We gave credit to the ultra-low rates when they were in the 2%-range for helping to create the frenzy. Likewise, higher rates will have something to do with the way the market turns out in 2022.

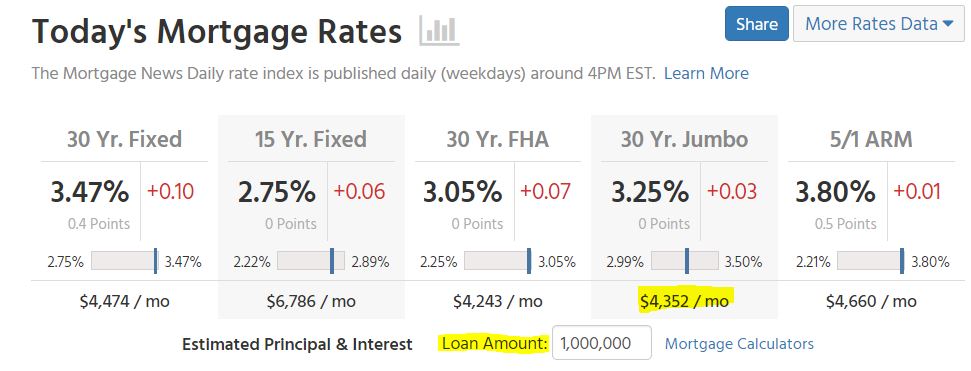

It’s not because the payment are so much different. When the rate changes from 3.0% to 3.85% on a $1,000,000 loan, the payment only changes $472 per month.

The change will be because of the effect that higher rates have on market psychology.

We’re not going to get a memo on the day when buyers decide that they have had enough.

We know what signs to look for – higher market times, declining SP:LP ratios, and a growing amount of active (unsold) listings – to recognize when the market conditions are adjusting, and it’s been quiet so far.

Harder to measure is how quickly the demand could subside.

With the quality homes fetching an average of five offers each (roughly), then for every sale there is probably 2-3 losers that are literally priced out or voluntarily quit the race. At that rate, the demand could be cut in half or less within a couple of months.

Add the war in the Ukraine, rates well into the 4s, and list prices starting at 10% above the comps, and you have all the ingredients needed for a slowdown. Because the market is so hyped up, there will be ample overshoot and the frenzy should last into summer. But everyone knows it won’t last forever.

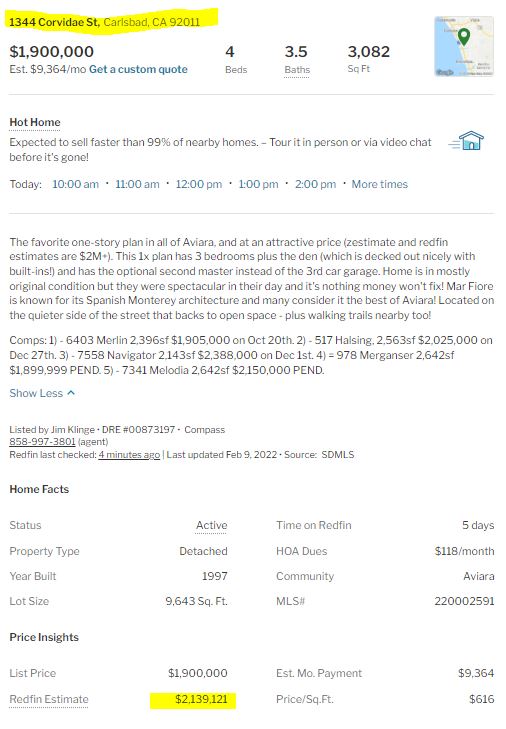

We see on every listing how the estimated values jump all over the place.

On my Aviara listing, the initial estimate was $2,247,615, but once the home hit the open market, the red team lowered their estimate by $313,637 to $1,933,978. A few days later, they have INCREASED it by $205,143 to $2,139,121…….which are some wild swings in less than a week!

It appears that the automated valuations can be wrong by 10% to 20%, and the guys behind the curtain are manipulating them as needed. A scary thought if people are relying on them.

Do people rely on them?

There are probably buyers who are believers, and use them to decide how much to pay for a home.

But it’s even worse for sellers. It’s been happening more and more that home sellers are putting more faith in their zestimate and Redfin estimate. If those estimates are higher than what their agent tells them, of course they want to list for a higher price and they wave around their computerized values as proof.

In today’s frenzy it may not seem to matter much, but there will come a day when accurate valuations will become more necessary.

Or will it?

Rob talks about the changes being made to the GSE’s underwriting guidelines below.

Fannie Mae and Freddie Mac are issuing more appraisal waivers based on automated property valuations! Usually it’s because the down payment is sufficient enough that they aren’t that worried about a default. But once the guidelines are changed, won’t it just be a matter of time before appraisals as we knew them become extinct?

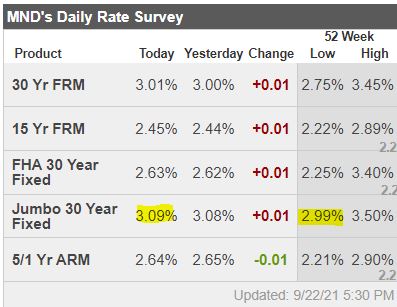

Mortgage rates in the mid-3s in January should put some pep in the buyers’ step. From MND:

Regular readers know that we’re fond of setting the weekly record straight in cases where day-to-day rate movements paint a drastically different picture than weekly surveys. When it comes to the latter, there’s really only one game in town.

Freddie Mac’s Primary Mortgage Market Survey is not only the longest running weekly survey. It’s also by far and away the most widely cited in financial media. It’s even relied upon by the mortgage industry for certain calculations that affect borrower eligibility.

Unfortunately, the rate that Freddie published today (3.22% for a 30yr fixed) is a drastic departure from reality. 3.375% would be an aggressive rate quote this afternoon, and the average lender is closer to 3.50%! A gap of just over 0.25% might not seem like a lot, but consider that it held inside a range roughly half as big for the entirety of the 4th quarter of 2021! It can take months for rates to rise a quarter of a point and we just did it in a few days.

Taking a cash offer is a sexy option but no guarantee to get past the home inspection. The best buyers work with the best agents, and another variable worth considering when selecting the winner.

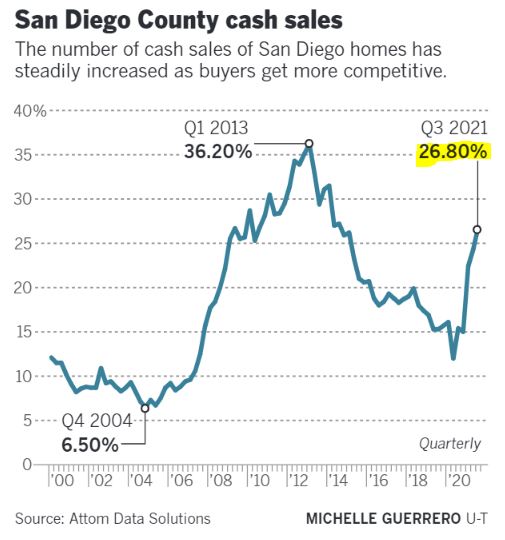

Almost 27 percent of San Diego County home sales were in cash in the third quarter — the highest in seven years. Attom Data Solutions said cash purchases, instead of loans, were up from 15.4 percent at the same time last year.

Sellers typically prefer cash buyers because it guarantees money for the home quickly, whereas mortgages can be delayed — or fall through — for a variety of reasons. San Diego has seen an increase in cash offers before, said Attom records going back to 2000. The real estate data provider said 36.2 percent of homes were purchased with cash in the first quarter of 2013 as the region came out of the Great Recession. At the time, many loan programs were still suspended from the housing crash and that made cash sales more of a necessity. The last highest level for cash sales was in the third quarter of 2014, with 27.2 percent.

The difference now is potential buyers face increased competition for a limited number of homes for sale and are trying to make the best offer possible, said Raylene Brundage, a Windermere agent who sells in several North County communities. “If it’s not contingent on a loan, there is less that can go wrong,” she said.

Brundage said sellers often go for cash sales over other loan types designed for first-time buyers and the military. Those types of loans require appraisals and inspections, making it possible a transaction could be halted. Cash sales not only mean money flows quickly into bank accounts but inspections, which are needed on loans, are often waived. A deal with a mortgage could take a month or longer to complete.

Brundage said she worked with two millennial couples this year who borrowed money from parents so they could make cash offers. Both were successful in getting homes. The majority of cash sales are coming from typical homebuyers, not investors.

Attom said 7.9 percent of the San Diego County sales in the third quarter came from institutional investors, which was lower than much of the nation.

In Atlanta and Phoenix, investors are making up 19.5 percent of sales; in Charlotte, 19.3 percent; in Jacksonville, Fla., 19.1 percent; and Tucson, Ariz., 18.4 percent. Parts of the South and Midwest have some of the smallest interest from institutional investors. In Madison, Wis., investors made up 2.3 percent of sales.

Those who still think we have a foreclosure event in our future are unfamiliar with how the rules have changed in California. There’s never been a better time to be a deadbeat:

The United States Department of the Treasury has approved California’s plan to provide $1 billion in mortgage relief, clearing the way for the California Mortgage Relief Plan to provide help to as many as 40,000 struggling homeowners, according to a statement from Gov. Gavin Newsom’s office. “We are committed to supporting those hit hardest by the pandemic, and that includes homeowners who have fallen behind on their housing payments,” Newsom said in a statement. “No one should have to live in fear of losing the roof over their head, so we’re stepping up to support struggling homeowners to get them the resources they need to cover past due mortgage payments.” California already has provided renters and landlords with assistance, he noted.

“Now, with our California Mortgage Relief Program, we are extending that relief to homeowners,” he said. The program will help homeowners make past due housing payments — to a maximum of $80,000 per household — by making a direct payment to the mortgage servicers.

The funding, which is allocated through the federal American Rescue Plan Act’s Homeowner Assistance Fund, is provided as a one-time grant that qualified homeowners will not be required to repay. Californians at or below 100% of their county’s area median income, who own a single-family home, condo or manufactured home, and who faced pandemic-related hardships after Jan. 21, 2020, may be eligible for the program. Applicants can visit the California Mortgage Relief Program at CaMortgageRelief.org for more information. Online applications will soon be available.

CEO and co-founder: Our approach—which brings every step of the process under one roof—helps buyers separate fear from risk to make more informed homebuying decisions. We are thrilled to bring our reimagined real estate process to create radically different experiences for homebuyers.

It will be radically different alright. They have had seven listings in San Diego County so far, and ALL of the listing agents got their real estate license this year. Their office is in San Mateo.

The disruptors all think this business looks easy, and by hiring a few novices, they can load up on VC money and conquer. But they could have offered the initial plan to all realtors and made their 2% on far more sales than they will with their skeleton staff cutting their teeth on the whole process.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Richard found a company that says they will provide funding for buyers to make all-cash offers, but their website doesn’t mention the program:

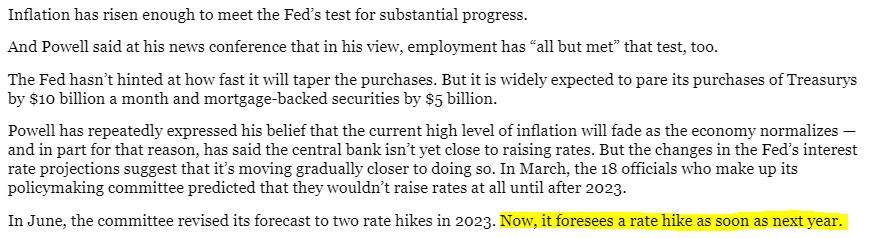

Mortgage rates were surprisingly steady today as the bond market reacted to a new policy announcement from the Fed. Perhaps “reacted” is the wrong word considering the market’s response. Specifically, the bond market (which dictates interest rates on mortgages and beyond) was hard to distinguish from most any other random trading day. That’s nothing short of impressive given what transpired.

So what transpired? That requires a bit of background, but let’s make it quick.

The Fed is currently buying $120 bln / month in new Treasuries and MBS. These purchases greatly contribute to the low rate environment for mortgages.

The Fed has done this, off and on in the past since 2009.

2013 was the first major example of the Fed “tapering” its monthly bond purchases after an extended period of accommodation. Markets freaked out and rates spiked at the fastest pace in years.

Late 2021 is well understood to be the second major example of Fed tapering and markets have been speculating as to when it would become official.

Today’s announcement advanced the verbiage that suggests the Fed will begin tapering at the next policy meeting in November. Then, in the post-meeting press conference, Fed Chair Powell bluntly and explicitly confirmed the Fed is indeed planning on announcing the tapering plan at the next meeting unless the next jobs report is surprisingly bad.

Bonds definitely experienced some volatility during today’s Fed events, but again, that volatility existed within a perfectly normal range. The absence of a bigger market reaction is a testament to the Fed’s transparency efforts.

In short, they ended up saying almost exactly what they’ve been telegraphing in the past month of speeches, and markets revealed themselves to be positioned for an “as-expected” result. So not only was the Fed transparent, but markets were also fully betting on that transparency. Relative to some of the drama in 2013, today amounted to a perfectly threaded needle of epic proportions.

What does it mean for mortgage rates? Today? Nothing really. Lenders barely budged from yesterday.

All of the above having been said, sometimes it takes a few days for post-Fed rate momentum to truly kick in. Additionally, we’d expect some of today’s potential impact to instead be seen in the wake of the next jobs report on October 8th.

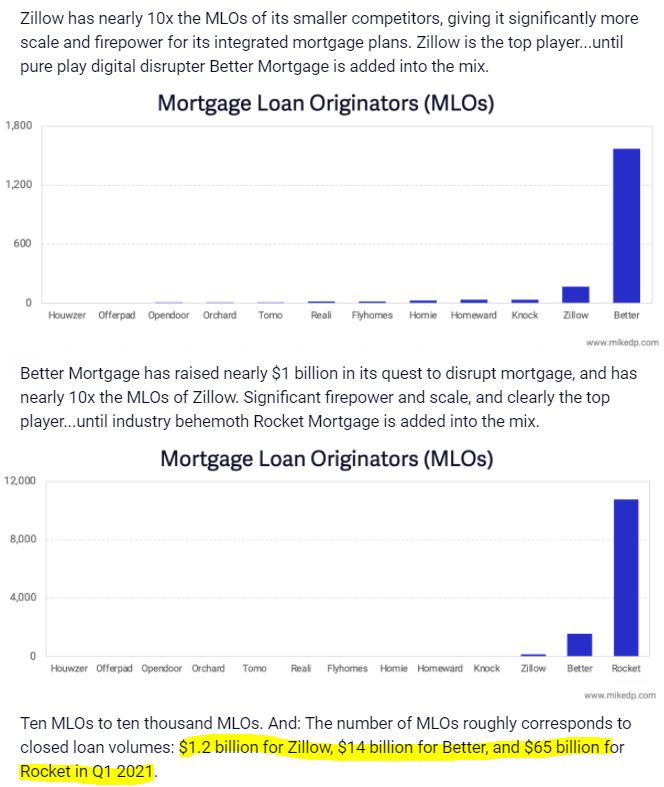

Mike sent out a comparison of mortgage lenders and their quest to disrupt the real-estate-selling business. Here he shows how Rocket is the dominant mortgage lender in the country, and their press release describes their ambition – they think being the jack-of-all-trades will cause them to dominate the space, and now every real estate company will have to offer all services just to keep up. The winners will be determined by who advertises the most:

Rocket Homes, a technology-driven real estate service provider and part of Rocket Companies, today announced it is revolutionizing the way home buying and selling is done in America by seamlessly integrating the tools, professionals and innovations needed to win in a red-hot housing market. Rocket Homes will be the first real estate company ever to create a wide array of choices for those in the market, putting clients in the position to create their own truly bespoke experience, rather than the traditional one-size-fits-all approach that has been the standard for more than a century.

The company is bringing together a comprehensive suite of services that includes: credit reporting, home search, the industry-leading ForSaleByOwner.com process, on-staff real estate agents, a nationwide network of trusted real estate professionals, iBuying services to provide a back-up offer to sellers – along with direct connections to Rocket Mortgage, America’s largest mortgage lender, and Amrock, a premier closing and settlement services provider.

“There is nothing more exciting than getting the keys to a new home, but far too often the process of getting to that point is confusing and fragmented. At Rocket Homes, we are laser-focused on using technology and innovation to create a fully customized and transparent experience that is stress-free and fully integrated – working seamlessly with sister companies to simplify and speed-up the process, all while saving our clients money,” said Doug Seabolt, CEO of Rocket Homes. “Whether a client is looking to sell their house on their own, get assistance from an on-staff Rocket Homes agent or meet face-to-face with our trusted local real estate professionals, we will have unique options and resources to help every client move through the process in a way that is fully customized to them.”

Homeowners looking to sell their property will have the ability to select the right experience for their needs and goals thanks to Rocket Homes Seller Solutions.Through the program, sellers can:

Leverage the industry-leading ForSaleByOwner.com platform that provides sellers all the tools they need to go through the process on their own. This option has become increasingly popular among homeowners in today’s competitive housing market.

Work with highly skilled, on-staff Rocket Homes Real Estate Agents that advise clients on the best list price, facilitate professional photos, list the house on the local multiple listing service, negotiate offers and handle all paperwork. Just like Rocket Mortgage effectively serves clients in all 50 states from centralized locations, Rocket Homes agents will assist with the most complex moments of the real estate transaction from downtown Detroit. With this option – which will be open to the public starting in the fourth quarter of 2021 – homeowners pay a significantly lower commission of only 1.5% for the selling agent, as opposed to the traditional fee of 3% — which represents a savings of $4,500 on a $300,000 home sale.

If a homeowner wants to work with an expert in their local area, they can tap into the Rocket Homes Verified Partner Agent Network of trusted and vetted professionals. This is a nationwide group of the best real estate agents who consistently receive top ratings from the clients they serve. The Partner Agent Network provides the option of a high-touch, in-person experience that some sellers desire. It consists of thousands of professionals working in every state, representing more than 3,000 counties across the country.

True to the company’s promise of providing certainty in complex moments, a soon-to-be-released iBuyer program, facilitated through third-party partner companies, will ensure every owner is given the opportunity to receive a guaranteed offer on their house. Consumers who need to sell their house before buying another often lose out on their new dream home due to the need to make a contingency offer – meaning their deal hinges on closing the sale on their existing property. With the forthcoming program from Rocket Homes, these consumers will now have a guaranteed offer on their current house and can eliminate the need for contingency altogether.

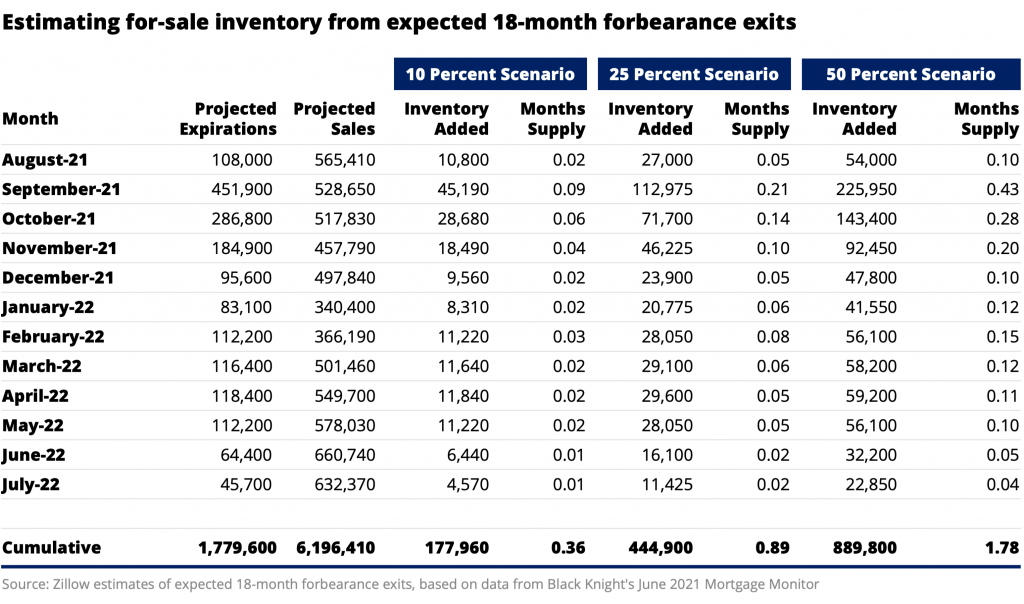

With expiration of a broad federal foreclosure moratorium on July 31, hundreds of thousands of U.S. homeowners are expected to exit forbearance in coming months. A significant share of these homeowners will likely end up listing their home for sale, contributing meaningfully to overall inventory levels and allowing homeowners in forbearance to benefit from home price appreciation and use the equity gained for a future down payment, according to a Zillow analysis.

Unlike 2008, when financial conditions and a souring housing market pushed many homeowners into involuntary foreclosure, strong equity growth and a robust sellers market are likely to ensure that even distressed homeowners have more options and the housing market is likely to be insulated from widespread disruption.

The largest wave of forbearance exits is expected in September and October of 2021, and Zillow projects that forbearance exits will lead to an additional 0.40 months of housing supply in August – October of 2021, a 15% increase relative to 2.6 months of supply in June. For context, this additional 0.40 months of supply roughly means an extra 211,700 homes for sale, which would represent 13.1% of all predicted sales over the next three months.

I hope those in forbearance do list their home for sale – call me today!

The NSDCC market is starved for inventory – look at the differences:

September 14, 2020:

654 active listings

481 pending listings

September 13, 2021:

316 active listings

304 pending listings

Last year we had more than twice the number of active listings as we have today! We can handle more!

But the foreclosure laws in California were significantly modified and nobody is going to get foreclosed – so don’t wait around for that to happen. The most likely scenario is for the lenders to continue the free-rent program for another year or two, and only lightly suggest a potential sale to those not paying their mortgage – which will only sprinkle an occasional new listing upon us.