This is my 748th blog post of the year! (641 published and 107 drafts)

Let’s note how drastic things have changed since rates went up:

NSDCC Detached-Home Sales, December

2012: 297

2013: 223

2014: 255

2015: 259

2016: 241

2017: 225

2018: 196

2019: 229

2020: 290

2021: 183

2022: 95

The best forecasting tool is the number of sales.

Look at how crazy-high the number of sales were in 2012 and 2020. In both cases, the demand had been building up and it really cut loose late in the fourth quarter – in spite of the holidays – to close a third more sales than normal (the average count of the other nine years is 212 sales). Then the two biggest frenzies in history broke out in the following spring.

The number of December sales can help us predict what is coming – and it doesn’t look good for 2023!

We will get our 100 sales once everyone reports their closings, but it’s HALF of the average count.

This year was terrible for many, if not most, agents, and about the best we can say is that we survived. It’s going to get worse in 2023 because there aren’t enough sales to go around. The conditions next year will force many agents into early retirement – why keep paying your dues if there’s not much hope?

You can’t ignore the current predicament and keep doing the same things you’ve done the last 5-10 years. You gotta do better. The industry has to do better.

Here are my 2023 requests of agents:

Publish relevant data that’s easy for consumers to digest. Come up with something juicy that makes a difference, instead of the usual agent blather we see on social media. Printing the number of sales is good, but also add your opinion on what it means – the audience wants hear your interpretation of the data and they will spend a minute or two to get it.

Make it easy to show your listings. If you employ the same hurdles from the frenzy days – like insisting that I send my buyers’ financials just to schedule a showing – then you should pay us more commission to compensate for the hassle.

Will you provide buyers and agents with a walk-through video of your listings please? Let’s preview the homes in advance by video, which will save your time if it isn’t a fit. Adding helpful tips or witty remarks are great, but they are not required. Put the video link in the listing remarks – which is still allowed by the MLS. I don’t see many Matterport 3D tours or any video tours, do you? Let’s upgrade!

We will be having HALF the normal number of sales in the early months of 2023. If we’re not doing it better, then these conditions will persist, and could go on for years.

Every day, we are getting closer to the end. Let’s give it everything we got!

This year was one of the best ever for us. We had our highest sale ever ($7,750,000), our highest average sales price ever ($1,870,835) and more people on my next-year’s client list than ever before – thank you!

The local market between La Jolla-to-Carlsbad fared pretty well too, all considered.

I suggested that there wouldn’t be any sales under $2,000,000 in the Davidson Starboard tract, and there wasn’t (the only one to close escrow since our $2,250,000 sale was across the street at $2,150,000).

I hoped we would have at least 100 NSDCC sales per month, and it looks like that will happen (we have 93 closed this month, as of today). Relatively-speaking, prices have held up too – but sales have plunged, which means sellers aren’t budging much, at least not yet.

Annual Detached-Home Sales Between La Jolla and Carlsbad

Year

# of Sales

Median LP

Median SP

Median $/sf

Median DOM

2017

3,084

$1,250,000

$1,225,000

$441/sf

35

2018

2,799

$1,350,000

$1,325,000

$475/sf

24

2019

2,834

$1,360,000

$1,327,750

$482/sf

27

2020

3,190

$1,499,000

$1,483,750

$517/sf

21

2021

3,184

$1,872,412

$1,900,000

$665/sf

14

2022

1,929

$2,289,000

$2,300,000

$828/sf

15

I will finalize the 2022 numbers next year, but you get the idea – we’re not going to hit 2,000 sales this year, after having almost 3,200 sales in each of the last two years.

Long-time reader GeneK left this comment last night:

The youngest boomers won’t hit retirement until 2030, and most of them will probably live another 20 years or so after that. How long will it be before that estate-sale marketplace takes hold, and will there be a retirement-sale marketplace for a while before that happens?

The housing stock between La Jolla and Carlsbad are generally older homes, with the exception being Carmel Valley. As a result, most of them are owned by the baby boomers, and they don’t want to move! Because they are comfortable with aging-in-place, the inventory of homes for sale will likely be very limited for the next 5-10 years – no matter what the prices are.

The median $/sf went up 25% this year, after going +29% last year!

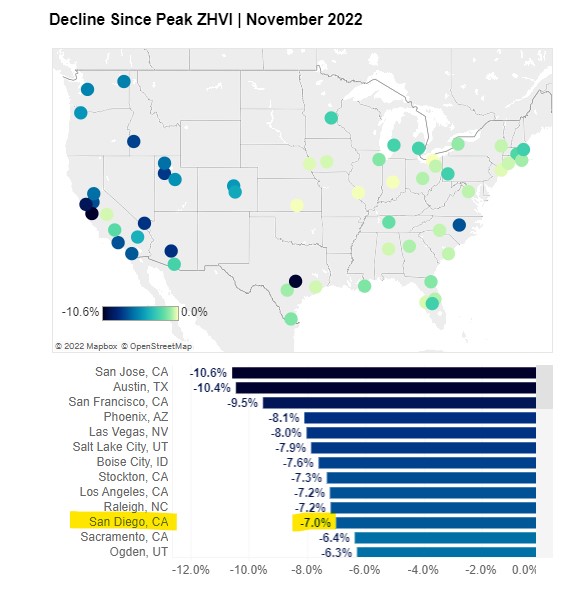

As the national leader of real estate, Zillow is attempting to guide people with data, thankfully. Their Home-Value Index has been decent, and I’ll take the -7% for San Diego….which means our premium areas haven’t felt much decline at all.

Their comment on current conditions isn’t ground-breaking but at least it offers some hope:

Activity in the housing market has slowed to a crawl this winter but the stage is set for a spring thaw: buyers can count on the usual springtime flood of new listings, and less frenzied competition than the last two spring selling seasons in the New Year. But if home shoppers really want to experience some deserted open houses, there’s no time like the present, because this lull won’t last long.

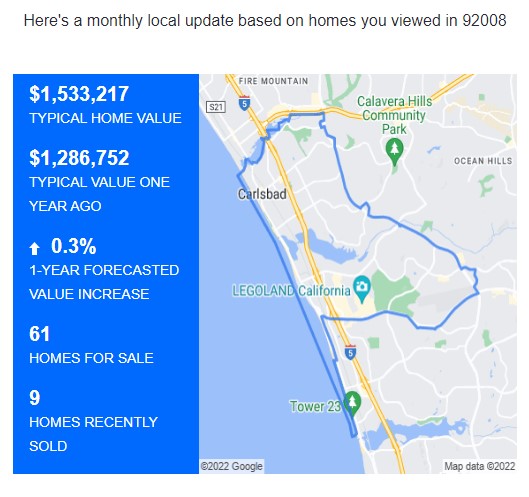

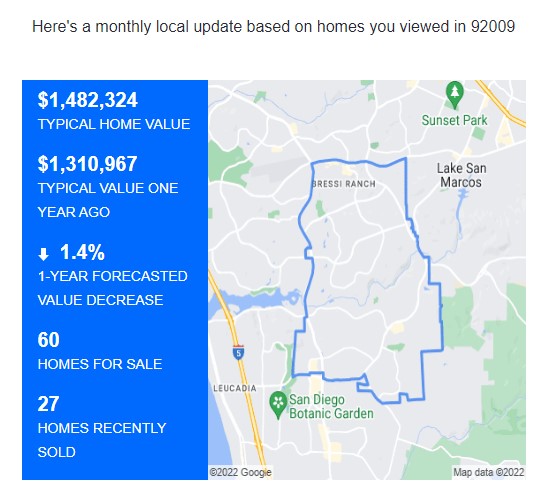

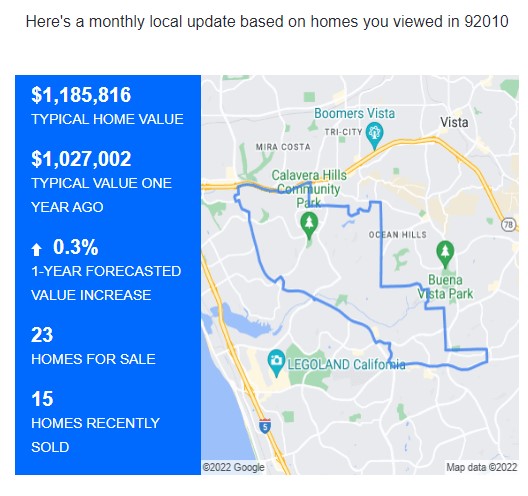

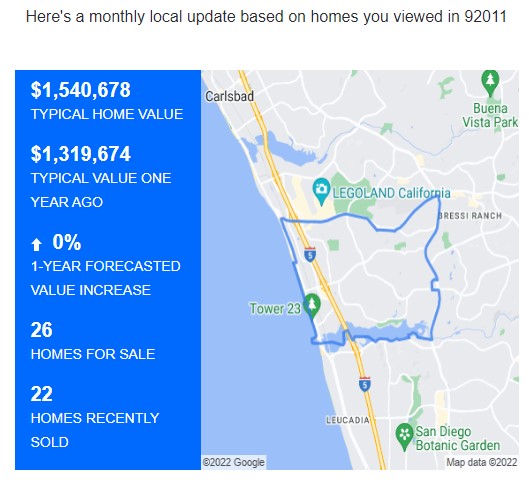

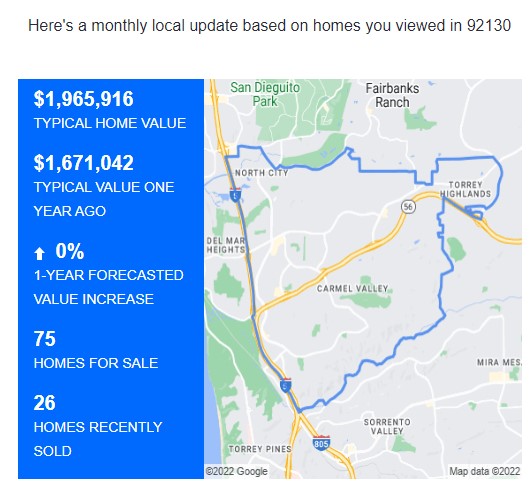

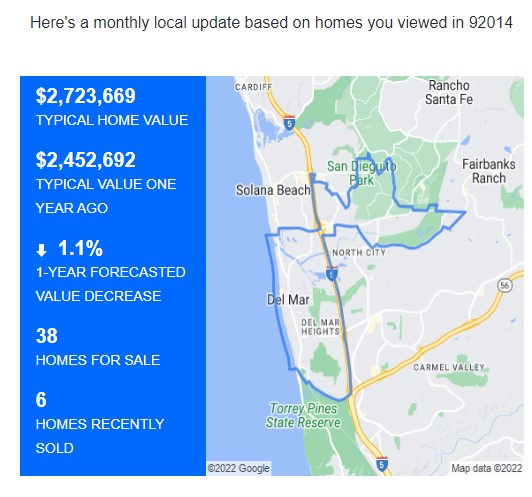

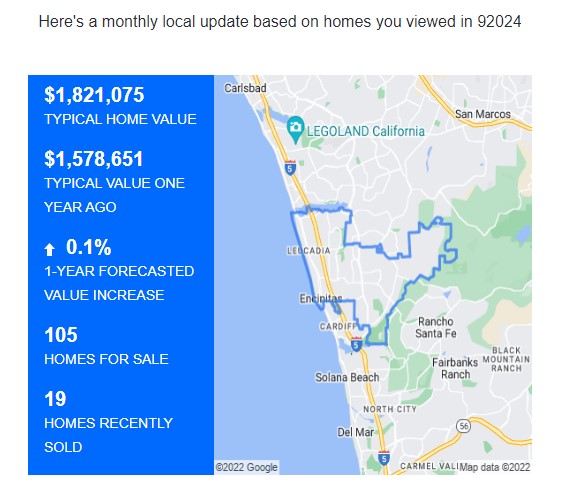

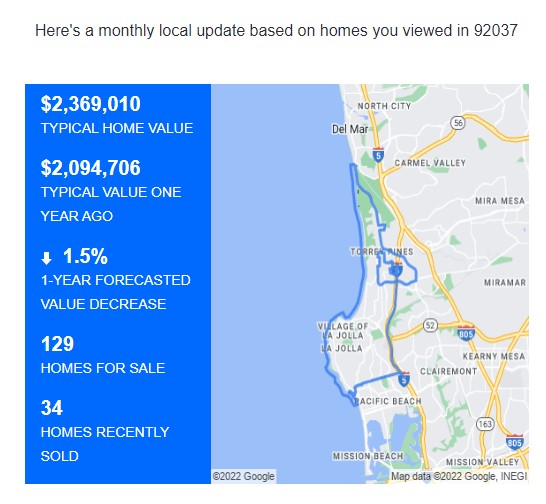

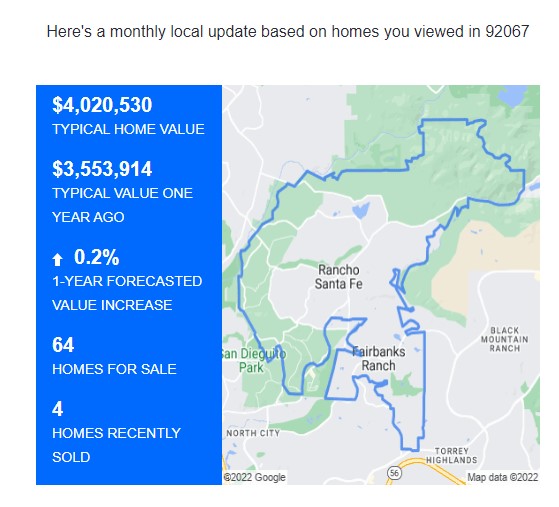

Here are their latest predictions about our local areas, all of which have values that are higher YoY:

NW Carlsbad

SE Carlsbad

NE Carlsbad

SW Carlsbad

Carmel Valley

Del Mar

Encinitas

La Jolla

Rancho Santa Fe

Let’s enjoy our stay in Plateau City – we may be here for a while!

Yesterday, Rob Dawg got started on his prediction on next year’s market:

Is this the official JtR 2021 prediction thread? If so I will post again but for now…

The huge demographic groundswell of house-ready millennials will drive prices much higher. The municipal imposition of covering costs plus will make new supply rare. Money printing drives investment into tangible assets.

Double digit appreciation in the recorded sales. Stagnation in the houses that don’t sell.

The demand is in place between millennials, downsizers, move-uppers, and out-of-towners to easily increase sales by 10% over this year’s record count.

The only hurdle is supply. Will there be enough people willing to sell?

Let’s break it down to a specific number, because we’ll see that achieving 10% more sales isn’t that far out of the question. How many more people need to sell? Here is the breakdown of 2020 listings and sales:

NSDCC 2020 Listings and Sales by Area (as of Dec 30th)

Town or Area

# of 2020 Listings

# of 2020 Sales

Median SP

Cardiff

172

108

$1,707,500

Carlsbad

1,426

1,155

$1,125,000

Carmel Valley

619

482

$1,500,000

Del Mar/Solana Bch

421

259

$2,000,000

Encinitas

618

468

$1,547,500

La Jolla

711

394

$2,262,500

RSF

546

311

$2,710,000

NSDCC

4,517

3,181

$1,479,000

Does my guess of +10% in all categories look and sound crazy?

It looks feasible that we could have an additional 319 sales next year, and get us to 3,500 total. If we pick up an extra 200 sales in Carlsbad, we only need another 119 in the pricier parts of town.

The median price going up to $1,626,900? We know that sellers will be tacking on their habitual extra mustard to their list prices, so $1.6-ish for the year is definitely within range.

Could we have 4,969 listings next year?

This is the big question, but it’s not some crazy number we’ve never seen before – in 2016 we had 5,182 listings and 3,104 sales when mortgage rates averaged 3.65%.

Having an extra 452 houses to sell means 1-2 more listings per day – I wouldn’t call that a flood – and it’s about the right number to whip buyers into a feeding frenzy without creating a glut.

After an insanely unpredictable real estate market in 2020, will our strong sellers’ market continue in North San Diego County’s Coastal region? Probably, but it should be more balanced.

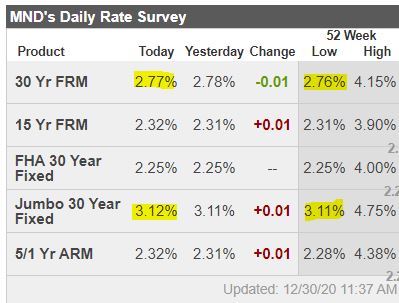

Mortgage rates around 3% (and under) will continue through at least the first half of next year, but how about the low inventory? The number of homes for sale today is 38% fewer than it was last year at this time, so it appears 2021 will start out with the lowest inventory ever for any new year.

But I don’t think it will last.

Do we have pent-up supply waiting to burst onto the market? Here are my categories where I think we will shave additional homes come up for sale, roughly in the order of the most-likely contributors:

1. Move-Uppers – Covid-19 changed what we want from homes. Low rates/high equity make it possible!

2. Baby Boomers – A survey said that half of seniors delayed listing their home in 2020 due to Covid-19.

3. Politics/Taxes – Many Californians have had enough. The migration trend to other states should ramp up.

4. Work From Home – This trend frees up many to move…..up and out!

5. Forbearances – Lenders will be lenient, but some in default will tap their equity, rather than risk losing it.

6. Prop 19 – Enables 55+ homeowners to take their low property-tax basis with them. Though this won’t be the sole reason to move, it makes for a nice sweetener – and may be the last straw to make it worth it.

7. Divorce Rate is Up 34% – Technically,this could add more sellers AND buyers, but realistically those coming out of a divorce will be more likely to split their equity and take a break.

8. Unemployment – Older homeowners will grapple with taking a pay cut or quitting the job-search altogether – and retiring earlier than expected won’t seem so bad when their home’s equity has never been so high. More boomer moves that would have happened in 2022-2025 will be pulled forward.

9. Eviction Ban – In the second and third quarter of 2020, there were 11% of renters who missed a payment. Mom and pop landlords will begrudgingly sell and pay the capital-gains tax, rather than risk another episode like this one.

10. Capital-gains tax. – From the WSJ:Biden will raise the tax on the capital gains of high earners to the same rate as wage income, increasing the rate to 43.4% (39.6% plus Medicare 3.8% investment tax) from 23.8%. Mr. Biden on Thursday estimated that these increases on high earners would raise $92 billion, but that’s before they put their tax lawyers to work. Biden has also said he will eliminate the 1031 exchanges, but all of the above will need Congressional approval. Just the thought could cause landlords to hurry up their plans of selling.

The potential home sellers that are in more than one category (and have more motivation) will be the first out – which means we should get off to a fast start in 2021. We probably won’t see a flood, but it will only take 10% to 20% more sellers to change the game dramatically.

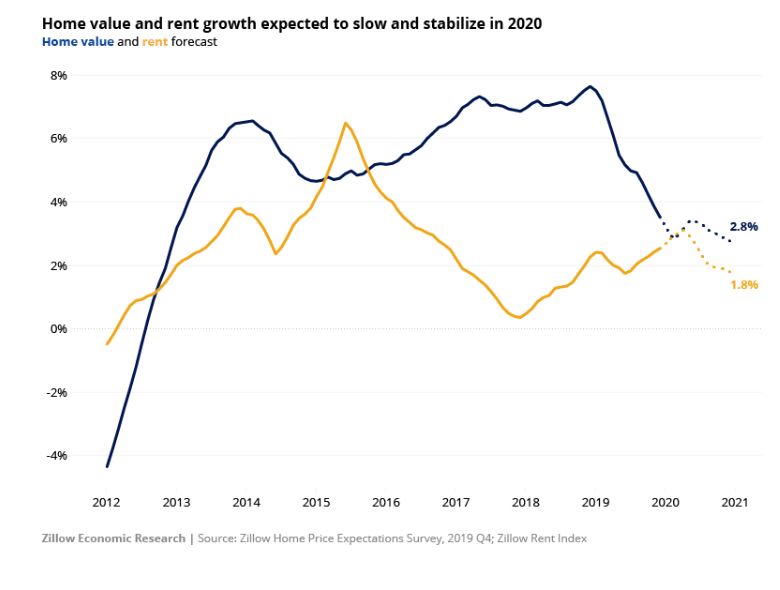

With the housing market stabilizing from the drama of the early years of home price recovery and the subsequent slowdown during 2019’s home shopping season, we have a rare moment of calm to reflect on what housing might look like in the year to come.

If current trends hold, then slower means healthier and smaller means more affordable. Yes, we expect a slower market than we’ve become accustomed to the last few years. But don’t mistake this for a buyer-friendly environment – consumers will continue to absorb available inventory and the market will remain competitive in much of the country.

But while the national story is a confident one, housing in some manufacturing-heavy markets may see adversity. The struggle could be even more stark, since similarly affordable housing markets with a more balanced job profile may be 2020’s rising stars.

There are several 50,000-foot reasons why we expect this gentle downsizing to continue:

Many of today’s younger, millennial home buyers have expressed a preference for denser, more urban homes that are more walkable to shared amenities.

Younger buyers are struggling to afford large homes built in prior decades

Eco-consciousness is also growing broadly.

Today’s older homeowners are expressing a desire for smaller, less maintenance-heavy and more accessible (read: fewer stairs) homes as they age and move into newer homes. In 2019, 56% of new construction home buyers were 40 or older, according to the 2019 Zillow Group Consumer Housing Trends Report.

Home builders are constrained by a shortage of buildable land in desirable areas. Prices on key building materials including lumber and steel are increasingly volatile. And competition for skilled construction labor is fierce, pushing wages up.

Each of these trends points to a continuation of this downsizing of new homes – smaller homes are inherently more dense, walkable and affordable; smaller homes are efficient and eco-friendly; smaller homes require less maintenance and are more accessible; smaller homes enable builders to do more with less.

There will always be demand for large, suburban homes on big lots – but on net, we expect attitudes to shift away from that and toward a lifestyle with a smaller footprint.

Mortgage Rates Will Stay Low, Keeping Housing Demand High

Mortgage rates fell markedly in 2019, and are expected to remain near their current, relatively low levels for the bulk of 2020. Softening GDP growth and investment, continued global weakness due in part to the U.S.-China trade conflict, and below-target inflation will continue to hold rates in check. Barring marked improvements in these indicators, the Fed will have no reason to return to rate hikes.

If low mortgage rates persist, this will keep home purchase demand strong and continue to fuel decent price growth in the nation’s most broadly affordable markets. But low rates won’t be enough to reignite high growth rates in the nation’s highest-priced markets, notably on the West Coast and in the Northeast. In these markets, buyers seem to have hit an affordability ceiling where even low rates can’t bring many homes into the typical first-time buyer’s budget range, especially because low rates don’t help overcome the upfront hurdle of high down payment requirements. In those high-priced markets, buyers will continue to fan out in search of more affordable areas.

Looking ahead at 2020, we think home sales will continue to climb, but slowly. Why?

Although a small fraction of overall sales, new homes sales grew significantly in 2019. That has helped buoy builder confidence and lead to some of the most robust permit and starts numbers in a long time.

If builders in 2020 deliver on their promises to build smaller and at more affordable price points, new construction will continue to be attractive to buyers unable to find a match in the competitive and limited existing home market.

Yes, inventory is tight – but when we say that, we’re really talking about the number of homes available to buy relative to demand from buyers. Sales can remain strong while inventory remains tight – and a sudden jump in the number of sales will result in a corresponding drop in inventory.

What really matters is the flow of homes onto the market – the turnover or velocity of home sales, not months’ supply or overall level of available inventory, that constrains home sales numbers.

And we have reason to believe that turnover among a given segment of homeowners will be made more possible now in a way that it wasn’t before. iBuyer business models, like Zillow Offers, are ultimately about lowering sellers’ transaction costs. Economics 101 says that lowering transaction costs and making transactions themselves easier will mean those transactions will happen more often.

Last year, I guessed that our NSDCC sales would drop 20% due to high mortgage rates, and pricing would stay about the same. Rates dropped instead, and both sales and pricing stayed about the same as the previous year.

In 2020, I think we will see sales drop 10%, just because we’re overdue, and guessing that the NSDCC median sales price might go up 2% to 3%.

We’ve entered the World Of Concierge, where all participants – flippers, ibuyers, and realtors/brokerages – are rehabbing, improving, decorating, and staging most homes for sale. The movement has been building for years, and in 2020 we should see full implementation.

It takes some of the sting out of paying full retail, and buyers really don’t mind paying all the money if they get a turn-key home. Because sellers and agents will be going further to satisfy the retail buyer, we should see more of the softer landing that we saw this year that was caused by dropping rates.

Here’s what Rob Dawg said last year:

Here goes.

Median +4%. Late year inflation and demand for even negative cash flow rental properties. Volume down only 12%. Lots of deck chair shuffling will look like volume. Reported volume -10% from 2018.

$2m+ volume will increase. Lots of quality properties aging out and none of the kids or grandkids can afford to take possession out of the communal estate. Add to this the “too many houses” crowd both casual investors and the very rich who have made their money and ready to throw off the carrying costs.

Almost nothing sub $550k will show up on the sales sheets.

Interest rates will range between 4.4% (early, briefly) and eventually 5.6% (in Q4). Inflation and banking regulations conspire.

There may be a technical recession that will be over before it is confirmed. People will argue whether there was a recession.

Here is a metric we haven’t followed. Total dollar volume of sales will be flat to slightly down.

But what do I know?

We both thoughts rates would be a problem in 2019, but what do we know? It’s hard to believe rates could drop lower in 2020, but if they did get into the low-3s it would ignite the market. Those who have been wanting to move up or down but had a mortgage rate in the mid-3s or higher could now justify moving and getting a lower rate. If California residents pass the referendum to enable seniors to take their old tax basis with them when they buy up in price, it could also ignite sales (if you believe the California Association of Realtors).

What’s Your Guess? The closest guesser will get four tickets to a Padres game!

Mr. and Mrs. Dawg did join us for a Padres game this year (vs. the Red Sox).

Home prices increased on an annual basis by 3.5 percent in October according to CoreLogic’s Home Price Index (HPI). The index rose 0.2 percent from the previous month.

The rate of increase in home prices appears to have stabilized for the moment. After trending higher for several years, the HPI hit a recent peak of 6.62 percent in April 2018, then decelerated to 3.53 percent by the following March. Since then it has moved back and forth over a narrow range, 3.3 to 3.6 percent.

Frank Nothaft, CoreLogic’s chief economist, said “Local home-price growth can deviate widely from the change in our U.S. index. While we saw prices up 3.5 percent nationally last year, home prices also declined in 22 metropolitan areas. Price softness occurred in some high-cost urban areas and in metros with weak employment growth during the past year.”

The CoreLogic HPI Forecast indicates that home prices will increase by 5.4 percent on a year-over-year basis from October 2019 to October 2020. They are expected to increase by 0.2 percent from October to November of this year. The CoreLogic HPI Forecast is a projection of home prices using the CoreLogic HPI and other economic variables.

CoreLogic’s current Market Conditions Indicators (MCI) show 35 of the country’s 100 largest metropolitan areas based on housing stock were overvalued as of October. The MCI analysis categorizes home prices in individual markets as undervalued, at value or overvalued by comparing home prices to their long-run, sustainable levels, which are supported by local market fundamentals such as disposable income. Those markets where home values are 10 percent higher than those long-term levels are considered overvalued and those 10 percent below are considered undervalued. The MCI placed 27 areas in the undervalued category and 38 at value as of October.

During the second quarter of 2019, CoreLogic, together with RTi Research of Norwalk, Connecticut, surveyed Millennials about their housing sentiments. Three out of four told researchers they are confident they would qualify for a loan with their current financial situation. Still, despite this confidence, more than half of the cohort cites buying a home as a stressful experience, noting spending the majority of their savings as one of the leading stressors.

Last December, I had guessed NSDCC sales would drop by 20% this year, but that was back when mortgage rates were touching 5%. With rates back in the 3s for most of 2019, our sales exceeded my expectations – here are the NSDCC detached-home listings and sales for the first 11 months:

NSDCC Detached-Home Sales, Jan-Nov

Year

Total # of Listings, Jan – Nov

# of Sales, Jan – Nov

Median Sales Price

2016

4,984

2,868

$1,165,000

2017

4,500

2,873

$1,225,000

2018

4,689

2,615

$1,325,000

2019

4,573

2,587

$1,325,000

We’re only 28 sales behind last year, and the late-reporters should pull us up real close to 2018.

This year’s sales AND pricing statistics are virtually identical to last year!

There should be more forecasts coming in the next week, but let’s consider what we have so far.

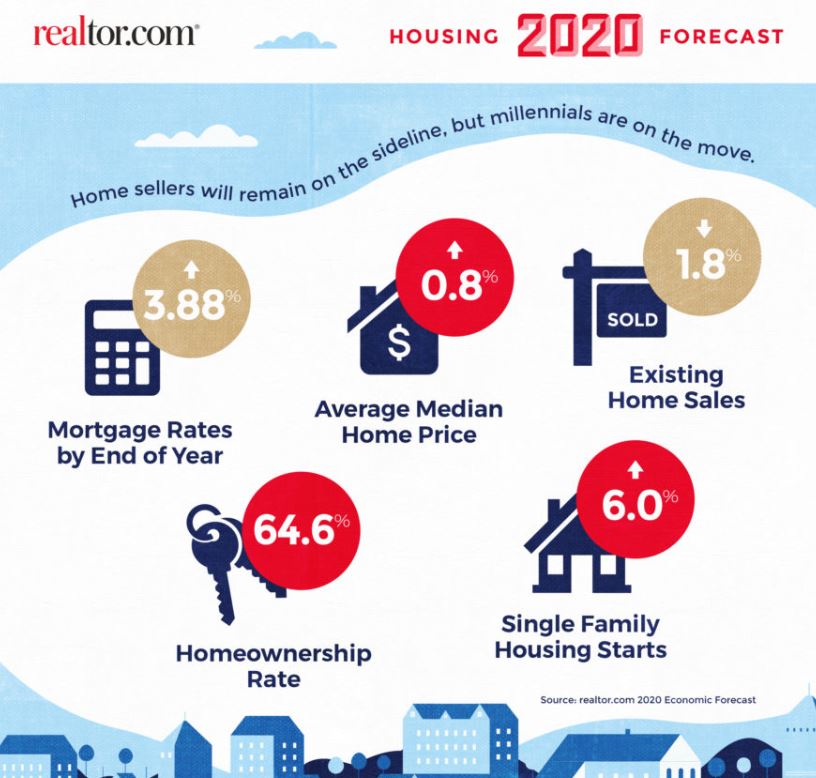

This in today from realtor.com – they have sales dropping in 2020, and prices flat:

Home sales will drop, the housing shortage could become the worst in U.S. history, and home values will shrink in some cities. That’s the 2020 forecast from realtor.com, which holds one of the largest databases of housing statistics available.

Sales of existing homes will fall 1.8% from 2019, according to the forecast. Home prices will flatten nationally, increasing just 0.8% annually, but prices will fall in a quarter of the 100 largest metropolitan markets, including Chicago, Dallas, Las Vegas, Miami, St. Louis, Detroit and San Francisco.

It is a seemingly contrary assessment, given the current strength of the economy and of homebuyer demand, but the dynamics of this housing market are unlike any other — the result of a housing crash unlike any other.

“Real estate fundamentals remain entangled in a lattice of continuing demand, tight supply and disciplined financial underwriting,” said George Ratiu, senior economist at realtor.com. “Accordingly, 2020 will prove to be the most challenging year for buyers, not because of what they can afford but rather what they can’t find.”

They also predict that the San Diego-Carlsbad metro sales will drop by 3.2%, and prices rise +0.2%.

“Low interest rates and a shortage of starter homes will continue to push up prices,” DeFranco said. “This is especially the case for lower price points, since builders have tended to focus on more expensive, higher-profit houses and less on replenishing low inventories of entry-level homes.”

It seems the price growth may continue beyond 2020, too. Data from Arch MI shows the chance of home price declines at a mere 11% for the next two years. There are currently no states or metro markets projected to see prices declines in that period.