As blogger-in-chief here, I’ll stay on the lookout for the positive housing news – because you won’t have any trouble finding the alternative, like this guy who has been calling for home prices to drop 10% to 30% for several years now:

Link to DoomHere’s a Bloomberg essay that draws some comparisons to the 1994 market, which is another time we had a spike in mortgage rates. We had neg-am and no-doc mortgages then, and were coming off a multi-year downdraft of housing prices due to the S&L crisis, but if mortgage rates are the big decider, then it’s a fairly good comparison – note the 20% drop in new-home sales:

Housing market softness in the back half of 2018 has investors and the public wondering how bad things might get. It’s understandable that people would be worried, considering that the last housing downturn led to the worst economic crisis since the Great Depression.

But housing market fundamentals in this cycle are nowhere near as risky as they were in the mid-2000s. Real-time data on mortgage applications suggest a milder path. Coincidentally, it looks a lot like 1994.

The economy in 1994 is remembered largely for financial market turmoil brought about by sharp increases in the federal funds rate by the Federal Reserve. During that year, the Fed increased its target rate for lending between financial institutions to 5.5 percent from 3 percent, a 2.5 percent increase in one calendar year.

Perhaps not surprisingly, mortgage rates increased sharply as well. The average 30-year fixed mortgage rate increased by around 2 percentage points in 1994, ending the year north of 9 percent. New home sales slumped.

In December 1993, the seasonally adjusted annual rate of new single-family-home sales was 812,000. A year later, in December 1994, it had fallen over 20 percent to 629,000.

The other noteworthy story of the 1994 economy was what happened to the yield curve. Because of the sharp increase in short-term interest rates, the yield curve flattened significantly. The spread between two-year and 10-year Treasury rates at the end of 1993 was 1.58 percent. By the end of 1994 the spread was at 0.15 percent — close to zero, but not quite inverted.

The story in 2018 is similar. While the increase in mortgage rates this year is not as severe as it was in 1994, the housing market is dealing with other headwinds — rising costs from land, labor and materials prices, plus a shortage of inventory after years of building fewer homes than population growth would seem to warrant. An increase of one percentage point in mortgage rates between mid-November 2017 and mid-November 2018 made homes less affordable.

Similarly this year, we’ve witnessed a flattening, but no inversion, of the yield curve. The spread between two-year and 10-year Treasury rates ended 2017 at 0.52 percentage points, and as 2018 winds down the spread has been falling to close to 0.1 percentage points.

It’s understandable why many fear this is a prelude to another big crash. Home sales have fallen, and inventories are rising. Home price appreciation has slowed, particularly for higher-end homes. The yield curve has flattened, with investors starting to anticipate interest-rate cuts in 2020 and beyond.

Prospective buyers see negative stories about the housing market, get nervous, and decide to sit back and see how things go rather than putting in offers. It’s the same thing that happened before the onset of the housing bust and the great recession.

Except we’ve built nowhere near as many homes over the past decade as we did in the years leading up to the 2008 financial crisis. Underwriting standards remain strict, as anyone who has needed financing to buy a home in recent years can attest. Household mortgage debt relative to incomes or gross domestic product continues to fall. Job growth continues, and wage growth is accelerating at a slow pace.

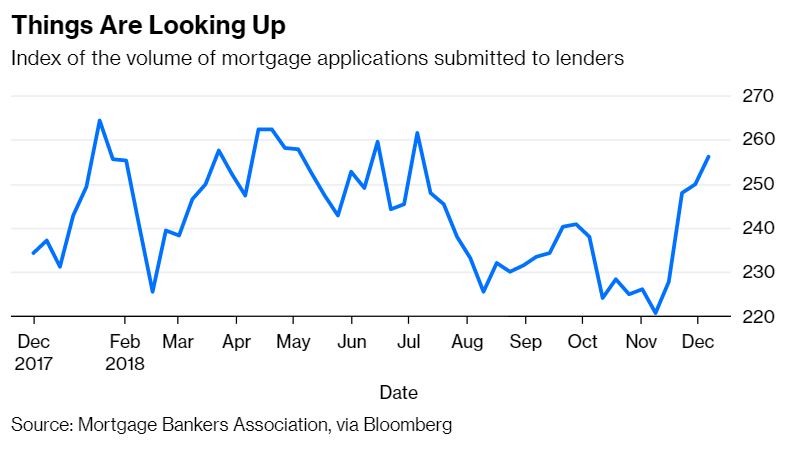

And while it’s still too early to draw any conclusions, mortgage application data in recent weeks is starting to tell a different story.

Because of the volatility in financial markets since the beginning of October, interest rates have fallen. The 10-year Treasury rate has fallen more than 0.3 percentage points from a peak of 3.24 percent in early November. Since the middle of November, average 30-year fixed mortgage rates have fallen by around 0.2 percentage points.

Mortgage purchase applications have responded to that modest drop in mortgage rates. The seasonally adjusted purchase index from the Mortgage Bankers Association has risen for four weeks in a row, to its highest level since July. The index is now up over the past year. We should be careful about reading too much into a few weeks of data, but perhaps, as happened in 1995 after the mild housing slump of 1994, a stabilization or decline in mortgage rates will support affordability, comforting the prospective buyers still a little nervous about a repeat of the troubles from a decade ago.

While housing is a smaller share of economic activity at the moment than it historically has been, a positive shift in sentiment there could be the early surprise of the economy in 2019.

Link to Article

That is a very good comparison. I bought my first house in 1990 and remember that Southern California market well. It was nothing like 2007-2012.

Agree, it was somewhat uncertain and regular until 1997 when they passed the 2 out of 5 tax-free profit and then it was off to the races.

Could it be that we are coming back to earth finally, just 20 years later?

Bruce…is calling saying we are in the 8 th inning of this rally…home prices to be flat for next 5-8 years

https://www.thenorrisgroup.com/a-year-in-review-part-2-with-bruce-and-aaron-norris-621/

Could we have half the houses go up and half go down and ‘prices’ appear to be flat?

We can start with the old, dated, unimproved two-story 70s tract houses – they are going to get crushed.

The rest could survive OK, yet the focus will be on those losing the most.

An inopportune time for disintermediation to come to the business too. Bad time to take a chance on a newby.

We saw that 3/4 of realtors have never seen a 5% mortgage. About the same number have never seen anything but a booming seller’s market.

Bruce has been right on the money all along – and check how the economists did at the bottom of this article:

https://patch.com/california/temecula/home-prices-to-increase-20-percent-investor-predicts

“It’s not my first rodeo.”

-Jim the Realtor