#1

My all-time #1 most watched video (out of 2,155) from Christmas, 2008, The previous owners paid $927,500 in November, 2005 – I sold it for $485,000 in April, 2009 after 56 days on the market for $108/sf:

My all-time #1 most watched video (out of 2,155) from Christmas, 2008, The previous owners paid $927,500 in November, 2005 – I sold it for $485,000 in April, 2009 after 56 days on the market for $108/sf:

Just one more rerun before Kayla introduces our new listing tomorrow night.

This is the 7th most-watched video on Bubbleinfo TV, and is a greatest-hits tour through the REO-listing days. In April, 2008, the Bank of America had dumped twenty of their REOs in my lap, and over the next 12 months the JtR foreclosure extravaganza ensued.

A month after this video premiered here on the blog (March, 2009), I was on the front page of the L.A. Times, which led to the spot on ABC News Nightline:

We’re a little low on videos currently so let’s re-run an old favorite from February, 2009. This is the second-most viewed video from JimtheRealtor YouTube account, with 27,104 views!

For those who have joined us in just the last couple of years, this was a typical day on the blog during the foreclosure era:

For those wondering if there will ever be any more bank-owned properties for sale, here is the list of 38 houses between La Jolla and Carlsbad that are owned by lenders, or 3rd parties who purchased them at the trustee sale:

NSDCC Foreclosed Properties July 2015

A few are listed for sale, and others are still waiting for occupants to vacate or lawsuits to be settled. This Bressi Ranch home was foreclosed in April, 2014, and just hit the open market last week at what most would consider to be pretty close to retail price:

The former owners had worked the system – they had been in default since 2008, and endured four different trustee-sale dates before finally giving up the ship. In the meantime, the lender probably did everything they could to modify the loans?

I don’t think anybody has to worry about getting foreclosed unless they have significant equity.

From the SD Union-Tribune:

http://www.utsandiego.com/news/2015/jun/05/foreclosure-shortsale-boomerang-buyers-real-estate/?

An excerpt:

When Chad Sanfillipo got the keys to his house in Ramona last year, he had come full circle in the real estate market.

After losing his home to a short sale during the crash of the housing market, Sanfillipo was once again an owner.

“It felt so exciting to be able to buy again, to have something I own,” said Sanfillipo, 45, who rented for a couple of years before a bank would lend him money again. “There’s no landlord or rent check. I get to say what I get to do with my house.”

Sanfillipo, a systems engineer, is one of roughly 116,000 San Diego County residents who had either a short sale or foreclosure between 2006 and 2014, before and after the Great Recession, according to CoreLogic, a real estate data company.

The good news for Sanfillipo and others who lost their homes during the downturn is that there’s ultimately forgiveness in the lending market. Each month, thousands of San Diegans who went through short sales or foreclosures are completing waiting periods that render them eligible to once again apply for government-backed loans. In the worst case, some must wait seven years, but others can get new loans in just one, depending on whether they go through the Department of Veterans Affairs, Federal Housing Administration, Fannie Mae or Freddie Mac.

People who lost their homes during the recession but own again are called boomerang buyers, and they’re becoming a larger part of the market.

Boomerang buying is becoming a nationwide movement. The National Association of Realtors says that 9.3 million homeowners underwent foreclosures between 2006 and 2014. Already, 1 million of them purchased homes again, and an additional 1.5 million will become eligible over the next five years.

http://www.utsandiego.com/news/2015/jun/05/foreclosure-shortsale-boomerang-buyers-real-estate/?

Hat tip to Wendy for sending in this article on subprime vs. prime mortgages causing the crisis. The authors probably didn’t catch the fact that prime borrowers were getting neg-am loans based on FICO scores only, and those weren’t considered subprime loans:

https://fortune.com/2015/06/17/subprime-mortgage-recession/?

An excerpt:

We can draw two conclusions from this data. One is that your chances of being foreclosed upon in the past decade was more a matter of timing than anything else. If you were a subprime borrower in, for instance 2002, who bought a bigger house than a more prudent and creditworthy borrower would have bought, chances are you would have been fine. But a prime borrower who did everything right—bought a house he could easily afford, with a large downpayment—but did so in 2006 would have had a higher chance of defaulting than the subprime borrower with better timing.

Since whether you were hurt by the crisis had more to do with luck than anything else, Ferreira argues we should rethink whether doing more to help underwater homeowners would have been a good idea.

https://fortune.com/2015/06/17/subprime-mortgage-recession/?

From Slate:

One of the most acclaimed movies from the festival circuit this year is 99 Homes, the latest from Chop Shop and Man Push Cart director Ramin Bahrani. Set in Florida in the aftermath of the 2008 subprime mortgage crisis, the suspenseful drama stars Michael Shannon as real-estate shark Rick Carver and Andrew Garfield as the man that Carver kicks out of his home and then tries to make his apprentice.

Bahrani, whom Roger Ebert called “the new great American director” and “the new director of the decade” in 2009, is known for the immersive research he does in advance of all his films, and his process making 99 Homes was no exception: The filmmaker spent weeks riding the streets with real-estate brokers as they conducted evictions, going to Florida’s “rocket docket” courts as they sped through foreclosure after foreclosure, and visiting the motels where families were living after getting torn from their homes. But though it’s grounded in realism, 99 Homes also works as a Faustian thriller, in the mode of Wall Street or Training Day.

99 Homes opens on Sept. 25, which is just in time to build Oscar buzz for Shannon—though the filmmakers surely hope it will start a larger conversation.

Hat tip to daytrip for sending this along:

http://www.vice.com/read/this-former-bank-regulator-quit-his-job-to-fight-for-his-house-518

Eric Mains is fulfilling a dream many Americans have had since the onset of the financial crisis seven years ago: He’s attacking fraud in the banking industry as aggressively as he can, using every possible tool under the law to achieve justice —and win some money back for himself.

Mains, a former team leader with the Federal Deposit Insurance Corporation (FDIC), has become so bitterly embroiled in a six-year dispute with his mortgage lender that he left the regulatory agency, fearing that he might have to eventually name it as a defendant in a federal lawsuit. He’s one of a small yet determined band of people still fighting foreclosure (the seizure of property) cases with obscure and sometimes arcane arguments, built on a simple yet mind-blowing premise: The true ownership of millions of mortgages issued during the housing bubble was fatally corrupted, and now it’s impossible to prove who actually legally controls those mortgages.

Recent Supreme Court precedent suggests that by rescinding his mortgage—canceling it, basically—Mains and people like him can put the onus on banks to prove they have the right to assets like his house in the first place. If Mains or his allies succeed, they would rip open a wound that virtually everyone in power has tried to stitch up and forget. But such a long-awaited victory wouldn’t make up for the years of stress and personal hardship Mains has suffered, including a failed marriage and now the end of his career in public service.

“I had to ask myself a question: Will I do this no matter if it hurts?” Mains told me. “I said yes. If I can afford to fight these suckers and bring this illegality to light, that’s why I went to law school.”

Mains has gotten divorced, lost custody of his kid, and wound up in the hospital – read the full article here:

http://www.vice.com/read/this-former-bank-regulator-quit-his-job-to-fight-for-his-house-518

The foreclosure rate of loans originated over the last few years has been LOW!

If the strict underwriting continues, we will only see an occasional foreclosure from now on. We’ll be telling our grandkids about how back in the day there was this guy who ran a video-cam through hundreds of them!

A certain foreclosure-subscription company is always rattling their sabre about any uptick in notices. The headline for this article is: Early Stage Foreclosure Filings up Nationwide and in Most States:

http://www.mortgagenewsdaily.com/12102014_realtytrac_foreclosures.asp

But with the banks engrossed with loan-modding anyone who can fog a mirror, the only thing that matters is how many actual foreclosures are being completed. Buried deep in the article:

The dip in total filings was due to a 10 percent reduction in bank repossessions or completed foreclosures compared to October. A total of 25,249 properties were taken into bank inventories or REO, down 17 percent from November 2013.

It was the 24th consecutive month in which completed foreclosures were lower on a year-over-year basis.

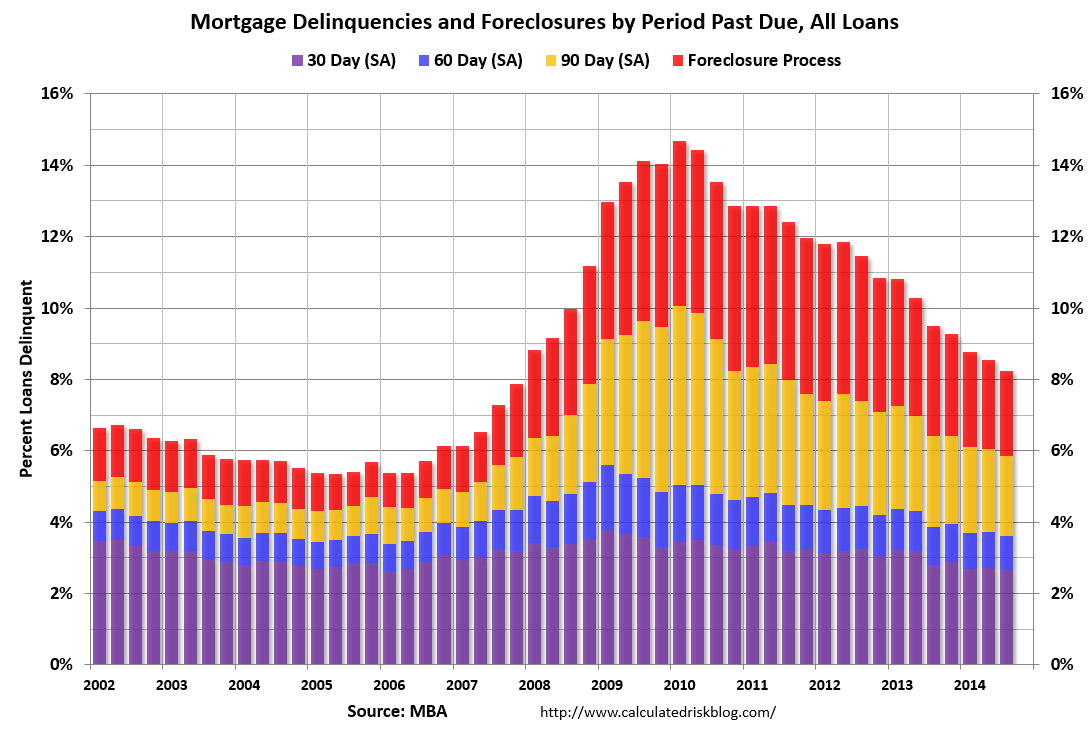

The national count of completed foreclosures has been dropping for two years straight! Bill showed how delinquencies have been tapering off too:

Regardless of how it happened, it looks like a soft landing that will last – at least as long as rates are ultra-low.

Here is how the local San Diego County numbers look:

Are you looking for an experienced agent to help you buy or sell a home?

Contact Jim the Realtor!

CA DRE #01527365, CA DRE #00873197