It looks like we are going to have an exciting end to the open-house extravaganza today – full report coming later! Meanwhile, we should be more sensitive with those who have trouble going through their stuff – it’s a complex mental health condition!

Hoarding disorder is a complex mental health condition that can have significant implications for both the individual and the surrounding community. By understanding the unique challenges faced by hoarders and implementing appropriate strategies, property managers can create safe and habitable living environments while upholding the principles of fair housing.

Understanding Hoarding Disorder:

According to the International OCD Foundation, it is estimated that 2-6% of the U.S. population, or approximately 6 to 18 million people, struggle with hoarding disorder. Hoarding disorder is characterized by persistent difficulty discarding or parting with possessions, regardless of their value, resulting in the accumulation of excessive clutter.

It affects people from all walks of life, irrespective of age, gender, or socioeconomic status. Hoarders often experience intense emotional attachments to their belongings, leading to extreme anxiety or distress when faced with the prospect of disposal. This psychological condition can pose serious health and safety risks, such as fire hazards, structural damage, pest infestations, and unsanitary living conditions.

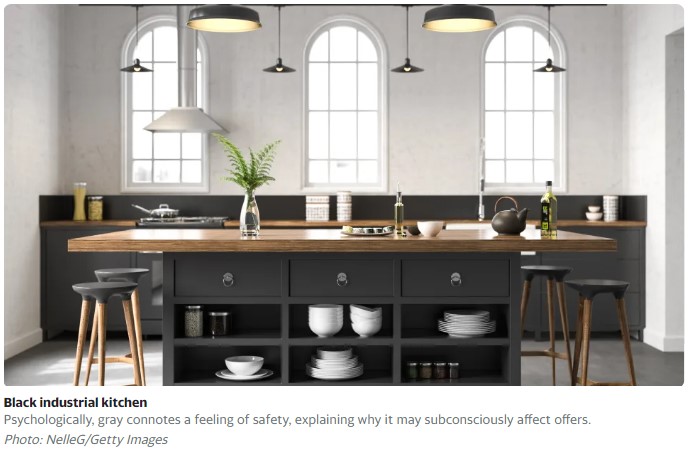

A home should be a visual expression of the person who lives there, right? While this may be true most of the time, the advice could change when it comes to selling your house. According to a new study by Zillow, certain paint colors can make your house sell for more—and some hues can even have the opposite effect. “People don’t buy homes every day, so they’re trying to quickly process a lot of complex information in an area where they don’t have a lot of experience,” Amanda Pendleton, Zillow’s home-trend expert, explained in a statement. “That uncertainty is likely why buyers rely on color as a powerful visual signal that a home is modern and up-to-date, or tired and needs maintenance.”

“Buyers have been exposed to dark gray spaces through home improvement TV shows and their social media feeds,” Mehnaz Khan a color psychology specialist and interior designer in Albany, New York, said in a statement. However, the reason gray paint colors can make your home sell for more might also have to do with more subconscious reasons. “Gray is the color of retreat,” Khan added. “As we come out of the pandemic and return to our hectic lives, buyers want home to be a refuge. They want to withdraw and escape from the uncertainty of the outside world, and rooms enveloped in dark gray can create that feeling of security.”

Home flipping is all the rage, and it complicates the demand for old houses and fixers because there are more flippers than buyers pursuing them.

Agents get calls, texts, and emails every day from flippers begging to buy their listings. They offer to have the listing agent represent them on the purchase, and then be the listing agent when they sell it – boom, three commissions!

Long-time homeowners get inundated with mailers to sell their home for cash, with no commissions, no fees, no repairs, no banks, no nothing – and close any time.

Those who are the most susceptible are the out-of-town heirs who roll in with zestimate in hand and an urge to grab quick cash.

But how much do the flippers pay?

Our listing in downtown Carlsbad – a house built in 1958 and had not sold in nearly 50 years – was a perfect candidate. I started getting solicitations the day it hit the open market and they came by the open houses too. “Jim, Jim, come on you can represent me and we’ll buy it right now!”

We received six offers, and FOUR were from flippers.

The list price was $995,000, and their offers were $800,000, $800,000, $825,000, and $866,500.

Someone called the Carlsbad Police and reported a possible murder, and later a flipper called me and said they have access to the title records and an easement runs right through the middle of the house so nobody is going to buy it – except him.

Thankfully we had two offers over $1,000,000 from owner-occupiers that were more attractive, and we made the deal with one of them.

The worst part of selling to a flipper is that once they tie you up and get into escrow, then they really go to work on you. Even if you thought their price already reflected a proper discount for condition, they will want more concessions later.

But for those antsy homeowners who just want to rid themselves of a headache and get their hands on some fast cash, it is a viable alternative!

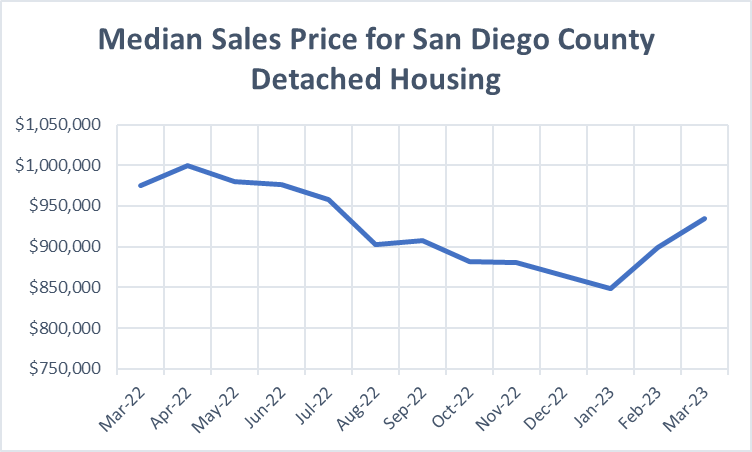

The median sales price for a detached home in the county continues on a seasonal climb. According to our MLS (depicted on the chart below) the median detached home price in March was $934,500. While the median price is down 4.2% from last March when the median price was $975,000, it is up 3.9% from February’s median price of $899,000.

Limited inventory is helping push prices higher, however it is still critical for sellers to price their home right. Multiple sources and personal experience have shown that pricing a home realistically based on local market data will help it sell quickly in today’s market. The danger of overpricing a home is having extended days on market, buyers questioning what may be wrong with a home that has not sold. This likely will result in price cuts and a steeper discount than if the home was initially priced at market.

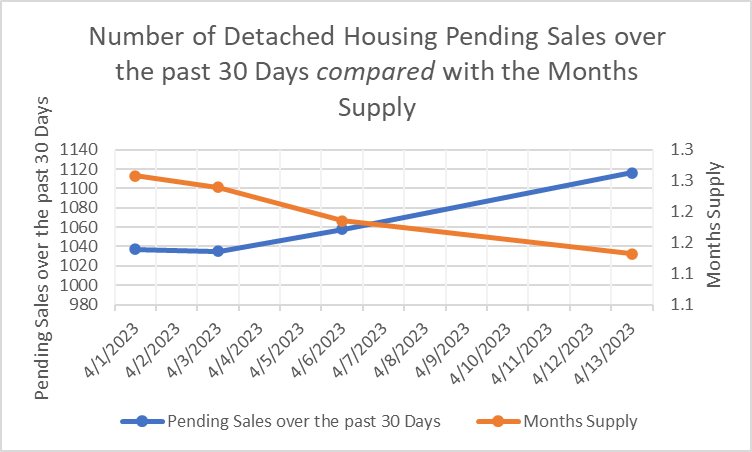

Data from our MLS on the chart below shows the trending increased number of detached housing pending sales over the past 30 days compared with the months supply of housing. It reflects a market with high liquidity, meaning sellers who priced their homes right can expect an offer within a few weeks, at or near their list price.

I would be grateful to help take care of your contacts who are seeking a real estate appraisal to establish a date of death value for estate tax purposes. The IRS has specific guidelines on establishing a fair market value for tax reporting purposes, so it is important to get it right the first time! Appraisals tailored to specific IRS guidelines are my specialty and I am ready to provide your referrals with the best service available, just pass along my contact information and I will do the rest.

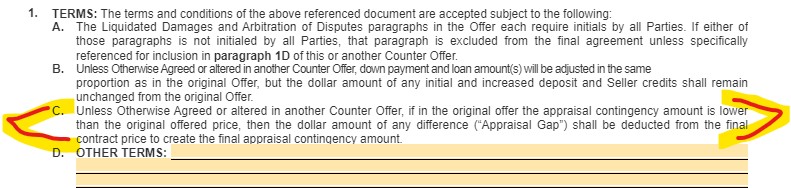

Hat tip to our seller who noticed a new paragraph in the counter-offers this year that went undetected by everyone I know – and we go to the Forms Update every year to hear about changes!

Paragraph 1C in the counter-offer identifies the Appraisal Gap:

When we first read this, it sounded like the purchase price would automatically be lowered to the appraised value without negotiation.

But Gov at the C.A.R. legal office submitted this response:

It means that if, for example, the buyer made an offer of $500,000, contingent on the property appraising at $475,000, and the Seller countered at $520,000 and the buyer accepts the counter, the buyer’s appraisal contingency is automatically adjusted to be $495,000. In other words the $25,000 “appraisal gap” is carried over in the counter. (I admit the language is a little confusing).

Here is the part of the contract that he references:

I’ve never seen anyone put a lower value in Paragraph L(2), but we just started using this version.

The touchy part was that the counter-offer comes later – after the contract verbiage above – which would mean that it would supersede it. It looked like the buyer could waive the appraisal contingency, but then the counter would make it valid again.

A great quote about higher-end listings from this free WSJ article:

Tomer Fridman, a luxury agent with Compass said the prices on some of the homes were exorbitant in the first place, so the reductions represent a long-overdue correction. “When you do a price adjustment at this level, that seller has to make it impactful,” he said. “You have to show you mean business.”

Once a home is for sale but not selling, how do you know what to do? Just dump on price? Lower in small increments and risk irritating buyers? Isn’t there a guide somewhere?

Both buyers and sellers can apply my List-Price-Accuracy Gauge:

Once on the open market, if you are……

Getting visitors and offers, you are within 5% of being right on price.

Getting visitors but no offers, you are 5% to 10% wrong on price.

Not getting visitors, then you are more than 10% wrong on price.

It’s nothing personal, it’s just a simple guide to know how close you are to selling.

The serious buyers rush out the first week to take a look, but after that it’s crickets, with only an occasional visitor. It is tough for sellers to cope, or make adjustments. But once the initial urgency has expired, you have to do something – don’t just sit there.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

How quickly should sellers make adjustments? The DOM clock is ticking!

0-14 days on market – Hot property, sellers have max negotiating power.

15-30 days on market – Buyers get suspicious, want to pay under list.

30+ days on market – The jig is up, and buyers expect deep discounts.

After being unsold for two weeks, sellers will suspect that something is wrong. But it is natural to resist changing the price and instead blame everything else.

Sellers, and agents, need to shake that off and act quickly to keep the urgency higher. The first price reduction should be for at least 5% and happen in the first 15-30 days for maximum effectiveness. If the home doesn’t sell in the next two weeks, then another 5% is in order, and by then the fluff is eliminated.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Where do sellers go wrong? They don’t properly price in the negatives.

Typically sellers just pick apart the comps to convince themselves why their home is the best around, and then settle on a list price that will show everyone who’s the boss. If you don’t have any negatives, then you probably will get your price! But typically sellers are forced to come to grips with the negatives of their house, and adjust accordingly.

Do sellers have to lower their price? No, not neccesarily.

There are other alternatives:

1. Make your house easier to show. Listing agents who insist on buyers jumping several hurdles just to see the home aren’t realistic about today’s market conditions. Make the home easy to see!

2. Fix the problems. New carpet and paint is the best thing you can do: 1) it looks clean, 2) it smells new, 3) you have to clean out your house to install it, and 4) you are managing a business transaction now – it is the logical solution. Utilize staging too.

3. Improve the Internet presence. Have at least a 12-25 hi-res photos and a simple youtube tour.

4.Wait for the market to catch up. If unsold for 60+ days, cancel and try again later – probably next year.

5. Reset the Days-on-Market stat. As long as the MLS allows agents to refresh their listings, then it’s in the best interest of the seller to reset the DOM. It is a gimmick, and instead sellers should concentrate on creating real value for buyers – that’s what will cause them to pay more.

The longer it takes to sell, the more discount the buyers will be expecting – usually about a 1% off for each week on the market. When other homes are flying off the market, the buyers’ obvious conclusion is that your price is wrong, and they load up the lowball offers.

Even if you complete one or all of the five ideas above, don’t be surprised if you need to lower the price too. Keep it attractive!