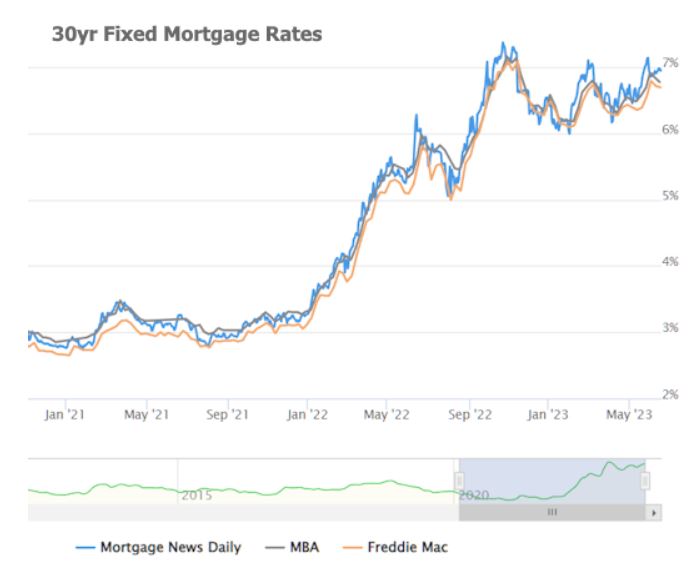

The average 30yr fixed quote for a top tier scenario was around 6.75% on Friday and was up to 6.87% by Tuesday afternoon. More than a few lenders are already back to 7%.

https://www.mortgagenewsdaily.com/markets/mortgage-rates-02212023

My thoughts below on how this year should wrap up. Buyers don’t have any reason to rush anything because rates and prices don’t seem to be going anywhere over the next few months. It will cause them to be extra picky which will tempt everyone to look ahead to the next selling season. We’re going to the game tonight with Natalie and Ryan – go Padres!

Let’s pay attention to current events:

There has been plenty of buffer built into mortgage rates lately, so more declines are possible. But a hot CPI tomorrow will give mortgage lenders a great reason to raise their rates in advance of the Fed meeting next week.

From MND:

Speaking of big things, the bigger question is “what’s next?”

What indeed! There are more questions than answers right now. Some say the bank failures are evidence that the Fed’s tough interest rate policies have “broken something,” and they must now dial back their intensity.

Others say the Fed knew some things would “break” and that they’ll only dial back if lower inflation says they can. To that, others say that inflation is even more likely to move down now that people are worried about the banking system and a recession.

And to that I say we just don’t know yet. All we do know is that these bank failures are very different than those seen before the financial crisis in several important ways. We also know the Fed/FDIC/Treasury stepped in with a non-taxpayer-funded plan to calm the market, and it seems to generally be working today.

If the market is calmer, then why are rates still so much lower? This has to do with the market shifting its expectations for Fed rate hikes in the rest of 2023. Specifically, the market now sees the Fed hitting a ceiling rate that’s more than 1.5% lower than it was at the beginning of last week!

If that continues to be the case in the coming days, mortgage rates could move down even more. We’ll learn more about those odds at two key moments: tomorrow morning at 8:30am Eastern Time when we get the next major inflation report, and then next Wednesday afternoon when the Fed releases its latest policy announcement.

https://www.mortgagenewsdaily.com/markets/mortgage-rates-03132023

Last year the NSDCC sales were the lowest on record. We were already thinking that if the 2023 sales could get to 80% of that number, it would be great. But if mortgage rates spend the next ten months over 7%, what will be the annual sales count for this year? Maybe 50% – 60% of last year?

On November 9th, 2022, the average lender was quoting 30yr fixed rates well over 7%. On day later, that figure dropped to 6.625%. It was one of the best individual days for rates on record and it was driven by an economic report that showed an unexpectedly large drop in inflation.

Inflation and several other key sectors of the economy had pushed the Federal Reserve to hike rates at the fastest pace in decades. When it looked like the data might provide some relief, rates quickly moderated.

Strangely (or so it seemed at the time), the Fed was highly reluctant to read too much into several months of generally more palatable data. They said it was too soon to draw any conclusions other than “it’s a start.” With that, markets hesitated to push longer term rates any lower until the data made an even stronger case of that.

Unfortunately, the data since then has made a case for rates to turn around and head right back up toward previous highs. February has been particularly brutal in that regard and today was just the latest example. In fact, today’s reports aren’t typically regarded as top tier motivations for rate movement, but the market is so defensive to begin with that it doesn’t take much of a bump to create a snowball of momentum.

The average 30yr fixed quote for a top tier scenario was around 6.75% on Friday and was up to 6.87% by Tuesday afternoon. More than a few lenders are already back to 7%.

https://www.mortgagenewsdaily.com/markets/mortgage-rates-02212023

The mortgage rates are heading for 7% again, which is shocking, given it was 5.99% on Feb. 2nd.

Higher rates will discourage both buyers and sellers, and make them want to wait for a “better market” some day in the future. Whether that day will come isn’t considered – all they know is that it isn’t today.

It should mean that the market will be cleared of any casualness, and only the highly motivated buyers and sellers will be engaging. Buyers will be more picky, and sellers will need to be sharp on price.

How sharp?

It will be different in each neighborhood, but I’ll give you one example.

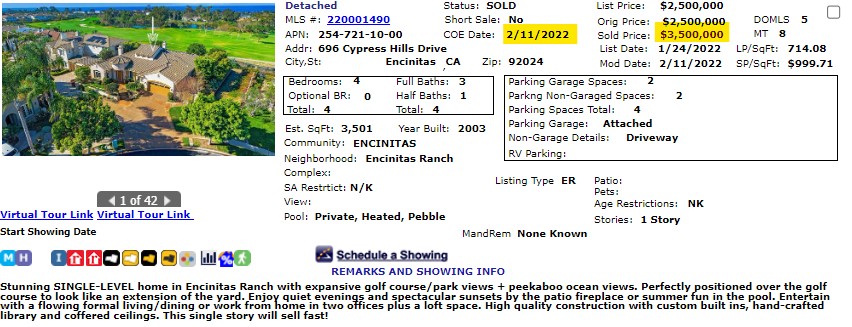

After I set the market on fire in Encinitas Ranch at the end of 2021, this one-story house went for sale. It got bid up a million over the list price (which was deliberately set low by the seller), and the buyer paid cash:

I think the buyer passed away, unfortunately, and the house is coming back on the market.

Today’s list price, just a year after purchase? $2,900,000.

It is possible that 2023 is going to be as good as it gets for sellers – at least for the next few years. The Fed is adamant about crushing the economy, and we could see mortgage rates well into the 7s and, dare I say, we might be pushing 8% mortgages by summer.

The number of sales will be lower than ever, which means more volatility. It will be wild and crazy for some, and that might be entertaining for the casual participants but it won’t draw them off the sidelines.

The higher the mortgage rates go, the less volume there will be and some markets could freeze up.

And this could be as good as it gets for a while – yippee!

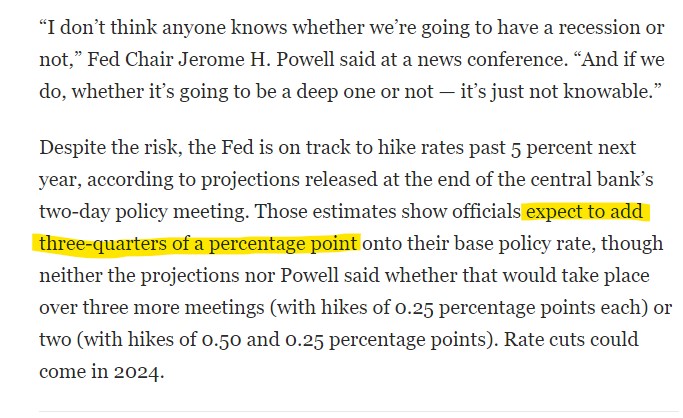

It’s bad enough that the Fed chairman doesn’t know how his actions will affect the markets. If you didn’t know, wouldn’t you be cautious?

Apparently not for Powell, and it seems likely that the Fed will bump their Fed Funds rate another 3/4% in the first half of 2023 – and maybe do all of it in the first quarter (there are two Fed meetings in 1Q23).

The mortgage companies have to be scrambling with the drastically-reduced volume of loans, so hopefully some of it is already priced in, for their sake. Financed sales are probably down 50% and there aren’t many homeowners wanting to refinance at these higher rates, so lenders will be forced to squeeze their margins just to stay in business.

If they can keep jumbo rates in the 5s, I think we’ll be ok next year.

But we can’t expect to absorb another 3/4% hike by the Fed and not see it affect mortgage rates. It means that today’s rates might be the lowest we see until a few months into the Fed-induced recession….if it happens. If the recession doesn’t happen or is mild, then we’ll be stuck with those higher rates – and if they hike by 3/4% and just let it ride, today’s rates could be the lowest we see in the next 2-4 years.

Yet they will be wasted because there is nothing to buy – sellers will hold off until the coast is clear.

Powell can’t envision this scenario, even though it should be obvious. When you publicly state that you are trying to reset the the real estate market, potential sellers are going to wait until later to sell.

Will Congress think about revisiting the 2 out of 5 year exemption, passed in 1997? They should, because that’s what could flood the market with inventory. If you want a reset, you need to do things to INCREASE the supply, not tighten it.

Rant over, thanks for listening.

This is how close we are to a market resurgence. If sellers would pay down 4% to 6% of the loan amount to lower the buyer’s mortgage rate by another 1% to 1.5% and get it into the 4s, we’d be looking good for springtime.

From JB:

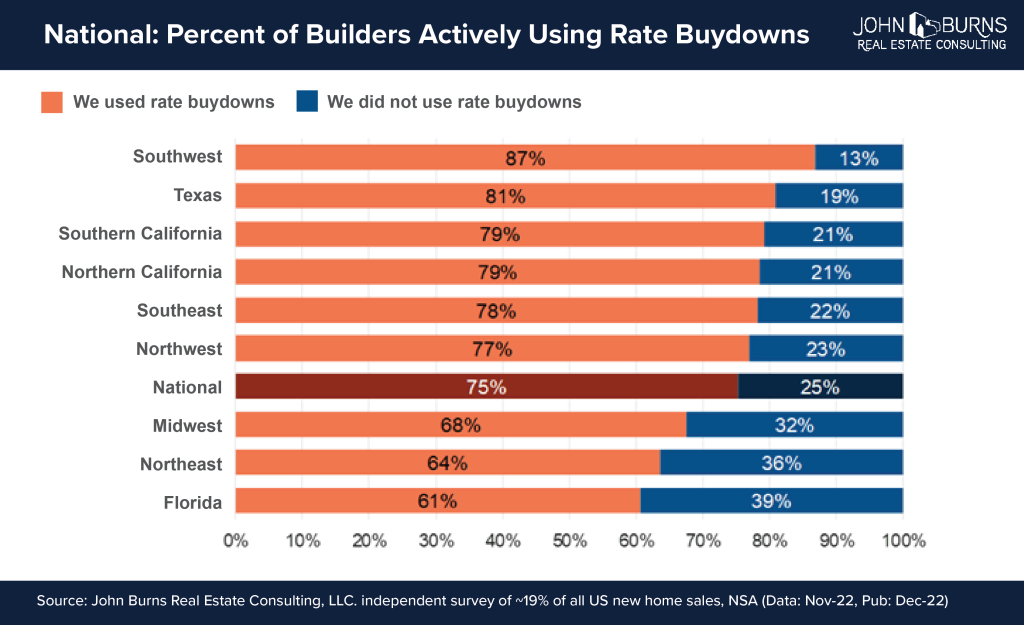

In early December, 75% of nationally surveyed home builders confirmed they are buying down buyers’ mortgage rates to make payments more affordable.

Our survey indicates 32% of builders are buying down the full 30-year term and another 30% of builders are temporarily reducing the rate for the first two years of the mortgage. The remaining 13% of builders identified other less common buydowns. Builders pay these costs up front, effectively reducing monthly payments by prepaying for some of the buyers’ interest on the loan. Few resale sellers are offering these savings to prospective buyers.

Two popular strategies involve builders lowering the mortgage rate for the buyer:

30-year rate buydown: Builders are contributing 5%–6% of the home purchase price up front to lower the 30-year mortgage rate by 1%–2% typically. For example, builders may reduce the rate from 6.5% to 5.0% using last week’s Freddie Mac mortgage rate.

2-1 temporary rate buydown: Builders are contributing 2% of the home purchase price up front, which lowers the first-year mortgage rate by 2%, and the second-year mortgage rate by 1%. Using last week’s 6.5% rate, a buyer’s rate would be 4.5% in year one, 5.5% in year two, and 6.5% thereafter. Borrowers still have to qualify at the 6.5% rate to benefit from a reduced payment in the first few years, giving them some breathing room to perhaps spend money on furniture or other needed items.

Because buyers have to qualify at the highest rate that will occur during the 30-year term, builders using the 2-1 temporary buydown tell us some buyers still cannot qualify. By shifting to a 30-year rate buydown, builders can lower the rate and monthly payment used to qualify struggling buyers.

Read the full article with more calculations here:

https://www.realestateconsulting.com/the-light-rate-buydowns-help-buyers-purchase-new-homes/

This isn’t exactly new news – most prognosticators figured the Fed would only raise their rate by 0.5% in December, instead of the 3/4% hikes recently – but the stock market liked it (up 628) and the 10-year yield dropped a tenth. All we need is mortgage rates to be in the 5s for selling season!

Monetary policy affects the economy and inflation with uncertain lags, and the full effects of our rapid tightening so far are yet to be felt. Thus, it makes sense to moderate the pace of our rate increases as we approach the level of restraint that will be sufficient to bring inflation down. The time for moderating the pace of rate increases may come as soon as the December meeting. Given our progress in tightening policy, the timing of that moderation is far less significant than the questions of how much further we will need to raise rates to control inflation, and the length of time it will be necessary to hold policy at a restrictive level. It is likely that restoring price stability will require holding policy at a restrictive level for some time. History cautions strongly against prematurely loosening policy. We will stay the course until the job is done.

He never had a clue about the real estate market, and was just winging it – and nobody has helped him with it since. “…..hopefully come out in a better place between supply and demand”??? The guy who has our economy in his hands is living on hope?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Will the 30-yr jumbo rate stay in the 5s? Here’s what MND says:

Excitement, volatility, non-stop action… concepts that have absolutely nothing to do with mortgage rate movement over the course of the past two weeks. In fact, since rates plummeted in response to the November 10th CPI data, they’ve been as flat as we’ve seen in 2022.

This is the goal for financial markets and mortgage rates as they traverse a time frame like the Thanksgiving holiday, but it’s also a byproduct of relevant events. Specifically, inflation data dominates the landscape. It was no surprised to see a big reaction to the CPI data 2.5 weeks ago, and markets may largely be waiting for the next installment before the next substantial shift in rates.

This doesn’t mean rates will remain as flat as they have been–only that they may resist moving too far in either direction until they have more guidance from economic data and the Fed. This week will bring some of that economic data, but the next CPI report arrives on December 13th followed a day later by the next Fed announcement.

Fed speakers were making the rounds today reminding markets that there are more rate hikes to come. The Fed sees the strength of the jobs market as providing a cushion to be aggressive in its fight against inflation.

While the Fed will almost certainly continue to hike rates on the 14th (probably by 0.50%), financial markets have long since baked that assumption into current trading levels. That means today’s mortgage rates already account for the current Fed Funds Rate forecasts.

Even then, the Fed Funds Rate doesn’t dictate mortgage rates and is an imperfect indicator for rate momentum. Longer term rates like mortgages and 10yr Treasury yields typically begin falling sooner and by larger amounts in any given rate cycle. The past few weeks could be the first phase of that typical pattern (10yr Treasuries have dropped 0.30% versus 2yr Treasuries since then), but again, the continuation of that pattern depends on confirmation from upcoming inflation data.

https://www.mortgagenewsdaily.com/markets/mortgage-rates-11282022

Today’s rates with no points

The Spring Selling Season could get a real boost if mortgage rates stay in the 5s.

The Fed has been telegraphing their intentions for months now, and at this point, there can’t be anyone who thinks the Fed won’t keep raising their Fed Funds rate – at least for their next two meetings. Mortgage lenders have to be pricing in the anticipated future increases, yes?

After some tepid inflation news last week, mortgage rates came down a 1/2%, and they have stayed there, which makes me think that there was already too much buffer priced in – and there has to be some extra left knowing that the Fed has more work to do.

But just in case, go out and buy a house today so you can get a 5-something rate!

Checking-in on the Buffalo snowstorm:

“But that’s my own fault.”? https://t.co/g7zWZg8GXM

— Rex Chapman?? (@RexChapman) November 21, 2022

Are you looking for an experienced agent to help you buy or sell a home?

Contact Jim the Realtor!

CA DRE #01527365, CA DRE #00873197