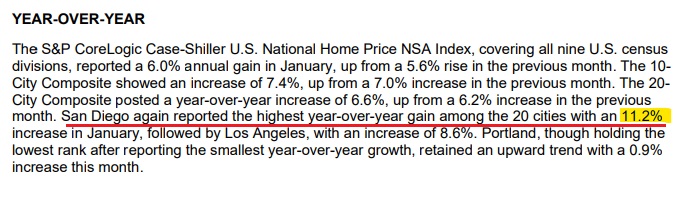

San Diego Case-Shiller Index, Non-Seasonally Adjusted

Month

SD CSI

M-o-M chg

Y-o-Y chg

Jan 22

384.13

+2.5%

+27.2%

Feb

401.44

+4.6%

+28.9%

Mar

416.45

+3.8%

+29.9%

Apr

425.90

+2.3%

+28.5%

May

427.80

+0.5%

+25.2%

Jun

424.83

-0.7%

+21.6%

Jul

414.03

-2.6%

+16.5%

Aug

402.48

-2.8%

+12.7%

Sep

393.80

-2.1%

+9.5%

Oct

390.61

-0.7%

+7.6%

Nov

385.40

-1.5%

+4.9%

Dec

380.09

-1.3%

+1.6%

Jan 23

378.79

-0.4%

-1.3%

Feb

384.46

+1.6%

-4.1%

Mar

394.05

+2.5%

-5.3%

Apr

401.90

+2.0%

-5.7%

May

409.32

+1.9%

-4.3%

Jun

413.72

+1.1%

-2.3%

Jul

416.68

+0.7%

+0.6%

Aug

419.08

+0.5%

+4.1%

Sep

419.35

+0.0%

+6.4%

Oct

418.82

-0.1%

+7.2%

Nov

416.36

-0.6%

+8.0%

Dec

413.45

-0.7%

+8.8%

Jan 24

421.34

+1.9%

+11.2%

It has felt like prices have been surging this year, and here is more evidence. The record high was 427.80 in May, 2022, and it should be back to that level by the next reading.

We’re in the midst of all-time record-high pricing today!

My only thought when seeing thas property was whether Kellen Winslow Jr would affect the outcome or if whether we are beyond that now. He bought his new for $2,871,000 in 2015 and had to cheap sell it for $2,850,000 in 2019 when he got into trouble.

But even his house resold for $4,800,000 last year, so no lingering after effects, apparently.

Oh, you’re going to get lower commissions alright – on the backs of the buyer-agents.

The last time I checked a couple of months ago, there were 30% of the monthly closed sales that offered a buyer-agent commisssion under 2.5 percent. Of the 92 closings so far this month, 25% of them were under 2.5% – and those were determined before the NAR debacle.

The listing agent determines how much the buyer-agent gets paid.

Not the seller, not NAR, not the attorneys – it is the listing agent who decides the commission rate to offer the buyer-agents. It makes for an easy solution. Want a lower overall commission rate? Just take it off the amount paid to the buyer-agent. What’s worse is the MLS rule that buyer-agents are not allowed to negotiate the rate – hopefully that will go away now.

Listing agents aren’t lowering their commission rate – they are taking the same or more than ever, and paying less to the buyer-agents. They are under-appreciating the amount of work it takes to conclude a successful buyer-side transaction (usually 3-6 months of frustration and losing).

If the listing agent has superior skills that result in a higher sales price and a smooth transaction, then no one will mind them getting paid accordingly, but their success is also at least partially due to the buyer-agent doing his job well. The good buyer-agents shouldn’t be penalized, and ideally, there would be a sliding scale based on performance.

But because everyone will be hearing that commissions are negotiable (for the first time, says Biden), the listing agents who feel the need to agree to a lower rate with their sellers will just subtract the same discount from the buyer-agent side. But is that in the best interest of the seller?

This practice will expedite the demise of the buyer-agent.

The reporting on the NAR settlement seems to be focused on creating hysteria, rather than finding the truth. Realtors commissions have always been a juicy topic, and the media is intent on using this opportunity to fabricate wild and salacious stories to attract the maximum number of eyeballs.

The hysteria may just be beginning, however. The NAR settlement included penalties for every brokerage that sells more than $2 billion in volume per year. For Compass, the top brokerage in the country for total volume, it means imposing a fine of $500 million without consulting with Compass management, let alone negotiating. The NAR doesn’t have the authority to speak for us, or commit us to any penalty so who knows what they were thinking but it guarantees the end of NAR – why would any brokerage want to be associated with such bums?

Those fines will get litigated and drawn out for years. The requirement to remove the commission rate in the MLS will start in July, but listing agents can advertise the amount of buyer-agent commission everywhere else. We will hear more about the buyer-agent commission than ever before – and steering done by both buyer-agents and buyers themselves. Buyers will prefer the listings that pay more commission, so they pay less. So much for fixing the concerns about steering!

As realtor-panic goes, the beginning of Covid was much worse – we didn’t think we’d sell a house for months! Those who panic about this hiccup are the realtors who don’t have much to offer – those who aren’t real salespeople. Nobody will mind seeing them either get better, or get out of the business.

But houses will keep selling at a brisk pace regardless of commissions.

This will blow over in a few months.

My previous post mentioned the need for getting good help. Getting cheap help will probably be tempting until people get a feel for the difficulty of what it’s like:

We made a clean, full-price offer. Three days later, still no answer.

We made an offer on a Friday that was $50,000 under list on a 2-br house in original condition. The sellers decided to take their chances with open houses (in search of two in the bush) over the weekend, instead of responding. We attend, and the listing agent isn’t doing the open house; there is a trainee there instead. We look harder to find something better, and succeed. By Monday, the listing agent wants to re-engage, and by Wednesday she begs me to get back in the game. They receive another offer, but it’s $100,000 under list. We moved on.

I’ve had several solid buyers attend open houses in the last year – people I’ve talked to who sure gave me the feeling that they liked the home so much that they were going to make an offer. But then when I follow up with their agents – who usually don’t accompany – they can’t close the deal. It makes me want to sell my listing to their buyer and just send them a check in the mail.

Multiple offers – what do you do? I lost another one where we offered the exact same price ($100,000 over list), and the listing agent seller picked the one with the bigger down payment, instead of letting the buyers decide it. Don’t you think there might be some gas left in the tank? Like $25,000 to $50,000?

You get an offer while off-market. Then what?

When does a seller lower their price? Or not?

Buyers and sellers typically have little experience in fixing things – especially the big stuff – and agents aren’t much better. So instead, a proper discount is attempted, but sellers always think in pennies, and buyers think in thousands. With little or no buyer representation, how are those going to get handled? They’re not, and more deals will die. This is a problem on virtually every sale.

Inexperienced people tend to over-react, and any bump in the road could be a deal-killer.

How much should buyers offer? Most agents respond with, “Well, that’s up to you”.

What is the real value of the property? Once a home is on the open market, Zillow and Redfin adjust their estimates to within a buck or two of the list price, so sellers, buyers, and agents must each determine the value themselves. How good are they at determining the value? How much variance is acceptable? Virtually nobody knows, and unless there is a good agent involved, more deals that are 1% to 2% apart will die an unnecessary death.

How do you know when you’re talking to the wrong agent?

Their only line is “Let me know if you have any questions”.

Good salespeople ask the questions, and then offer opinions and advice!

The commission lawsuits are the best thing to ever happen for my slogan! Get Good Help!

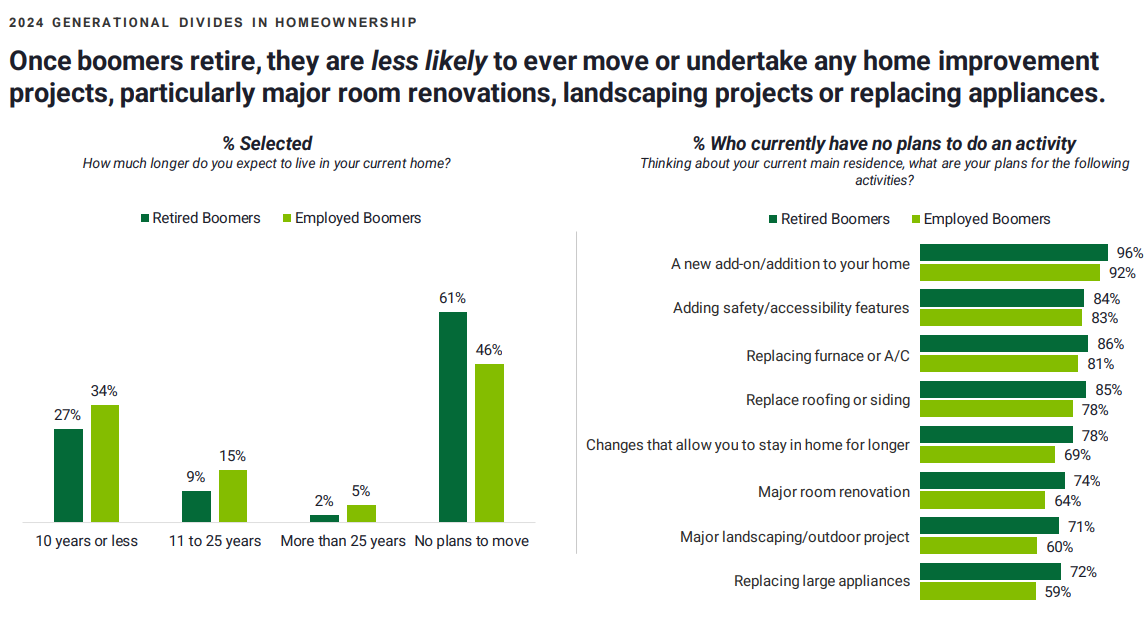

As the boomer estate sales become the dominant source of homes for sale, their buyers can expect to do some work. In most cases, there will be a lot to do!

It’s been obvious that the entire real-estate-selling business has been deteriorating towards single agency. I see it every day on the street, and I’ve posted evidence of the shift regularly.

The trend is moving quickly now on multiple fronts.

The DOJ is going to decouple commissions, which will prohibit sellers from offering to pay the buyer’s agent. The buyers can include it in their offer, but it likely won’t get that far. The buyer-agents who are left will want a written agreement to get paid by the buyer if the seller won’t pay. How many agents will be able to demonstrate why they are worth it? Not many, but maybe the buyers won’t ask too many questions.

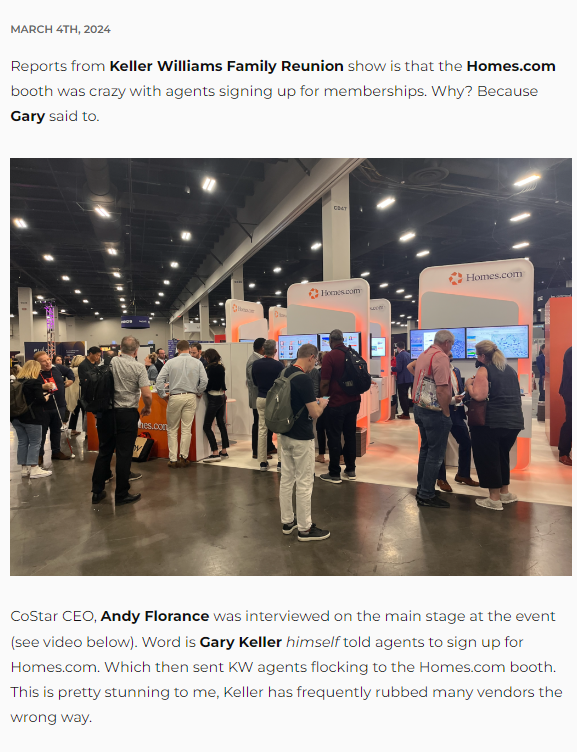

Homes.com is spending millions and billions on advertising their website to compete with Zillow. Their twist? They funnel all the leads back to the listing agent, instead of farming them out to the highest bidders like Zillow does. I’ve been called by several phone jockeys from Homes.com to sign up for their enhanced listing packages, and I’ll sign up. Robert Reffkin responded positively to the Homes.com program, and you can see how Gary Keller feels about it above.

Agents are giving up on representing buyers because it’s too hard and doesn’t pay enough. Most of the unsold listings are grossly over-priced and the occasional deal gets multiple offers within minutes. Agents have to spend months or years working with their buyers before they get lucky, only to then get a reduced commission from the listing agent. Now I have to convince the buyer to pay the commission too? Great, thanks.

Listing agents are advertising for buyers to avoid paying the buyer’s-agent commission by coming directly to the listing agent instead. Realtor cannibalization is what we deserve. (link)

This house priced at $1,985,000 in Rancho Penasquitos received 15 offers and likely sold for 15% to 20% over list (an offer that was 12% over with free rentback wasn’t enough).

I remember when $2,000,000 got you a decent house in Carlsbad!

It looks like the over-heated housing market will cause the government to do something so it looks like they care. There was a $8,000 first-time homebuyer credit back in 2009-2010 that was free money given to those who just happened to buy a house then – nobody bought a house just because of the credit. The same will happen now – it will just be free cheese for those buyers and sellers in the right place, at the right time.

How the two credits would work, according to the White House:

“Middle-class” first-time homebuyers would get an annual tax credit of $5,000 a year for two years. The White House didn’t specify what “middle class” means.

A one-year tax credit of up to $10,000 to “middle-class families who sell their starter home, defined as homes below the area median home price in the county, to another owner-occupant.”

President Biden is calling on Congress to pass a mortgage relief credit that would provide middle-class first-time homebuyers with an annual tax credit of $5,000 a year for two years. This is the equivalent of reducing the mortgage rate by more than 1.5 percentage points for two years on the median home, and will help more than 3.5 million middle-class families purchase their first home over the next two years.

To qualify, home buyers must meet the following eligibility standards:

Must not have owned a home in the last three years.

Must not be a prior recipient of a first-time home buyer tax credit.

Must not earn more than 60% above than the area’s median income.

Must be making an arms-length transaction.

Must be at least 18 years old.

The President’s plan also calls for a new credit to unlock inventory of affordable starter homes, while helping middle-class families move up the housing ladder and empty nesters right size. Many homeowners have lower rates on their mortgages than current rates. This “lock-in” effect makes homeowners more reluctant to sell and give up that low rate, even in circumstances where their current homes no longer fit their household needs.

The President is calling on Congress to provide a one-year tax credit of up to $10,000 to middle-class families who sell their starter home, defined as homes below the area median home price in the county, to another owner-occupant. This proposal is estimated to help nearly 3 million families.

To qualify for the $10,000 Home Seller Tax Credit, sellers must meet the following eligibility requirements:

The home seller must live in the home they’re selling as their primary residence.

The home buyer must make the home their primary residence.

The home buyer must not earn more than 60% above the area median income.

Additionally, the home for sale must be a starter home which is defined as a home that sells for less than the county’s median home price. Eligible property types include single-family homes, condominiums, townhomes, multi-unit homes, and any other home zoned for residential residence.

The bill will increase available housing inventory for homes selling between $100,000-250,000 which, according to the National Association of REALTORS® Existing Home Sales report, is the fastest-selling segment of U.S. homes.

To take effect, these proposals would require Congressional approval. As of today, neither Democratic nor Republican leadership in the House or Senate has come out to support the measure.

President Biden also called on Congress to pass the Downpayment Toward Equity Act, a downpayment assistance program for first-generation home buyers that gives up to $25,000 in cash grants. The bill was originally introduced in the 2021-2022 Congress, then re-introduced in 2023. It has 44 co-sponsors in the House of Representatives. A corresponding bill is expected to be introduced in the Senate soon.

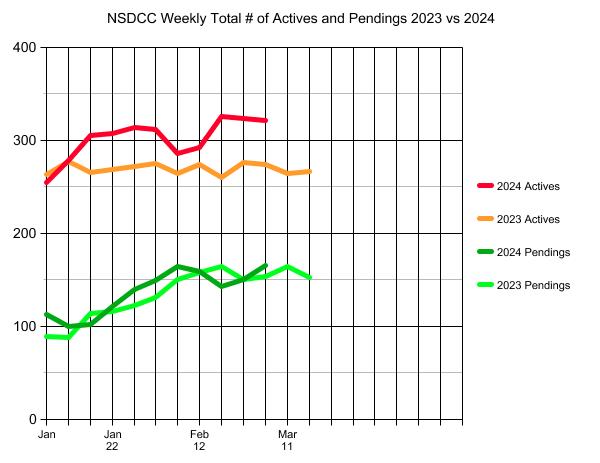

There have been 12% more listings YoY in the first two months of 2024, and buyers are responding!

Closed SFR sales between La Jolla and Carlsbad are +20% YoY in the first two months of the year!

It’s why the number of active listings (red line above) isn’t exploding, AND there have been 88 new pendings in the last two weeks – which is about twice the pace we had in January. The median LP of those 88 pendings is $2.5 million, which means pricing will be at least +10% higher than last year. Wow!

There had to be skeptics to my Los Altos Adventure last weekend.

Did you mis-price the houseby more than a million dollars on purpose – or just by accident? Come on – you were 440 miles out of your normal market area….dude….you got lucky!!

I like to pay close attention to the market activity in the days before inputting a new listing. This was the latest listing by the guy who has just captured nationwide attention of his lowball $10,000-commission offer to the buyer-agents. As of Wednesday night, this was still active, and I told my sister that I didn’t want to compete directly because mine would help to sell his. If it was still an active listing when I woke up on Thursday, then I’m not coming up and we will postpone the listing for at least two weeks due to weather:

Miraculously, when I woke up the listing was marked pending – so I left for Los Altos.

All I had to be was the most attractive new listing in a very exclusive area (Nvidia is based in San Jose). There had to be losers from the Parma bidding war who were motivated to buy the next one, and there was nothing else for sale at this price point.

I was talking it up with every agent who came to my open house, and eventually I found an agent who was in the same office as the buyer-agent of Parma – and they confirmed that it sold for $4,150,000! Do you think I told that to every person I met over the next 48 hours….yes!

Let’s note my options: Either price attractively and have buyers bid it up, or price at retail and wait.

Here’s an example. The size of house and lot are pretty similar to mine, and it’s a busy street too. How are they doing? They listed for $3,998,000, and 30 days later they are still unsold:

The more obstacles that need to be overcome, the more attractive the price needs to be.

I’ve been showing houses to buyers the last couple of days, and this theory has never been more clear. As we walk into a house that appears to be priced at the top of the range (or higher), the skepticism builds with every step – and we’re looking for any reason NOT to buy.

But when you walk into an attractively-priced home and see defects, they just confirm why the price is attractive – buyers don’t expect perfection when the price is attractive!

What happens once a home hits the open market depends on the listing agent. Yesterday, one was blaring his Jesus music, and another was chatting with the sellers who were still hanging around even though the open house started 15 minutes earier. Most listing agents aren’t implementing any bidding-war strategy – heck, yesterday there was one agent who didn’t even know the price of the home!

In reviewing the Los Altos comps, about half of them had closed over the list price, so I knew it was going to be hot. I knew that I was selling a house that looked all original, and was on a busy street. So we priced it attractively and I aggressively implemented my tried-and-true bidding war strategy that works!

We can expect that the election season will be like no other in the history of the USA!

Prepare accordingly!

Can you imagine how this will play out? If Biden wins, there will be a civil war. If Trump wins, he’s promised that there will be full chaos on Day One. We can write off the 4Q24, and maybe more!