The wildcard on pricing is that every potential seller has sufficient equity to dump on price if needed.

Why a seller would give it away when there are so many other alternatives (renting, reverse mortgages, hard-money loans, etc.) is beyond me. Even flipper companies like Opendoor (who owns 197 properties in SD County today), have to pay somewhat close to retail to get business.

But there are cases where sellers can, and do, dump on price – like here, where I had the competing listing and we withdrew and rented, rather than give it away:

Those sellers paid $875,000 in 2016, so they still left town with a smile on their face – but you can guess that the neighbors didn’t appreciate it. Especially the two who paid over $2,000,000 just months earlier.

It would take a few desperate sellers dumping at the same time to call it a trend.

But if there were enough of those closings sprinkled throughout the county, the median sales price (a terrible measuring device) could fall 10% or more pretty easily.

When looking at 2023 and beyond, you can probably expect that there won’t be many realtors like me that advise sellers to hold out on price. It doesn’t change their paycheck much if they dump and run, and there won’t be anybody in the press or social media sticking up for sellers either.

There is a chance it could get ugly – just because sellers have so much equity that it feels like free money, and they will still walk with hundreds of thousands of dollars, even if they decide to give it away.

It is a true honor to have listed for sale my favorite home of all-time!

365 Marine St., La Jolla

3 br/3.5 ba, 2,894sf

YB: 2018

LP = $6,950,000

This custom contemporary was designed and carefully-crafted for over three years to be the ultimate beach house just 100 yards from the sand! The main living area has floor-to-ceiling glass panels that open dramatically to create the perfect indoor-outdoor experience with breath-taking 180-degree ocean views over Marine Street beach! The interior is loaded with so many custom features that they make this home downright sexy! Ample off-street parking and an easy walk to the village too. Architect Mark Morris said in his 20+ years of designing super-custom modern-contemporary homes in the area, this is his favorite project of all-time. The ultimate in modern contemporary design – it’s a trophy property!

I don’t care what color he’s seeing, if he sells his tony golf-course estate today and thinks he will buy it back later for less, he will be in for a rude awakening. Without foreclosures (now mostly outlawed in California) causing banks to give away homes, there won’t be any more downturns or cycles. But for those who agree with him, yes – please sell!

Bond manager Mark Kiesel sold his California home in 2006, when he presciently predicted the housing bubble would pop. He bought again in 2012, after U.S. prices fell more than 30% and found a floor.

Now, after a record surge in prices, Kiesel says the time to sell is once again at hand.

Sky-high values, soaring interest rates and other costs of homeownership — maintenance, property taxes and utilities — dampen prospects for future appreciation, according to Kiesel, chief investment officer for global credit at Pacific Investment Management Co. He’s weighing putting his Orange County house on the market and becoming a renter rather than an owner.

“I can look at my long-term 25-year charts and they tell me when to buy and sell and they’re flashing orange right now,” Kiesel, 52, said during an interview at Pimco’s Newport Beach, California, headquarters. “I think we’re in the final innings.”

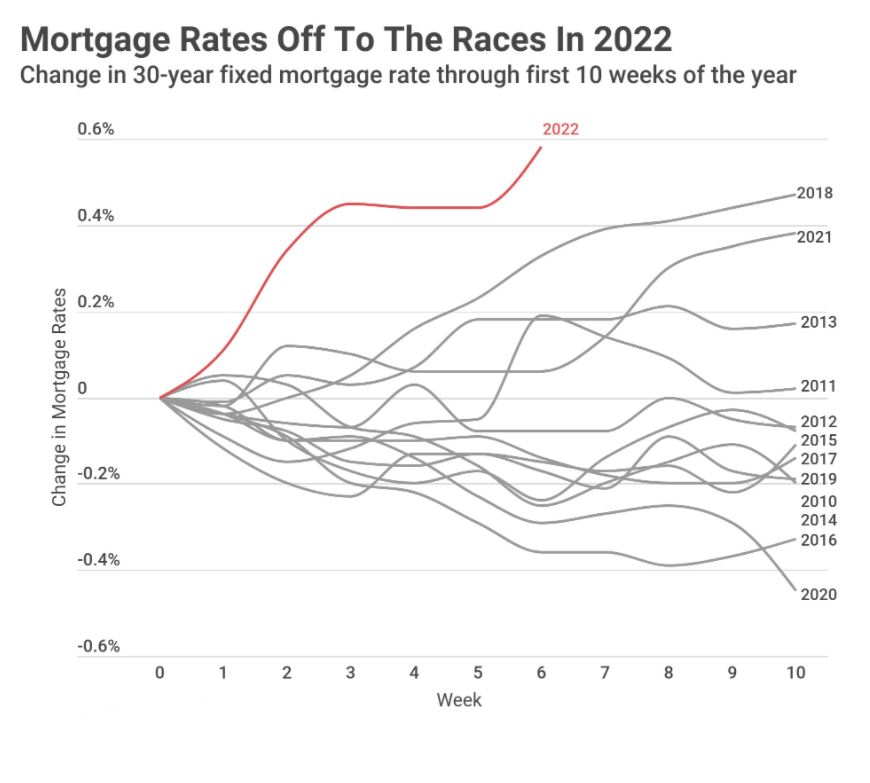

Home prices soared almost 20% in the 12 months through February, according to the S&P CoreLogic Case-Shiller Index, as pandemic moves, low borrowing costs and a dearth of inventory spurred heated competition for housing. But the market is now facing the fastest rise in mortgage rates in decades as the Federal Reserve works to tamp down inflation. The average 30-year rate is now 5.1%, close to a 12-year high, Freddie Mac data show.

Home sales contracts, a leading indicator, fell for the fifth consecutive month in March as rising borrowing costs added to affordability pressures, the National Association of Realtors reported on Wednesday.

Kiesel’s possible sale is a personal move and not a forecast of a crash by Pimco, which in March put out a note predicting “No Bust After the Boom” following years of housing undersupply. “Estimates of this secular shortage range from two to five million houses,” according to the authors.

But Kiesel’s past personal decisions have proved prophetic.

He sold his Newport Beach house in May 2006, calling housing “the next Nasdaq bubble.” Home prices peaked that year before going on to plunge, triggering the global financial crisis.

“It’s not just houses that will be for sale,” Kiesel said in a June 2006 interview. “You’re going to see financial assets for sale over time, and ultimately corporate bonds.”

Then in May 2012, Kiesel decided it was time to own again, buying a golf course-adjacent home.

“For those of you renting or on the sidelines, I recommend you at least consider getting ‘back in’ and buying a house,” he wrote in a credit market note. “The future is hard to predict, but U.S. housing is healing and is probably close to a bottom.”

U.S. housing prices have more than doubled in the past decade and the house Kiesel bought for $2.9 million in 2012 now has an estimated value of $5.5 million, according to Redfin Corp.

Buying a home in today’s market would likely yield about a 2% return, Kiesel said. He considers his home as an investment, refusing to form an emotional attachment to his property.

“It’s only a good investment if you buy it the right time,” he said. “If I were to buy a house today, I would probably get max 2% return on it. And I can find other things I can make money on other than a house.”

When thinking about selling, homeowners (especially the long-timers) complain about paying the capital-gains tax on their net profit above the $250,000 exemption per person. With the rapid escalation in values lately, it has turned into a six-figure tax for many!

Here’s something to think about and I’ll give credit to Doug because it’s been one of the main reasons he has wanted to move. The problem is that people don’t move enough.

Want to avoid paying capital-gains tax?

You should move every time your equity approaches the exemption amount!

The last big frenzy in the early-2000s was fueled by people taking advantage of their tax-free profits by moving repeatedly, and getting rich in the process.

It’s when I came up with my favorite motto:

Don’t Unpack, I’ll Be Back!

Of course, I think everyone should move every 6-12 months – it’s exciting!

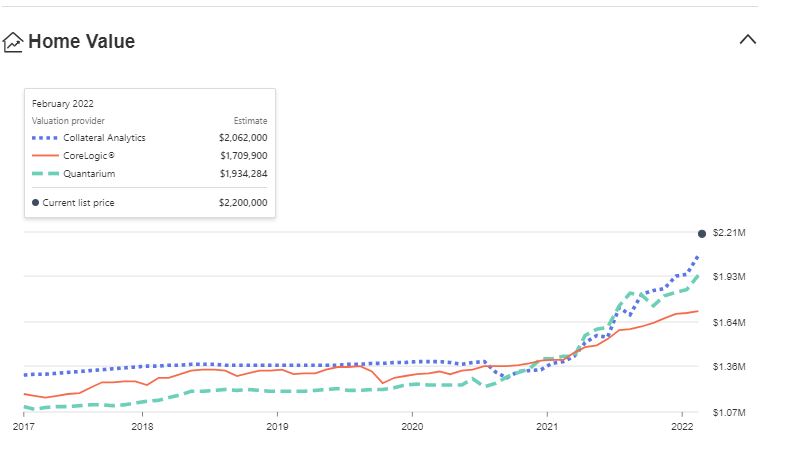

It is amazing how much faith the consumers put into their zestimates and Redfin estimates. In spite of them obviously being ginned up, people just want to believe!

As long as automated valuations are carrying so much weight, let’s include a few more!

There are three more estimates at the bottom of realtor.com listings.

Take the Average? Median? Highest? Lowest?

Sellers will find out what their home is worth when they put it on the open market, so any pricing error will be temporary, and easy to fix.

It’s the buyers who should be concerned about putting too much faith and confidence into the accuracy. Look how it turned out for Zillow’s ibuying venture – they lost between $500M and $800M!

When calculating how much your home has increased in value, you have to identify its COST BASIS – meaning anything and everything that you spent to pay for the product. The IRS defines a capital improvement as a home improvement that adds market value to the home, prolongs its useful life or adapts it to new uses. Minor repairs and maintenance jobs like changing door locks, repairing a leak or fixing a broken window do not qualify as capital improvements.

Capital improvements and things you can put in your COST BASIS include:

The price you paid for the property, including settlement costs, such as: title fees, legal fees, recording fees, survey fees, and any transfer taxes or fees you paid in connection with the purchase.

Additions: An added extra bedroom or bathroom, a deck on the back of the home, a new garage, an added porch or patio….anything that adds value to your home.

Lawn and grounds improvements: Value-adding landscaping projects, driveway or walkway construction, a new fence or retaining wall, adding a swimming pool, etc can qualify as property improvements.

Exterior improvements: New windows, a new roof, and new siding are examples. Any and all renovation costs including ANY and ALL costs related to that renovation work.

Insulation: This includes insulation in the attic, inside walls, under floors, or around pipes and ductwork.

Systems: Installing a new heating or air conditioning system, new ductwork, adding a central vacuuming system, wiring improvements, installing a security system, solar, geothermal, generators, batteries, and putting in lawn irrigation are improvements.

Plumbing: Installing a septic system, water heater, or soft water system adds value.

Interior improvements: New appliances, kitchen renovations, new flooring/carpeting, the installation of a fireplace, etc.

If you needed to make home improvements in order to sell your home, you can deduct those expenses as selling costs as long as they were made within 90 days of the closing. Your COST BASIS does NOT include hazard insurance premiums, moving expenses, or any mortgage-related charges (mortgage insurance, credit report fees, and appraisal costs are out) and general repairs that are essential to keep something working do not qualify. Yard maintenance, HOA fees, and real estate taxes don’t count. Always check with your accountant.

Keeping tabs of these costs throughout the lifetime of a house is wise.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

How do you calculate the capital-gains tax when selling?

Subtract your COST BASIS, commissions, and closing costs from your sales price to determine the taxable gain. Those who lived in the home for two out of the last five years can also subtract the $250,000 exemption if single (or $500,000 if two people), and then the rest is the taxable amount. Long-term capital gains — that is, gains on assets held for a at least a year – are generally taxed at a lower rate than earned income (money that you get from working).

In 2022, the IRS ranges are as follows:

0 Percent – $0-$41,675 Single/$0-$83,350 Married

15 Percent – $41,676-$459,750 Single/$83,351-$517,200 Married

20 percent – $459,751+ Single/$517,201 Married

The State of California will take their chunk too. Check with your tax adviser!

This is the house I featured here when it went on the market on January 12th. It was a little early for the usual selling season but the market has been so hot over the last three months that we dove right in.

The numbers:

Model-match sale across the street in May: $1,450,000 (the list price was $1,299,000)

Realtor.com estimate of my listing: $1,531,100

Zestimate: $1,549,500

Our list price: $1,795,000

Five offers: between $1,800,000 and $1,950,000

Other agents would have grabbed the $1,950,000 and been happy. It was a half-million over the comp!

But I was just getting started. I encouraged every bidder to raise their offer by sending each of them a written counter asking for their highest-and-best offer.

The key point?

The winner who paid $2,100,000 was the buyer who made the lowest offer originally.

In 2021, the practice of countering buyers for their highest-and-best offer went by the wayside. If listing agents do counter, the latest practice is to only counter the top 2-3 offers and ignore the rest.

If I would have done that on this listing, I would have left $150,000 on the table! When the sixth offer arrived late, I still gave them ample opportunity to bid higher too.

When you get multiple offers, you want me in your corner.

Are you thinking of selling? Contact me at 858-997-3801, or klingerealty@gmail.com.

The Super Bowl is complete, and the spring selling season begins today!

Judging by the quick jump in the total number of pendings, homebuyers aren’t waiting around. Mortgage rates have risen faster than any time in the last dozen years, and the number of homes for sale is scary low:

There was heavy activity over the weekend, and on the hot buys, the offers seemed to be starting at 10% over the list prices – which is now the new normal. Waiving contingencies and giving sellers free rentbacks for 60 days will be part of the landscape for the next few months.

Will rising rates cool off the market? Only for those who are on the fringes and sensitive to payment shock. The affluent – the buyers who are controlling the market – are less impacted, and a measly 1% rise in your loan rate only changes the payment by $1,116 per month on a $2,000,000 mortgage.

How long will the 2022 frenzy last?

It should stay hot until one of the following happens:

Mortgage rates hit 5%

A flood of inventory

Mid-summer

By summertime, the pool of highly-motivated buyers should be diminishing, and we’ll be left with those who haven’t been willing to pay these prices. Remember that when you see another crazy-high sales price, there was only one buyer who was willing to pay that much – the rest all wanted to pay less!

I screwed up the national rankings the other day. Donna sent me that clip but it was the 2020 list, not from last year. Anyway, who cares about the national – real estate is local!

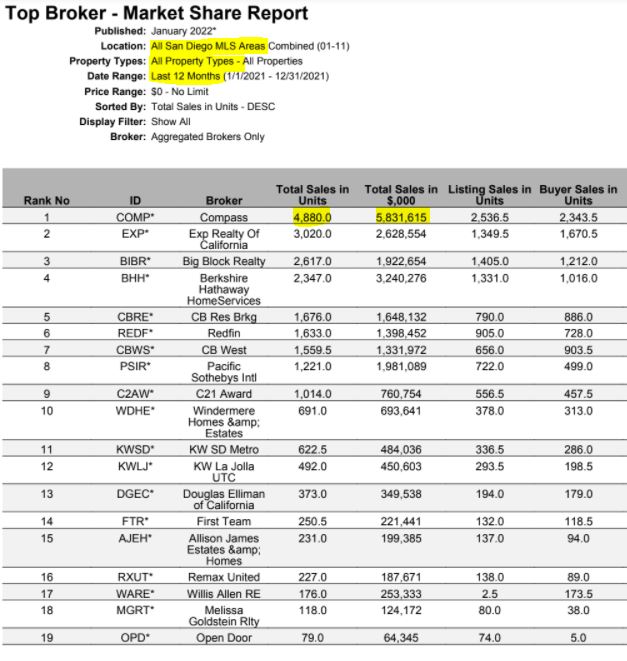

In just 3+ years, Compass has become the dominant real estate brokerage in San Diego County, and it’s not close. Even if you add the two CBs together, our volume last year was almost double any other brokerage.

How will this affect consumers in the future?

As buyer-agents are phased out over the next 1-2 years (and it could happen sooner), there won’t be a need for the MLS. Inputting our listings onto Zillow will become voluntary, and only used if the homes can’t be sold in-house.

It will be just like the commercial side of real estate, where all the good deals are kept in-house, and only when they don’t sell, are the listings inputted onto LoopNet.

It will be the sixth sale over $3,000,000 this year in Encinitas Ranch! With a solid foundation of six sales, the next peak to climb is obvious – potential ER sellers will be wondering if they can get $4,000,000!

Buyers will cringe at the thought, and be reluctant to be the first to pay it. Everything will have to go perfectly for a $4,000,000+ sale to happen.

Let’s identify what could impede such a sale:

Coming Soons – Advertising the property to the public before it’s ready to be shown just diminishes the urgency. By the time a buyer does see it, their dwindling enthusiasm and disappointment has already set in.

Value-Range Pricing – As we head into the post-frenzy era, the gimmicks and sideshows only wear out the buyers. They want the truth, and an easy path to purchasing the home.

Poor presentations – Professional photos and videos will be a must – buyers want to swipe! Once they get into the home, it better look like a top-notch model home to warrant $4,000,000.

Hard to show – Having to clear hurdles like submitting financials just to see the home, having tiny windows of time to see the home, and having the listing agent follow around the buyers like a hounddog only create anxiety in buyers.

Unattractive High List Price – The list price will need to start with a three, to get to a 4-handle. Otherwise, the gap will seem too large, and buyers will be tempted to wait it out.

But even if the sellers and listing agent handle all of the above correctly, it will still come down to how they handle the offer(s) once received. If days go by and then the typical counter-offer is returned with several demands like free rent for 60 days after close, buyer must waive appraisal (or all contingencies), and a higher price than offered, it will be easy for buyers to back away.