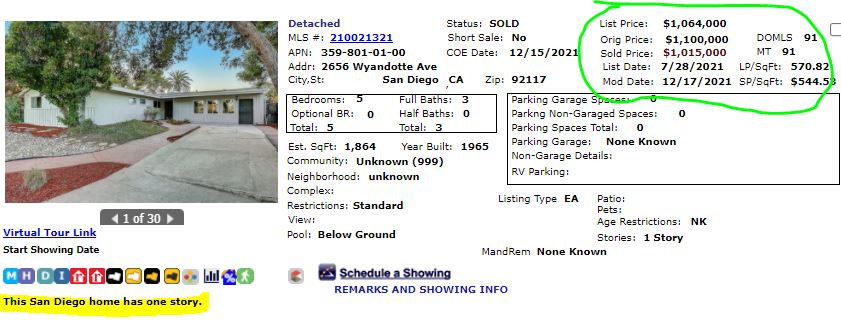

Because Opendoor listed this home for $1,100,000 right after they bought it for $1,081,000 (and did no improvements), it must have meant that they thought they stole it. The market thought otherwise, and some might think they were lucky to get what they did.

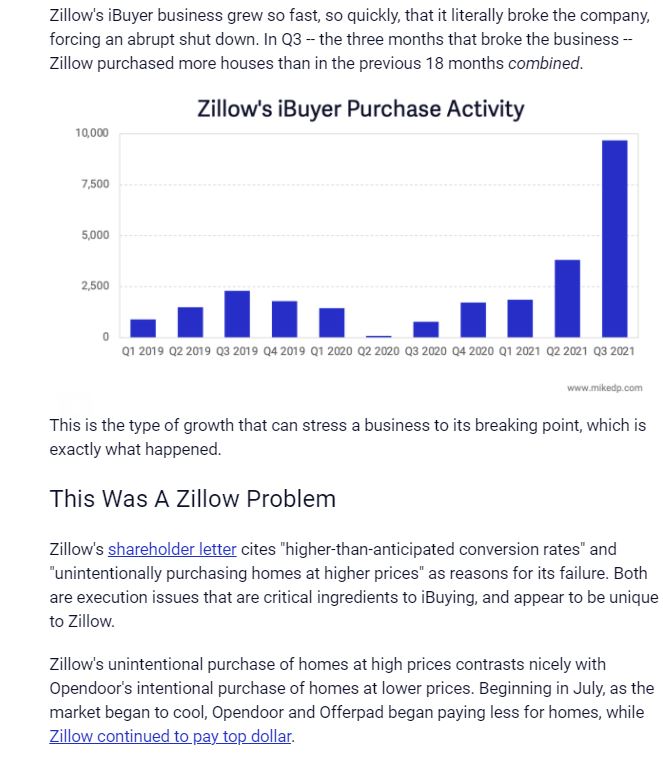

Mike pointed out that Zillow simply kept paying too much for homes, and instead of adjusting on purchase prices being offered, they shut it down yesterday.

But Zillow is too big and too aggressive to rest.

Here’s what Mike thinks could be next:

While Zillow 2.0 may have been a failed experiment in iBuying, what captures the imagination is the next iteration of the business. How will Zillow leverage its massive competitive advantage and its iBuyer learnings for Zillow 3.0?

I wouldn’t be surprised to see Zillow play deeper in the Power Buyer space, a model that is asset-light, easier to scale, less risky with better unit economics, and has a natural overlap with Zillow Home Loans (Opendoor diversified into Power Buying earlier this year).

Zillow as a Power Buyer — either through organic development, partnership, or acquisition — is a natural extension to its existing business of helping home buyers. The world of real estate has evolved significantly since 2018, and Zillow needs to stay relevant to those evolving consumer needs.

It would be a smart move. The buyer side is where the help is needed.

Assisting buyers with making all-cash offers is a very attractive service, with no real downside because all they have to do is funnel the business into their mortgage company to refinance the purchases after the fact. They could flip these buyers to their Premier Agents too – a group who is wondering if it’s worth it to be a Zillow customer today.

The supply and demand will be out of balance for years to come, and buyers are the ones that really need the help. Go Zillow!

The ibuyers are borrowing money like crazy to build their inventory of homes to flip. Opendoor doesn’t have the brand-name awareness of Zillow, so they are advertising a lot and buying homes directly off the MLS. Zillow has everyone’s email address so they are able to reach their users directly. Both have been fairly well-compensated during the 12-month frenzy – will it continue? From this article:

Opendoor Technologies Inc., which buys homes from consumers and lists them for resale, is in talks with lenders for a new revolving credit facility of roughly $2 billion, according to people familiar with the effort.

The company, which is rapidly accelerating the number of homes it purchases, plans to use the proceeds to help increase acquisitions, said one of the people, who asked not to be named because the matter is private.

A representative for Opendoor declined to comment.

Opendoor, led by Chief Executive Officer Eric Wu, pioneered a data-driven spin on home-flipping known as iBuying. After the company buys a home, it makes light repairs and seeks to resell it, profiting by charging sellers a 5% fee for the convenience of an easy sale.

The company acquired 8,500 homes in the second quarter, more than double the number it bought in the first three months of the year, according to an statement Wednesday. It also had roughly 8,100 additional houses under contract at the end of June.

Opendoor uses debt to fund acquisitions, and had just under $4 billion in borrowing capacity under existing revolving credit facilities as of the end of June. The company had drawn $1.8 billion on those facilities, according to a filing.

Zillow Group Inc., Opendoor’s main competitor, has also moved to increase its firepower for home purchases. The company borrowed $450 million through a first-of-its-kind bond offering earlier this month.

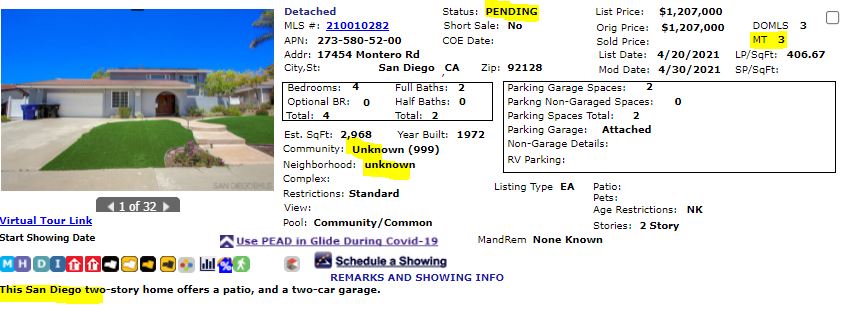

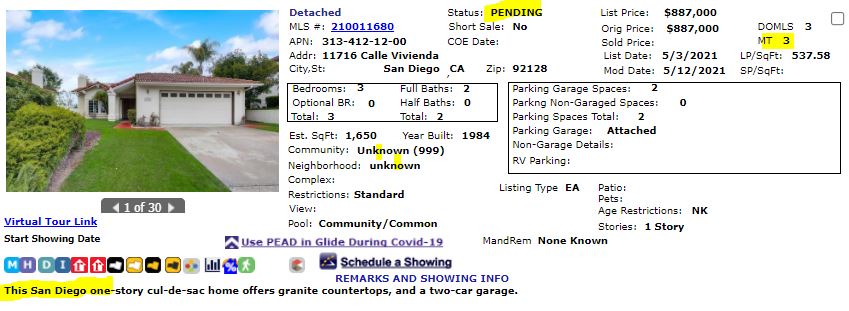

Zillow’s recent activity has been more consistent than Opendoor’s, so let’s look at the Zillow numbers to see if the convenience they offer sellers is paying off. Zillow currently owns 138 homes in San Diego County, and of those, 72 are active listings and 38 are pending. They have sold 48 homes this year – here are the 13 they have closed since July 1st:

Zip Code

Purchase Price

List Price on the Flip

Sales Price

92021

$549,000

$586,100

$585,000

92025

$542,000

$565,100

$542,000

92027

$819,000

$860,100

$930,000

92054

$927,500

$949,700

$961,900

92057

$369,500

$402,900

$425,000

92057

$763,500

$821,000

$890,000

92058

$451,500

$486,900

$500,000

92069

$831,500

$861,700

$836,600

92102

$446,000

$466,900

$475,000

92111

$430,000

$442,000

$437,600

92129

$463,000

$498,500

$500,000

92130

$605,500

$641,000

$641,000

92130

$699,500

$732,900

$727,000

Totals

$7,897,500

$8,314,600

$8,451,100

They have a consistent 2-month turnover between the day of purchase, and the day of sale, so it’s a quick $553,600 profit, or an average of $42,585 per sale – though they had to pay out close to half of that in buyer-agent commissions (all fix-ups are included in their purchase prices). It’s a good thing that sellers aren’t in a hurry – Zillow is currently six weeks behind in responding to purchase requests.

Sellers are leaving some money on the table, but as long as Zillow is flipping every home, buyers will still have the same amount of inventory to consider – it’ll just be at a higher price.

The other big ibuyer has begun operations in San Diego County.

How are they doing? The P is for pending sale, and the S is their first sold:

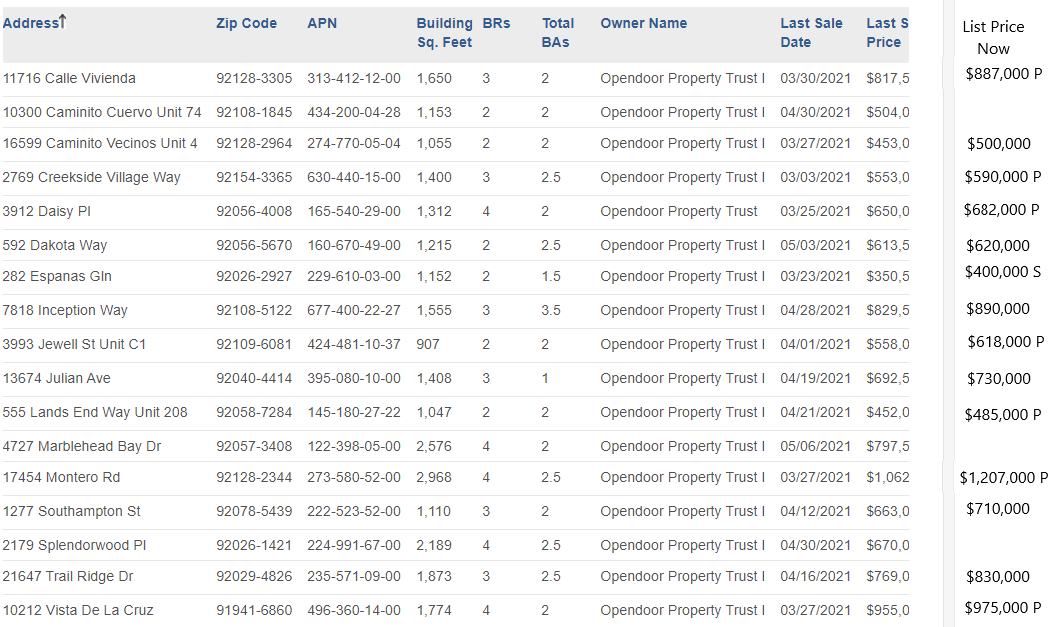

Three of the homes aren’t on the market yet, but let’s look at 14 properties that are.

They are happy to offer you a sales price that is close to the retail book value on paper, but then when they come out to visit in person, they find stuff wrong and have to deduct a big chunk to compensate.

Cash purchases: $9,418,000. Their 8.5% repairs/commissions fee: $800,530.

Net proceeds to sellers: $8,617,470.

How does it compare to selling the old analog way? Let’s assume the sellers Got Good Help, and reap the benefit of the frenzy conditions (instead of the ibuyer) when their sales price gets bid up. Let’s apply the standard 5% over-list premium to the total of the list prices above:

Difference between selling to OD, and selling with me: $1,268,616/14 = average $90,615 more per seller.

How are they selling their properties? The first few were listed with an Orange County broker, but now they have gone in-house and are listed with their Phoenix-based brokerage and agent – who got his California license less than a year ago. Hey, it’s Frenzy-2021 so they don’t have to try too hard to get properties into escrow. They offer 2% commissions with a brief description and boom – off to escrow:

The frenzy is helping to accelerate the dumbing-down of the real estate business.

There are sellers who get a postcard in the mail that offers quick cash and because the price is more than it used to be, they roll over and take it, all in the name of convenience.

Spence has gotten involved with Offerpad, joining the other disrupters who lead with lies and insults about traditional realtors.

He said, “The real competition for Offerpad isn’t Zillow or Opendoor, it’s the fact that 99.5% of the time people sell their home the old analog way.”

But at the same time, these consumers are also relying more and more on services like Uber, Instacart and Amazon. “They’ve become conditioned to wanting an ease of use,” Rascoff said. “They’ve been conditioned to pressing a button on their phone and having some magic happen.”

His magic costs 7.5%.

They don’t mention their percentage, but even analog people have a calculator handy. To offset, they pack their Traditional Offer with concessions and costs that add up to 9%, which makes theirs look like a deal.

But the worst part for any seller who makes their home-selling decision based on the cost is that they assume that everyone will sell the home for the same price. Offerpad will try to convince you that their ‘team of real estate experts’ will pay the full retail value for your home, and then hit you with the testimonials:

Will consumers go for it?

Will people ignore the math, not speak to a traditional realtor, and not know the real value of their home – and instead just press the button to have some magic happen?

P.S. They aren’t the only ones using that photo, though not sure who went first:

This is a good summary of the Zillow Offers homebuying machine. Like Amazon, they are hoping that consumers are willing to overpay for convenience:

The website that allows you to imagine living in homes you could never afford is out to do to real estate sales what Amazon did to retail.

“Our vision with Zillow Offers and Zillow is a one-stop shop, buy, rent, sell, lending and closing service,” says spokeswoman Jordyn Lee, who says the company is working toward a more streamlined approach to cumbersome real estate transactions.

It’s even partnering with homebuilders to buy their customers’ old homes, with closings scheduled to coincide with completion of the new property. The inability to sell a home is a primary source of new home purchase cancellations, experts say.

“It makes complete sense for an entity like Zillow, that is a dominant force in the housing market with its listing and information service,” says Dr. Vivek Sah of UNLV’s Lied Real Estate Institute. “Expanding into its own brand of residential brokerage will align its services together and provide a one-stop shop to its customer base.”

It also eliminates the awkward process sellers face of showing their home while living in it, and synching the timing of buying and moving to a new property.

A variety of “iBuying” services on the market cater to different niches. Some provide loans to facilitate deposits on new homes before existing home sales have closed. Others allow buyers to design new construction. Zillow is branding itself as the choice for stressed buyers seeking an immediate, hassle-free transaction.

Zillow says it’s not out to undercut sellers, citing a study by ibuying expert Mike DelPretethat indicates its purchase offers are about 3.3 percent less than market value.

That’s not the only seller concession.

“For the convenience of not doing repairs and holding open houses, we do charge a service fee of seven to nine percent,” says Zillow spokesman Viet Shelton, adding the fee is the primary source of revenue and profit from Zillow Offers.

That’s more than a conventional commission of six percent, generally split between agents for the buyer and seller.

In addition to the higher fee, Zillow deducts the costs of repairs the property needs from the amount it pays the seller.

Still, DelPrete says, it’s not a moneymaker for the biggest iBuyers, such as Zillow and Opendoor.

“The average percentage increase of a home purchased and resold by Zillow in 2019 and 2020 was 1 percent,” Del Prete said via email. “The iBuyers are not trying to profit on the resale value or appreciation of a home. This is part of the reason the model is so unprofitable and why the iBuyers are losing tens of thousands of dollars on each home sold.”

Hat tip to RK for sending in this article – an excerpt:

I asked a realtor there that I know to do a CMA on the property. When she was done, her number came out to $460,000. Zillow’s offer was $440,000. This is where things got interesting. Their pitch is that with Zillow’s service, you would be provided with a dedicated selling advisor, the ability to sell without showings, the buyer would make repairs, and you get to choose your closing date. Zillow then proceeds to inform you, the client, that “all you receive” in a traditional sale is a dedicated selling advisor. When you continue to scroll down, Zillow quotes the average realtor’s commission at 6% and then says their Zillow Service Charge is 12.9%. To their credit, they don’t hide the fact that you will pay substantially more money using their service. At the bottom of the email, it estimated my net proceeds would be $383,240 using Zillow, and if I used a realtor proceeds would be roughly $413,600.

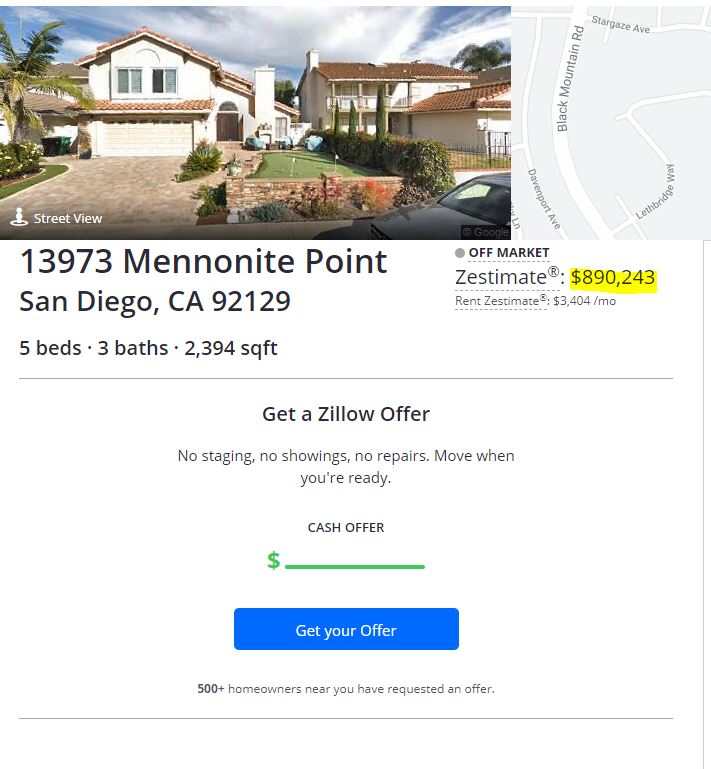

We ended up with 12 offers on my listing in Rancho Penasquitos, with SIX of them over $900,000. Donna and I did some expert maneuvering to coach the buyer-agents higher on price, and we may have gotten an assist from Zillow too.

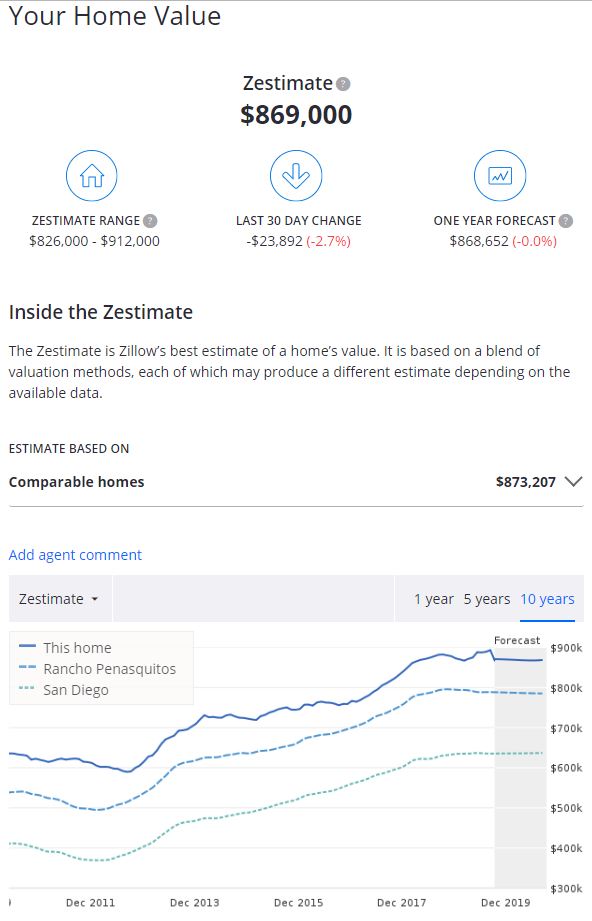

This was their zestimate before the listing hit the market:

This was their zestimate after the listing went on the MLS for $869,000. Zillow has no shame – they just hit the number. At least Redfin tries to hide it by changing their estimate to within 1%:

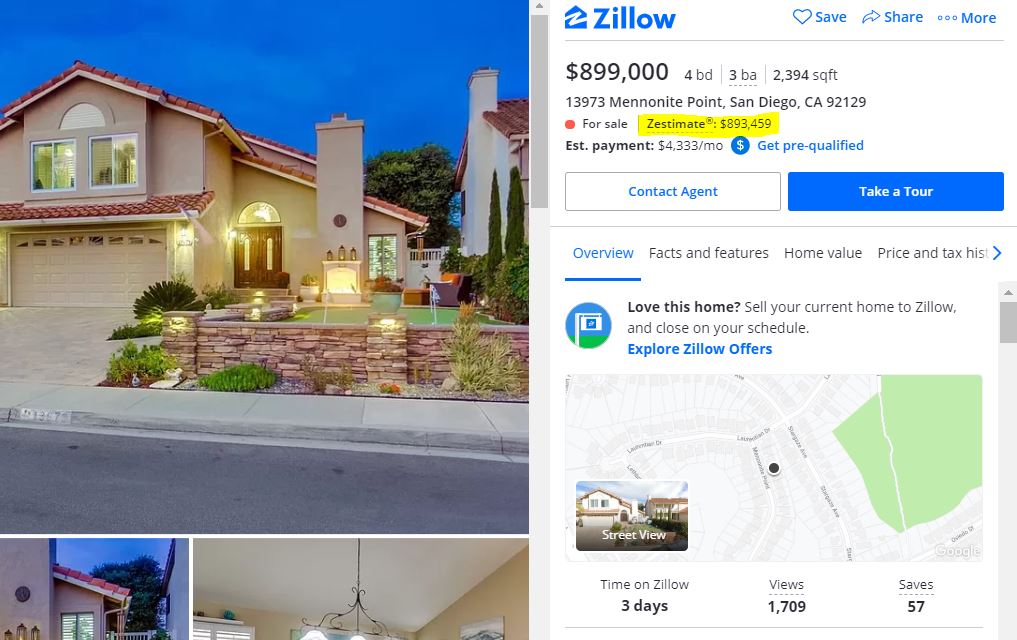

Then we RAISED our list price to $899,000 because we were getting such good action, and Zillow rasied their zestimate right back up:

They have no qualms about manipulating the zestimates right before your eyes.

Think of what they will do to you when they try to buy your house.

It’s conclusive – the Zillow Offers program is only good for sellers who want/need BOTH quick cash and max convenience, because the cost is heavy.

TIPS TO HOME SELLERS:

Don’t find yourself in a position where you NEED to cash out in a week.

If you want max convenience, hire me and we’ll handle everything.

Don’t get suckered by the bait-and-switch.

The word on the street is that they are pushing down the zestimates to help convince sellers to take less – and they have already bought 31 properties in San Diego. Keep a record of your zestimates!

Zillow will likely be successful, however, because they don’t mind spending $100 million per year on advertising to promote their brand – and it works.

The ibuyer’s quote will be a curiosity, but unless it is close to the homeowner’s expected value, then selling on the open market will seem like a better option for those who want max money.

Would a homeowner who has found another house to buy be an exception? Rather than trying to convince a seller to take an offer that would be contingent upon them selling their current home, they could sell their house instead to an ibuyer in order to purchase the next home non-contingent.

I just had a case like this, so we tried it out.

The house that needed to be sold was in Los Angeles, and the homeowners were confident about its value being in the low-$900,000s – or at least $900,000. Though it was an older home, it had been updated – and they felt that if it went on the open market that it would sell within two weeks.

The zestimate was $875,000, and when I ran the comps, most were under $900,000.

They pursued a reseller called Fast Offer, and I ran it through my source.

Their guy quoted $830,000, and because they would likely get beat up again once the reseller did a home inspection, they figured their net would be $820,000-ish…..which was insulting!

My automated source processed the address and asked three yes-or-no questions (with my answers):

Have you seen the inside of the property? Yes

Is it a fixer? No

Would you consider a discounted, quick, no-hassle cash offer based on condition? Yes

Their response was immediate:

The home doesn’t qualify.

The ibuyers have to be looking for realistic homeowners with houses that can be flipped easily and for a decent profit. They only have to ask the second question to gauge their chances – unless the homeowner admits that they own a fixer, it’s probable that they would hold out for a retail price…..or higher!

We did discuss that the $820,000 could have been close to the amount that an open-market sale would net. But in this case, the people gave up on buying the next house, rather than be ‘lowballed’ in their mind. Homeowners aren’t going to give it away!

The Compass Bridge Loan will be a better solution – and should be available this month!