Part of a nice flurry of July sales that are inline with the monthly sales counts in March-June. But the median sales price has a month-over-month change of -17%, which will cause the doomers to flip out. But it’s only because there were a bunch of lower-end sales this month.

Your home’s value didn’t drop 17% in the last 30 days!

More plain talk from Steve about home prices and future appreciation rates. He is talking to realtors.

What I sent to Steve:

Hi Steve,

I enjoyed your deep dive today and also put it on my blog where local realtors are known to hang out.

You mentioned that you are studying the locked-in effect.

I don’t think it has the effect people think it does, and I’m not sure there is any effect.

Why?

The extreme difficulty of finding a superior home.

The extreme difficulty of winning a superior home, once you find one.

Paying capital-gains taxes on the sale of the previous home – and usually six-figures of taxes.

Higher property taxes for most, even in California.

Start the 30 years over again on the mortgage – which those extra years should be a bigger hurdle than the higher rate for those who analyze the differences in costs.

Then pack up the stuff and uproot everybody and everything from the previous house to start fresh in the new place….and hurry up with the $25,000 to $50,000 in repairs and improvements that literally every buyer has to do when buying a resale home.

We will only know if there is a locked-in effect if rates plunge to 3% again, which is very unlikely. So it’s all just fodder for the twitterverse.

But if rates did plunge – even to 4% – then we’ll find out that homeowners are still reluctant to move.

Then the problem will be re-labeled as the Forever-Home Effect.

San Diego is the #1 area that homeowners don’t want to leave! Don’t you get the feeling that we are going to out-perform every other real estate market in America for a long time to come?

Today we have 2,293 active listings of attached and detached homes in the county – population 3.3 million!

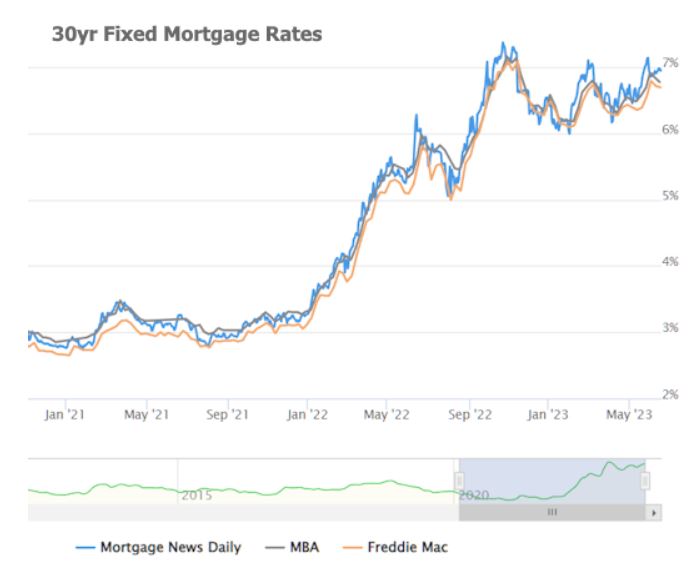

Powell’s goal was to crush the real estate market…..

In June 2022, Powell told reporters that spiked mortgage rates would help to “reset” the U.S. housing market, and that “we need to get back to a place where supply and demand are back together and where inflation is down low again, and mortgage rates are low again.”

Then in September 2022, Powell told reporters that we had officially entered into a “difficult correction” that would restore “balance” to the housing market. At the end of November 2022, Powell went a step further, and said a “housing bubble” had formed during the Pandemic Housing Boom.

Last week, Powell said, “The housing market is bottoming and may already be improving.” He made the comment after the central bank kept benchmark rates steady but indicated more hikes may be needed later this year.

“Activity in the housing sector remains weak, largely reflecting higher mortgage rates,” Powell told reporters after the rate announcement. “Certainly, housing is very interest rate-sensitive, and it’s the first place, really, or one of the first places, that’s either helped by lower rates or is held back by higher rates. And we certainly saw that over the course of the last year. We now see housing putting in a bottom and maybe moving up a little bit. We’re watching that situation carefully.”

In his prepared statement yesterday, he said, “Although growth in consumer spending has picked up this year, activity in the housing sector remains weak, largely reflecting higher mortgage rates.”

Then he said,“We think housing inflation will be coming down significantly over the course of the rest of this year and next year. Consumer inflation has eased since last summer due mainly to falling energy and core good prices. In contrast, rents and other housing inflation has been moving higher.”

What he doesn’t see…..

Powell’s comments get turned into headlines, like this:

Potential home sellers take one glance and – even though they aren’t quite sure what he means – they decide the market is no good and that it’s smarter for them to wait for better times. It would take a flood of supply to effectively reset the real estate market, yet his policy is doing the opposite. Plus, his higher rates are pricing out the marginal buyers (the regular people), which creates less competition for those who can withstand higher rates – the affluent buyers.

The end result is affluent people chasing the few sellers who really need to move – just the type of buyer who can, and will, pay more to get what they want now….which will help to keep prices elevated.

What’s likely to happen:

The off-season will commence shortly and there will be fewer sales than ever, with an occasional deal here and there. The trendline will look softer than during the selling season, which will cause Powell and others to abandon the bottom talk and instead declare that their ‘housing inflation’ – code for rising prices – is coming down. Everyone will take it as a sign that the recession is finally here!

Then the 2024 selling season will get rolling in February, confounding the experts even more.

It might take a couple more years before they start believing that home sales are seasonal – if they ever do.

My thoughts below on how this year should wrap up. Buyers don’t have any reason to rush anything because rates and prices don’t seem to be going anywhere over the next few months. It will cause them to be extra picky which will tempt everyone to look ahead to the next selling season. We’re going to the game tonight with Natalie and Ryan – go Padres!

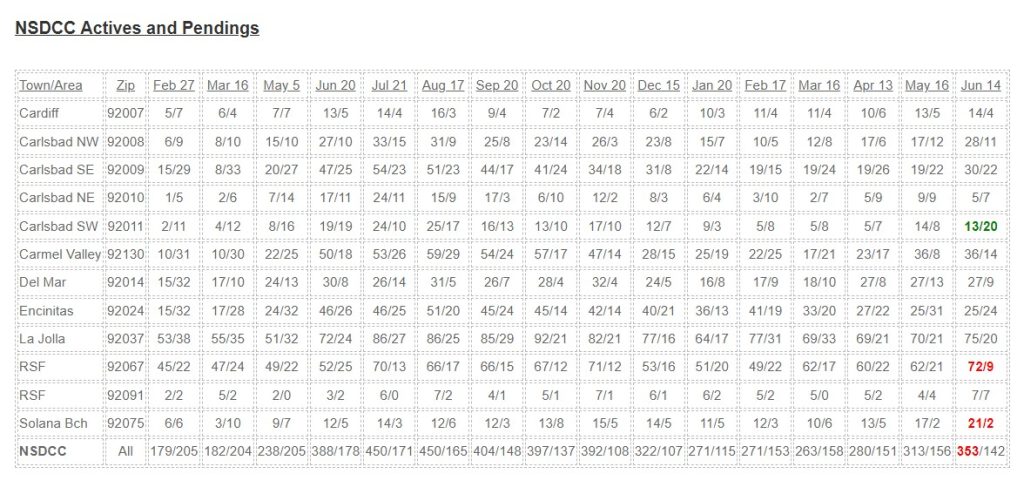

The number of active (unsold) listings has been on the rise, and is now 13% higher than it was a month ago – though I would still characterize the current market conditions as steady.

Compare your stats from this month to last June and July when higher rates had begun to take their toll. The rate-change was rather abrupt, and it was natural for buyers to wait-and-see about the impact which caused the active inventory to soar.

If your area looks similar to last June/July, it’s probably not a good thing.

The activity this year is more normal and typically what happens as the selling season closes out – sellers are too enthusiastic after a couple of hot months and don’t adjust their price expectations fast enough.

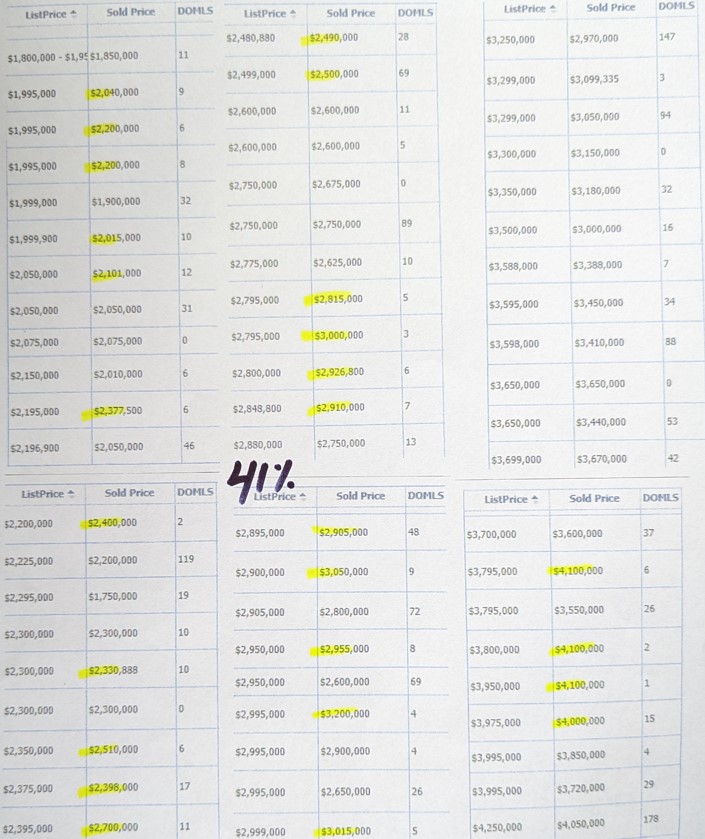

There have been 57 closings between La Jolla and Carlsbad this month, which is good. The monthly sales total should finish over 100, but it probably won’t get up to the 168 sales we had in May.

There will be a few more eye-popping sales, but generally the 2023 market is fading away.

Here are expert opinions on the market. I disagree with all of them:

The year started out with signs showing that the Federal Reserve’s inflation-fighting tactic was effective in cooling down the hot pandemic housing market.

For the first time in 11 years, home prices dropped year-over-year in February as mortgage rates more than doubled following the Fed’s consecutive interest rate hikes, curbing affordability.

However, the median price of a home increased month-over-month for the second consecutive month in March. The median home price is projected to increase for a third month in a row in April to $393,300, which is 2% lower than the previous April’s median price of $401,700, according to data released in May by the National Association of Realtors (NAR).

One big factor behind the strengthening home prices and the decrease in sales volume — down 23% in April from a year ago — is the lack of housing inventory.

“Home sales are bouncing back and forth but remain above recent cyclical lows,” says NAR Chief Economist Lawrence Yun. “The combination of job gains, limited inventory and fluctuating mortgage rates over the last several months have created an environment of push-pull housing demand.”

Where are home prices headed?

Generally speaking, high mortgage rates should prompt house prices to trend downward.

“Yet, housing supply remains so restricted, that any uptick in demand will put upward pressure on prices,” wrote First American Chief economist Mark Fleming in a blogpost. “This is the dynamic that played out in March, as the spring home-buying season ushered in more demand for homes, while insufficient supply prompted buyers to compete and bid up prices.”

No return to typical seasonality in the market

There will be a lot of uncertainty in the economy over the next few months and prospective home buyers are going to be more opportunistic, as opposed to following traditional seasonal market trends, says Bright MLS Chief Economist, Lisa Sturtevant.

“There will continue to be volatility in mortgage rates as we wait to see what the Fed will do at its upcoming meetings and as we watch economic data roll in over the summer,” says Sturtevant. “Prospective buyers are going to be watching rates closely, and many will try to make an offer on a home when they see rates dip. As a result, we should expect less seasonality this year than we had prior to the pandemic.”

More sellers returning to the market

While inventory will remain low this year, we should expect to see more sellers who had been on the sidelines list their home for sale this summer and into the fall, says Sturtevant.

Many existing homeowners have been “locked in” with super low mortgage rates, which has discouraged discretionary moves.

“However, some people have to move, and others will decide to move for a bigger or smaller home, or to change jobs or neighborhoods, despite rates remaining elevated,” says Sturtevant.

The uptick in new home construction has provided more opportunities for move-up buyers who may have been staying in place because they did not have anywhere to move to.

“One thing that could shut down new listings is if we see a sharp spike in mortgage rates to 8 or 9%, a situation that is still unlikely but not out of the realm of possibilities,” she says.

New home construction

Instability of regional banks is a concern for builder and land developer financing going forward, says Robert Dietz, chief economist for the National Association of Home Builders.

Lending conditions for builders have tightened, and the interest rate for development and construction loans is now well above 10%, which threatens housing supply.

Single-family spec home building loans had an effective rate of 13% in the first quarter of 2023 compared to 9% in the first quarter of 2018.

“Our expectation is that the rate of these loans will move lower as the Fed cuts the federal funds rate, but our forecast is that will not happen until later in 2024,” Dietz told USA TODAY. “As a result, land development would be suppressed, and we risk loaning low on lots during a home building rebound in 2024. Lot development can take three years in a typical market.”

The experts are saying that real estate has recovered and everything will be fine now, in spite of high rates. They are quick to add that nobody can predict the future!

Well, it looks fairly predictable to me.

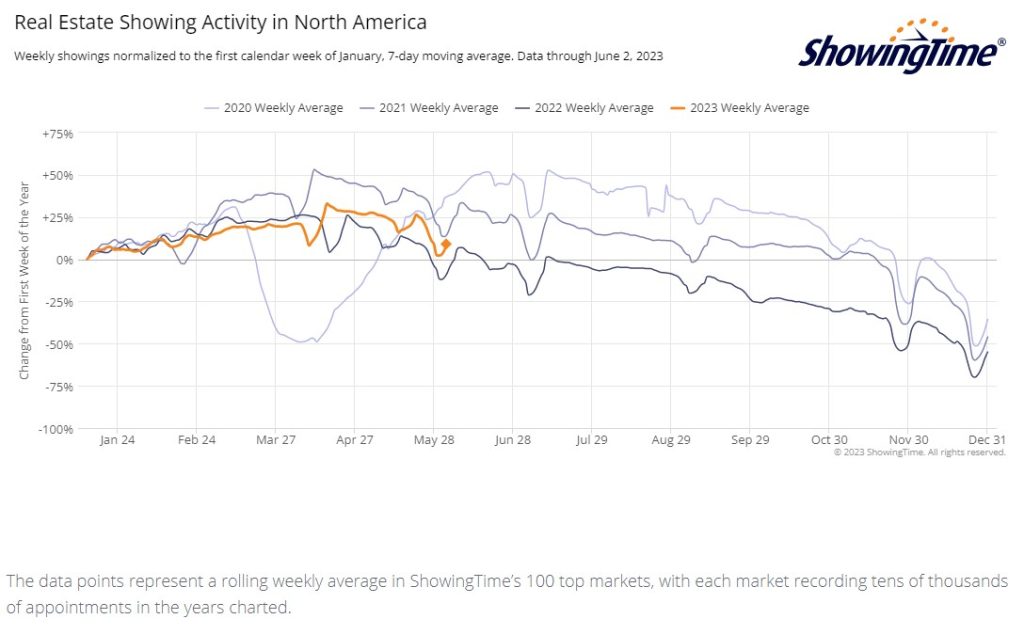

The previous three years plotted above were the hottest frenzy markets of all-time, so we’re lucky just to be having a similar run of showings. But today those showings will be less fruitful, and even if the 2023 trend can stay close, we probably won’t be having as many actual sales.

If the rest of this year goes about the same as recently, we should have a couple of strong weeks in June, take off July 4th, and then a couple of decent weeks in July before drifting off for the rest of the year.

Mortgage rates would have to get into the 5s for it to go any better.