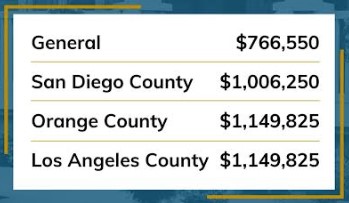

In 2024, you will be able to buy a million-dollar home in San Diego County with 3% down.

Thank you taxpayers!

What will it take to qualify for a $1,006,250 loan? The P&I payment at 7% is $6,695, and by the time you add PMI, property taxes, insurance, and HOA, the total payment will be around $8,733 per month.

It would take an annual income of $325,000 to qualify with only a car payment or two, and no other debts.

Hopefully those earning $325,000 have more than 3% to contribute to the down payment. But if not, it’s ok if you want to opt for the max mortgage interest write-off instead. What a great country!

People might think that 8% mortgage rates will kill the real estate market, but they are one more thing that can be fixed with money.

Two popular strategies to lower the mortgage rate:

30-year fixed rate buydown: Paying one point, or 1% of the loan amount will lower the rate by 1/4%. It would take a few points paid to make a significant difference, and the home seller can contribute too. On a $2,000,000 purchase with 25% down and a loan amount of $1,500,000, the monthly payment is $11,006 at the 8% rate. But the payment can be permanently reduced to $9,358 per month (6.375%) by paying six points, for a savings of $1,648 per month! Hopefully the seller will contribute some or all of the fee.

2-1 temporary rate buydown: Paying 2.4 points will lower the mortgage rate by 2% in the first year, and then by 1% in the second year. With the same $1,500,000 loan, here’s how the 2-1 buydown looks:

In both of those examples, you have a fixed-rate 30-year mortgage. If you are more of a gambler and don’t want to pay any points, the other alternative is to get the 3/1 ARM that has a fixed rate of 6.25% for three years, and then the rate adjusts annually for the remaining 27 years.

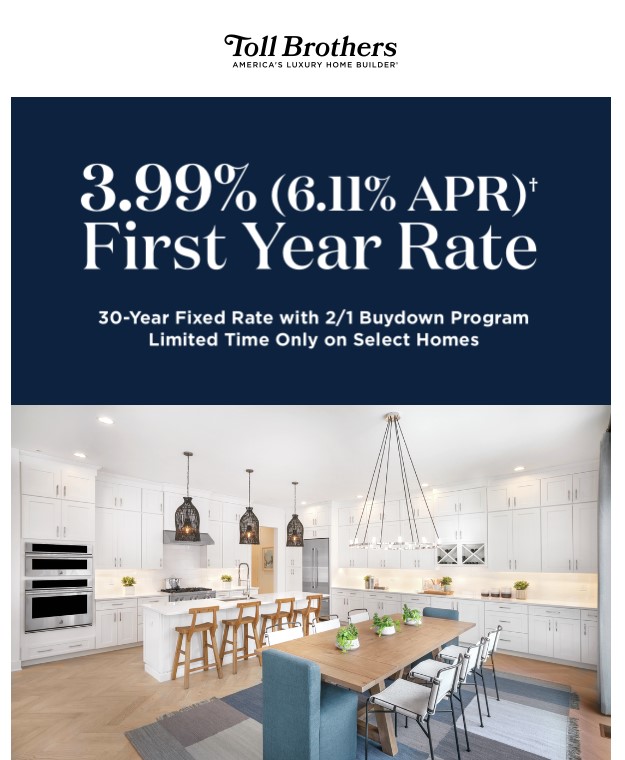

Or you can buy a Toll Brothers home:

A side note on Toll Brothers. Their Del Mar Mesa tract where construction was getting underway? They did sell all of those homes.

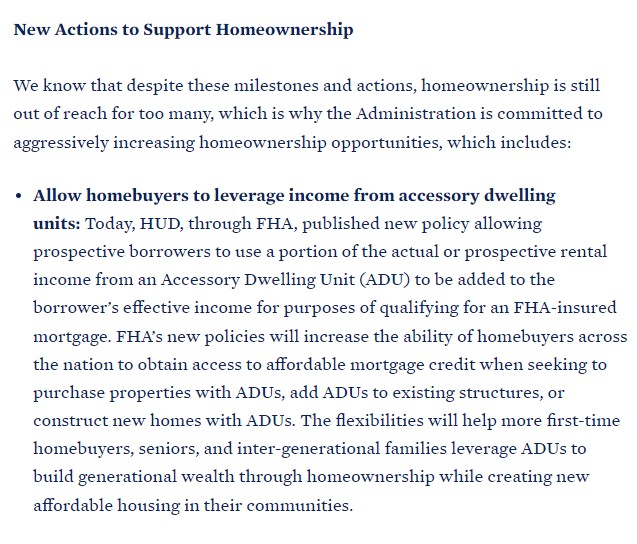

The White House issued a press release today that outlines more money to bolster prop up the FHA loans:

For millions of Americans homeownership is a foundation for so many parts of their lives, and for many it is also their primary source of wealth. The Biden-Harris Administration is committed to expanding access to homeownership, ensuring homeowners can afford to stay in their homes and make the repairs they need, and that the wealth building potential of homeownership works equally for everyone.

Today, the Biden-Harris Administration is releasing new data showing major federal investment in homeownership, and announcing key new actions to accelerate progress. These actions make important strides, but given the lack of homes on the market and current interest rates, to truly ensure homeownership is accessible to all households, we need Congress to act. That is why President Biden proposed $16 billion for the Neighborhood Homes Tax Credit, which would result in more than 400,000 homes built or rehabilitated, creating a pathway for more families to buy a home and start building wealth. The President has also proposed a $10 billion down payment assistance program that would ensure first-time homebuyers whose parents do not own a home can access homeownership alongside a $100 million down payment assistance pilot to expand homeownership opportunities for first-generation and/or low wealth first-time homebuyers.

I love this new way to qualify – they will count the prospective income you might get from an ADU:

Hat tip to the readers who sent in this article found in the tabloid newspaper NY Post. It mentions the Fannie/Freddie fee increase for those with higher credit scores, and fee discount for those with lower credit scores. All the revised policy does is reduce the gap – those with lower credit scores are still paying more.

LLPAs are upfront fees based on factors such as a borrower’s credit score and the size of their down payment. The fees are typically converted into percentage points that alter the buyer’s mortgage rate.

Under the revised LLPA pricing structure, a home buyer with a 740 FICO credit score and a 15% to 20% down payment will face a 1% surcharge – an increase of 0.750% compared to the old fee of just 0.250%.

When absorbed into a long-term mortgage rate, the increase is the equivalent of slightly less than a quarter percentage point in mortgage rate. On a $400,000 loan with a 6% mortgage rate, that buyer could expect their monthly payment to rise by about $40, according to calculations by Stevens.

Meanwhile, buyers with credit scores of 679 or lower will have their fees slashed, resulting in more favorable mortgage rates. For example, a buyer with a 620 FICO credit score with a down payment of 5% or less gets a 1.75% fee discount – a decrease from the old fee rate of 3.50% for that bracket.

When absorbed into the long-term mortgage rate, that equates to a 0.4% to 0.5% discount.

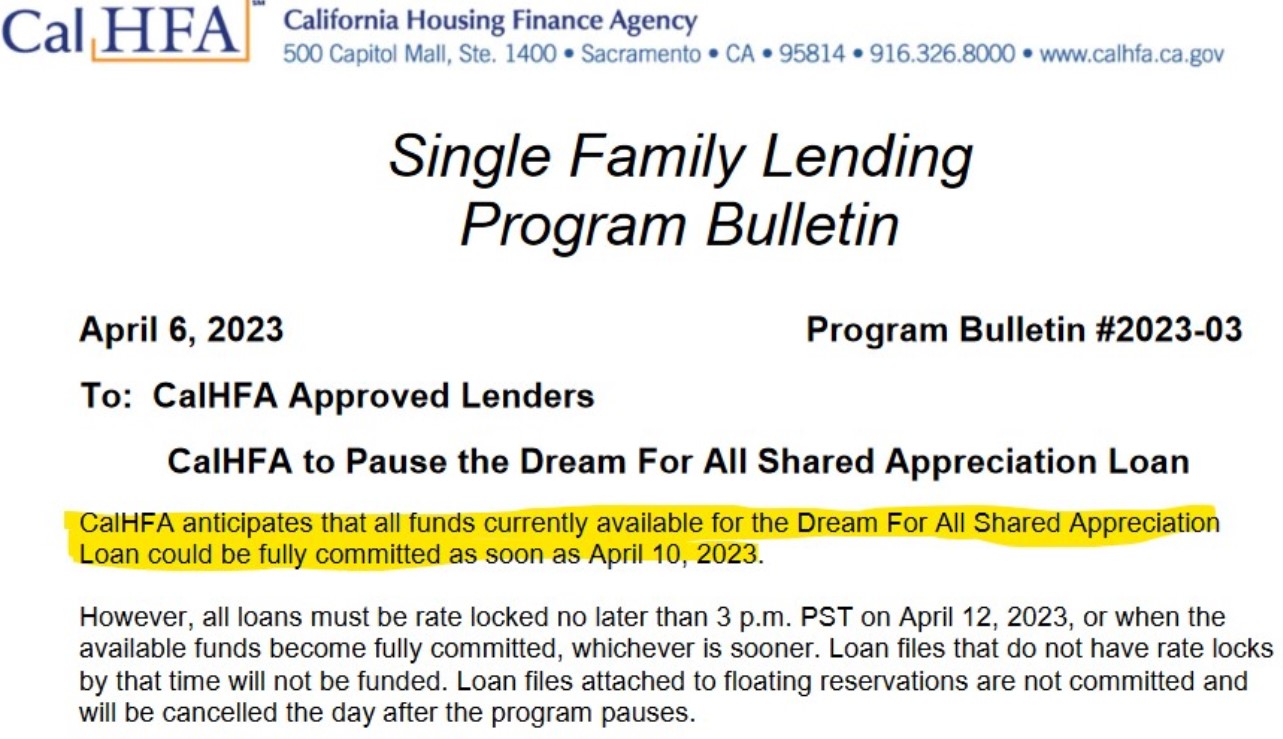

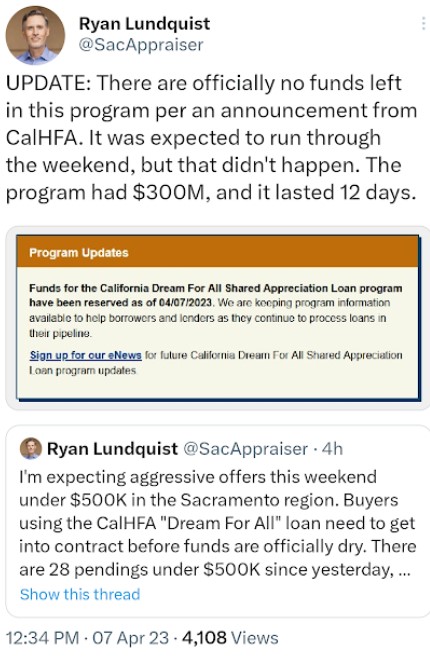

People thought that this program’s $300 million would last a few months.

How about two weeks!

I doubt the homebuyers all found homes already. Doesn’t it have to be that the $300 million in loan preapprovals all happened quickly, and now those buyers are searching for homes at a higher price point than they previously expected?

It probably feels like free money!

It should mean a surge of home sales in the $500,000 – $1,000,000 range throughtout the state.

Thank you California taxpayers!

Added later – it looks like you did need to have an accepted offer:

This is how close we are to a market resurgence. If sellers would pay down 4% to 6% of the loan amount to lower the buyer’s mortgage rate by another 1% to 1.5% and get it into the 4s, we’d be looking good for springtime.

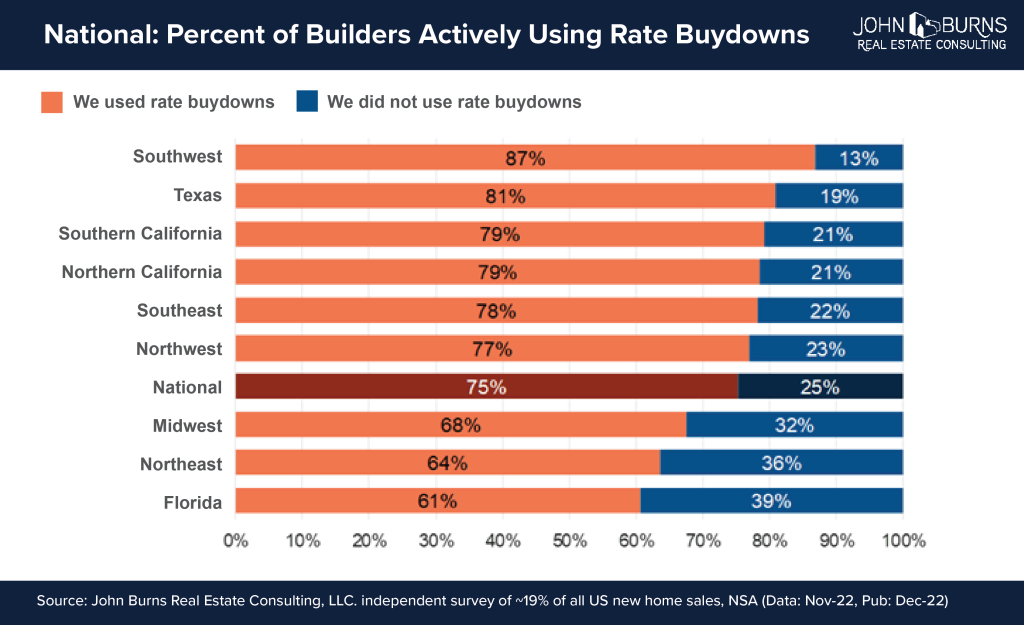

From JB:

In early December, 75% of nationally surveyed home builders confirmed they are buying down buyers’ mortgage rates to make payments more affordable.

Our survey indicates 32% of builders are buying down the full 30-year term and another 30% of builders are temporarily reducing the rate for the first two years of the mortgage. The remaining 13% of builders identified other less common buydowns. Builders pay these costs up front, effectively reducing monthly payments by prepaying for some of the buyers’ interest on the loan. Few resale sellers are offering these savings to prospective buyers.

Two popular strategies involve builders lowering the mortgage rate for the buyer:

30-year rate buydown: Builders are contributing 5%–6% of the home purchase price up front to lower the 30-year mortgage rate by 1%–2% typically. For example, builders may reduce the rate from 6.5% to 5.0% using last week’s Freddie Mac mortgage rate.

2-1 temporary rate buydown: Builders are contributing 2% of the home purchase price up front, which lowers the first-year mortgage rate by 2%, and the second-year mortgage rate by 1%. Using last week’s 6.5% rate, a buyer’s rate would be 4.5% in year one, 5.5% in year two, and 6.5% thereafter. Borrowers still have to qualify at the 6.5% rate to benefit from a reduced payment in the first few years, giving them some breathing room to perhaps spend money on furniture or other needed items.

Because buyers have to qualify at the highest rate that will occur during the 30-year term, builders using the 2-1 temporary buydown tell us some buyers still cannot qualify. By shifting to a 30-year rate buydown, builders can lower the rate and monthly payment used to qualify struggling buyers.

Read the full article with more calculations here:

In the mid-1990s when 30-year fixed mortgage rates climbed over 9%, ARM usage jumped to 35% of all mortgages. In 1999-2000 as 30-year fixed mortgage rates shot above 8%, ARM usage raged once again to 34% of all mortgages. For comparison, the percentage of homebuyers using ARMs today is just 9%, even as housing affordability resides near its all-time worst and 30-year fixed-rate mortgages have more than doubled in the span of 19 months. As noted by the CEO of KB Home during its Q3-2022 earnings call September 21st: “We have some great and compelling interest rates on adjustable mortgages, where it’s a 10-year fixed. And if I were a buyer, I would take that in a minute. Those [rates] are couple of hundred basis points lower than the 30-year fixed, and nobody is taking it so far.”

Back in the day, ARM usage around here was probably more like 2/3s of the loans, instead of 1/3 of mortgages nationally. Rarely did anyone think they were buying their ‘forever’ home, and moving again within 2-5 years was the plan. I used to just go back to my past clients every two years!

It when I coined my all-time favorite slogan, “Don’t unpack, I’ll be back!”

I predict that over the next 3-6 months, the mortgage industry will be heavily advertising alternative loans like the short-term (5-year and 7-year) fixed rate, or the 2/1 buydowns. These were the products that kept the party going after the new 2-out-of-5-year law was passed in 1997, and serial movers could cash out tax-free every couple of years and buy a better home.

It was later, around 2004-2005, that Countrywide developed their toxic version of the neg-am loan, and then was offering 100% financing to anyone with a 700 credit score that the bubble started popping.

I think we are all convinced that the Fed is going to deliberately cause a recession in the next 1-2 years, and will have to lower rates again – and continue their biggest boondoggle in history. Anyone who buys with an adjustable-rate mortgage can refinance to a lower 30-year fixed rate then.

Wouldn’t it be great if the mortgage industry brought back the convertible loan where you could change your ARM into a fixed rate without having to refinance!

The key to igniting the demand will be a 3-handle, and it’s already in some ads:

Some listing agents are offering a seller credit to buy down the mortgage rate, but it’s vague and uncertain. Will it be enough to make a real difference? Do I have to go through your lender to get it?

I think the mortgage industry needs to advertise the specific rates and terms to gain acceptance in the marketplace. Buyers have only been thinking about getting a 30-year fixed, and will be slow to consider an ARM. But it might be the best hope of a softer landing.

Buyer: I’ve had about 40 calls since 7am this morning for mortgages.

I didn’t take any of them and most of them are leaving VMs and texts saying they got notified by Experian that my credit was pulled for mortgage purposes and they want to help. Not sure why and how Experian is sharing my information. I am sure there is a fineprint somewhere.

Lender: It’s not uncommon these days unfortunately. It’s called a trigger lead. Very annoying thing the credit bureaus do.

Here is some info:

What is a trigger lead? When a borrower applies for a mortgage, the three credit bureaus take that information and sell it as a “mortgage lead” to any lender that is willing to pay for it. The “mortgage lead” has the borrower’s name, contact information and the date they applied for credit on it.

Why would someone buy a trigger lead? A trigger lead is a really good indicator that someone is in the process of refinancing or a purchasing a home. A lot of lenders feel this a great opportunity to try to steal the transaction for themselves.

Why is it so bad right now? With interest rates going up and refinance activity going down, most lender’s pipelines have begun to disappear. In response to that a lot of them are buying trigger leads right now.

Why doesn’t your bank do something about this? Unfortunately we do not have ability to block or restrict the credit bureaus from selling this information. This activity is not illegal, it’s legal for the credit bureaus to sell it as they are the owners of the data.

What can we do to help borrowers avoid this? They can remove their information from being sold as a trigger lead. They can do this over the phone or through a website provided by the credit bureaus. Web link here: www.optoutprescreen.com or phone here: 888–567–8688. This must be done before they apply for credit and can take up to 5 business days to process so this may not work for everyone.

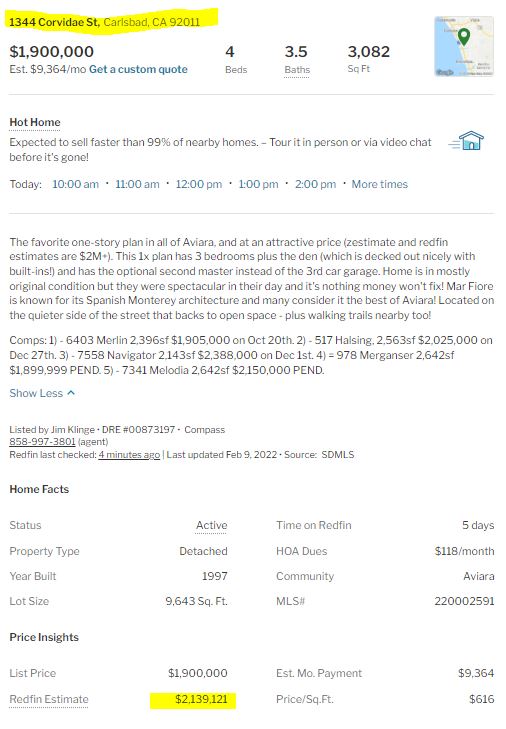

We see on every listing how the estimated values jump all over the place.

On my Aviara listing, the initial estimate was $2,247,615, but once the home hit the open market, the red team lowered their estimate by $313,637 to $1,933,978. A few days later, they have INCREASED it by $205,143 to $2,139,121…….which are some wild swings in less than a week!

It appears that the automated valuations can be wrong by 10% to 20%, and the guys behind the curtain are manipulating them as needed. A scary thought if people are relying on them.

Do people rely on them?

There are probably buyers who are believers, and use them to decide how much to pay for a home.

But it’s even worse for sellers. It’s been happening more and more that home sellers are putting more faith in their zestimate and Redfin estimate. If those estimates are higher than what their agent tells them, of course they want to list for a higher price and they wave around their computerized values as proof.

In today’s frenzy it may not seem to matter much, but there will come a day when accurate valuations will become more necessary.

Or will it?

Rob talks about the changes being made to the GSE’s underwriting guidelines below.

Fannie Mae and Freddie Mac are issuing more appraisal waivers based on automated property valuations! Usually it’s because the down payment is sufficient enough that they aren’t that worried about a default. But once the guidelines are changed, won’t it just be a matter of time before appraisals as we knew them become extinct?

After the TV show, Derrick and I were discussing the good old days when homes were cheap and everyone moved often. He is a mortgage originator, so I asked him how many adjustable loans he has done this year.

His answer? None.

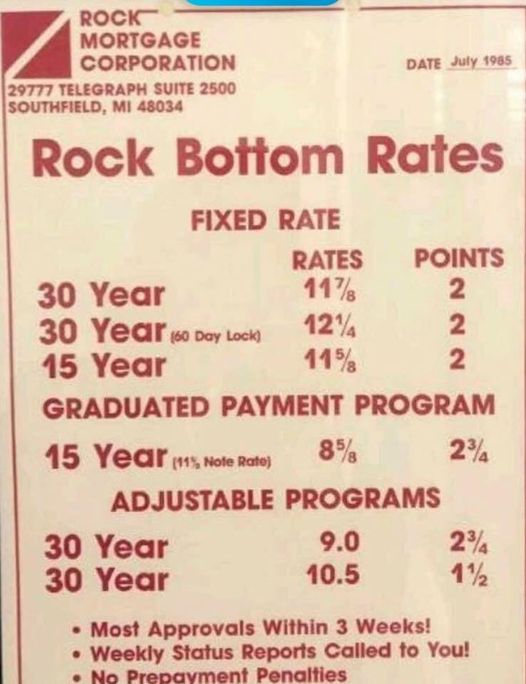

Back in the day, adjustable-rate mortgages were the preferred product. Look at the difference:

$300,000 loan amount

Monthly payment at 11.875% = $3,057

Monthly payment at 9.0% = $2,414

Difference = $643 per month!

Nobody looked too hard at the terms of the ARM because a) $643 per month was a ton of money back then, and b) no one planned to stay forever. Home buyers could always refinance if they had to, but many solved their ARM concerns by moving again – heck, there were lots of homes for sale!

Then the 2-out-of-5-year tax exemption was passed in 1997 which really juiced the market. Homeowners were rewarded with tax-free money for moving!

It was rare that anyone had the full $500,000 in net profit, mostly due to the lower home prices and because of other recent moves. Yet many moved again just to say they got their tax-free money!

At the same time, the mortgage industry, led by Countrywide, flooded the market with an alternative – the interest-only mortgage with a rate that was fixed for the initial period, and you could choose 3, 5, 7 or 10 years. Once those saturated the market, Countrywide stole the neg-am ARM idea from the S&Ls and spiked them with high margins, and, well, we know how that ended.

As the private mortgage companies exited the market, the government lowered rates, and backed Fannie/Freddie to provide market liquidity. For the last ten years, the only program being offered is the 30-year fixed rate mortgage, and because rates are so much lower than before, buyers didn’t mind.

The end result? Today, you never hear anyone buying a home for the short-term.

The combination of ultra-low rates and difficulty of finding a better home has locked in everyone into their current home. Even if the current home becomes unsuitable, it beats moving again.

The low-inventory era is here to stay, and will likely get worse.