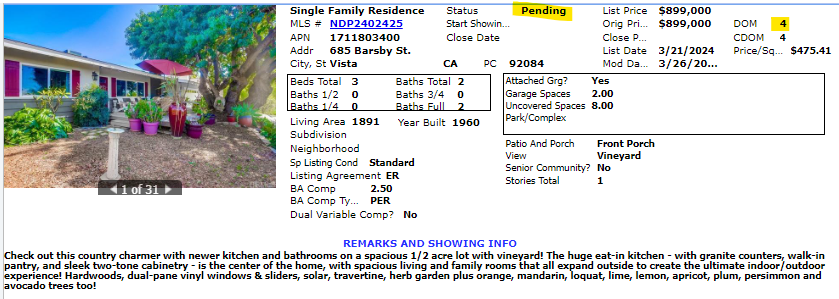

Take a drive to the country and see our new listing in Vista!

685 Barsby St., Vista

3 br/2 ba, 1,891sf

YB: 1960

0.51-acre lot

LP = $899,000

Check out this country charmer with newer kitchen and bathrooms on a spacious 1/2 acre lot with vineyard! The huge eat-in kitchen – with granite counters, walk-in pantry, and sleek two-tone cabinetry – is the center of the home, with spacious living and family rooms that all expand outside to create the ultimate indoor/outdoor experience! Hardwoods, dual-pane vinyl windows & sliders, solar, travertine, herb garden plus orange and avocado trees too! This is a hot buy!

Open house 12-3 on Saturday, March 23rd.

https://www.zillow.com/homedetails/685-Barsby-St-Vista-CA-92084/16628107_zpid/

Are you looking for an experienced agent to help you buy or sell a home?

Contact Jim the Realtor!

CA DRE #01527365, CA DRE #00873197